Life Insurance Frequently Asked Questions

When it comes to life insurance, you’re bound to have many questions. Don’t worry; the life insurance providers also have questions for you.

It’s essential to communicate and gain a full understanding of what the insurance provider is asking you, what you need to know about the provider and their coverage, and everything else you need to know to feel confident in your decision.

So, with that in mind, let’s go through the most common life insurance FAQs to look out for.

Secure Your Family’s Future. Start with Your Custom Life Cover Quote Now

Important Questions to Ask

Life insurance is simple in concept, but, as with any industry that has existed as a commercialised entity for centuries, it’s full of complexity and intricate details.

Asking important questions helps you understand what’s on offer for you, what you can expect from life insurance, and what the details are for the coverage you’re seeking.

Do you need life insurance coverage?

This one is less of a question for your insurance provider and more of a question for yourself.

So, ask yourself this: Is there anyone in your life who depends on your income and savings to survive? Spouses, children, and others are all potential beneficiaries of the benefits you can get from life insurance.

It is, after all, insurance. If you don’t need it, great! You’ve lived a long and healthy life and settled your affairs.

On the other hand, if you suffer a tragedy, you can at least rest assured that your loved ones are cared for in your absence.

Indeed, there’s a common myth that life insurance cover is only necessary if you’re already elderly or if you’re infirm or otherwise anticipating an early demise.

Truthfully, though, life insurance can benefit anyone who has someone else in their life to care for.

Consider, as well, any debts and financial obligations you may have. In addition to burial arrangements and the costs associated with funerals, is your mortgage paid off?

Do you have debts with co-signers, or will they be paid out of your estate?

Any debts or other burdens that would carry over to a dependent or spouse after your passing can be paid off using a life insurance payout instead.

Should you seek a term or a whole life policy?

Term life insurance is often viewed as a gamble. You lock in a low premium for a reasonably high amount of cover for a fixed term, such as 10, 20, or 30 years.

If you pass during that time, your beneficiary can claim your death benefits, and the policy will pay out. You gain no real benefit from it while you’re alive, save for peace of mind, and if you outlive your cover, you have nothing to show for it.

Whole life insurance instead lasts as long as you continue to live and pay into it. It usually costs significantly more because it’s almost guaranteed to pay out, except in cases of fraud.

Often, it even has an added cash value similar to an investment account you can access in your golden years, so you gain some benefit from it while you’re alive.

Many people argue that whole life cover isn’t a good option because the same money in an investment account will bring you more returns, and that may be true, but it depends on doing the math yourself.

Here’s a helpful chart comparing the two:

| Factor | Term Life | Whole Life |

|---|---|---|

| Duration of cover | Cover for a specific period, usually 10 to 30 years. Designed to protect during high-need periods. | Lifelong cover as long as premiums are paid. Does not expire after a set term. |

| Cost | Higher premiums are due to lifelong coverage and cash value components. Premiums remain level for life. | It offers a guaranteed death benefit and the potential to accumulate cash value over time. |

| Benefits | It provides a death benefit if the policyholder passes away during the term, but there is no cash value component. | Generally, it is more affordable due to the limited coverage period and the lack of cash value accumulation. Premiums are fixed during the term. |

| Cash Value Accumulation | Generally, it is more affordable due to the limited coverage period and the lack of cash value accumulation. Premiums are fixed during the term. | Part of the premiums contribute to cash value, which grows tax-deferred. It can be borrowed against or withdrawn. |

How are your death benefits paid?

If you pass away, you may be concerned with how many hoops your beneficiary will need to jump through to receive your death benefit.

It can be valuable to ask your insurance provider how they pay out your benefits, what the process is, and what your dependents may need to have to be able to make the claim.

One significant question is whether the money is paid out in one lump sum or if it’s taken as an annuity or instalment plan.

One may be more beneficial than the other, depending on your dependents’ financial situation after your passing.

Taxation Of Cover?

Life insurance payouts are generally free from Income Tax and Capital Gains Tax in the UK.

However, the payout may be subject to Inheritance Tax if it increases the value of the deceased’s estate above the threshold.

Writing the policy in trust can help avoid Inheritance Tax and ensure faster access to the funds.

Are there limitations, exclusions, or riders on your cover?

Many insurance policies are broad and generalised. If you pass away during your covered term and have kept up with paying your premiums, your beneficiary simply needs to file the claim, and it will be processed and paid out.

Not all life insurance policies are so easy to manage, however. Sometimes, they may have exclusions or limitations on when they will pay out.

For example, if you sign up for cover and pass away within a few months, your cover may not have kicked in yet and thus won’t pay out.

Other policies may have specific causes of death excluded from valid payouts; for example, many have suicide riders, so you can’t sign up for a large policy and then commit suicide to deliver the lump sum to your beneficiary.

More commonly, a policy may allow you to exclude a particular cause of death in exchange for a cheaper premium.

That cause is more likely to be a critical illness or ongoing ailment you already suffer. This can vary from provider to provider, so be sure to discuss the topic with them.

How do you know the insurance provider is reputable?

There are many different lists of the best insurance providers in the UK. They often include the same list of names, including companies such as Aviva, Vitality, Zurich, Royal London, AIG, and Direct Line. Others, such as Aegon, Liverpool Victoria, and AXA, are frequently mentioned.

You have a few options other than simply using lists of reputable names and choosing one.

First, you can vet them yourself according to your needs. Follow their application process thoroughly to obtain a quote and compare it with quotes from other reputable providers.

Look into their history and check for complaints or issues with paying out benefits. Look for complaints against them. Ask them what percentage of claims they pay out.

Another option is to look for organisations that vet and reinforce insurance providers. Groups such as the British Insurance Brokers’ Association, the Association of British Insurers, and others can all provide lists and recommendations for reputable and trustworthy insurance providers.

Questions Your Provider May Ask You

Now, let’s reverse the situation and discuss the questions your prospective life insurance provider will ask you and why they’re important.

What is your medical history?

Your medical history is an important part of the calculations an insurance provider does to classify your risk to them.

This will involve basic information like your height and weight, your history with tobacco and various drugs, and any medical diagnoses you’ve received.

You will also likely need to disclose any pending tests you’ve performed, any prescriptions you’re currently on, any planned treatments, and any procedures you’ve done. You’ll also need to disclose your history with issues like strokes or diabetes.

All of this is important so the insurance provider knows how risky it is to extend coverage to you and what price point makes financial sense for them to do so.

However, some information is protected, and your insurance provider can’t ask about it. This includes genetic testing for non-diagnostic purposes.

It’s also essential that you are honest with all of these answers. If you try to hide something from your provider or lie to them about something you’re aware of, it can get your claims denied if you do end up passing away and they discover the fraud.

They will also generally cross-check the answers you give them with your medical records, so they’ll be able to spot some lies or omissions immediately.

Do you have occupational risk factors?

Chances are, you will have a whole section of the application for life insurance coverage that goes into detail about your occupation and the risk factors you may experience in it.

These can include questions such as:

- Do you often engage in dangerous tasks at work?

- What is the typical environment in which you’re working?

- Do you regularly need and use personal protective equipment?

- Do you work with dangerous or hazardous chemicals?

- Do you work with dangerous or hazardous machinery?

These and other questions are all part of an overall analysis to determine if you have any job-related risk factors.

Someone who drives a lorry for a living, works in a quarry or a mine, or works with toxic chemicals will have higher risk factors than someone who works in an office building or as a sales clerk.

As with any other question your insurance provider asks you, it’s all about classifying your risk levels.

Similarly, you will generally be asked about your lifestyle and the risk factors that may arise from the activities you engage in as hobbies or for entertainment.

Obviously, Someone who likes to skydive, climb mountains, go scuba diving, or race motorcycles will have a higher risk than someone whose hobbies include reading, bird-watching, and jigsaw puzzles.

Are there concerning elements in your family history?

Your family history can be a direct risk factor for a variety of genetic and hereditary ailments. People who have a family history of cancer are more likely to develop cancer than people whose families don’t seem to develop cancer as often.

The same goes for many diseases, such as kidney disease, liver disease, heart disease, asthma, anaemia, high blood pressure, high cholesterol, epilepsy, dementia, autoimmune diseases, and more.

There are undoubtedly many reasons why you might not develop the same ailments as others in your family. It’s also possible that you’re unaware of your family history.

People who never knew their parents, who were adopted, or whose family has passed before it could be discussed, all may have spotty or non-existent family histories.

While you can pursue genetic testing to evaluate your risk factors, you don’t necessarily need to disclose the results of those tests.

The insurance provider will generally not request the results of genetic testing, nor will they require a genetic test, except in rare cases.

It’s worth noting, however, that if you independently pursue genetic tests and find that you do not have the same risk factors that your family history would imply, you can also intentionally inform your insurance provider.

Generally, they will take such positive information and adjust your risk profile to mitigate the effects of the negative family history.

Where Can You Get the Best Life Insurance in the UK?

Finding good life insurance coverage is easier now than it ever has been in the past.

You no longer have to identify and reach out to every insurance provider individually, navigate all of their application processes, fill out the same forms repeatedly, and spend all that time seeking a quote.

Instead, all you need to do is fill out one simple form.

When you fill out our quote form – or even call us so our agents can do it for you – we send it to the UK’s best insurance providers on your behalf.

All you need to do is wait, and they’ll send you quotes for cover in no time. From there, it’s just a matter of comparing the best quotes you receive and picking the one that best suits your needs. It’s fast, easy, simple, and more effective.

Obtaining life insurance doesn’t have to be tedious or stressful.

Whether you’re newly graduated from university and want to secure your family’s future, or you’re approaching your golden years and want to leave a lasting legacy, we can find the right policy for you.

Why should I have life insurance anyway? Here are some further answers to commonly asked questions

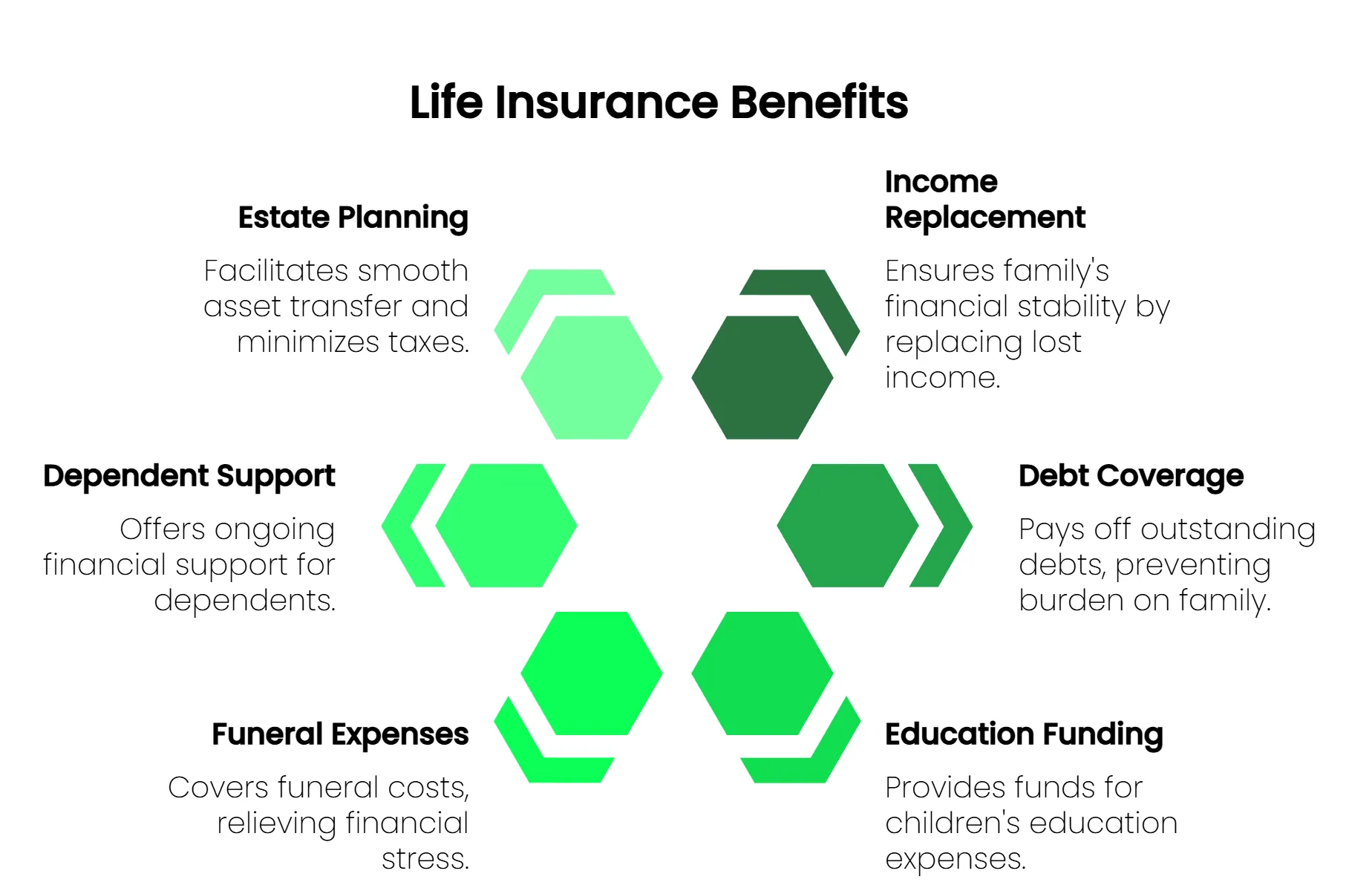

Most insurance policies are designed to protect the insured’s property. Life insurance is designed to protect dependents from the financial impact of your serious illness or death.

Some mortgage lenders require homeowners to have life insurance. This assures that the mortgage balance will be repaid if the homeowner dies before the mortgage loan is satisfied.

Should people without mortgages purchase life insurance?

Yes, because a life insurance policy can be used for various purposes. Basic term insurance can run for the duration of the mortgage. Decreasing term insurance features coverage that decreases over time.

If I am young and healthy, do I need life insurance?

The main factor when considering whether life insurance is worthwhile is whether another person will suffer a financial loss upon your death.

Will family members be able to make mortgage payments and pay household expenses?

If you have a joint mortgage with a partner, does that person depend on your income to help repay the mortgage?

Regardless of age, purchasing a life insurance policy is wise if you rely on someone for financial support.

What happens if I stop paying my premiums?

If you discontinue paying your premiums, the coverage provided by your life insurance policy will cease. In the unfortunate event of your passing after this point, your family or dependents will not receive any monetary benefit, and you will not be entitled to a refund of the premiums you had previously paid.

Before committing to a life insurance policy, you must carefully assess your financial situation and ensure you can consistently meet the premium payments.

Selecting an affordable policy is crucial to ensure continuity of coverage and provide financial protection for your loved ones.

What illnesses or health conditions are not covered by life Insurance companies?

Several factors regarding illnesses or conditions not covered by Life Insurance must be considered. While specific exclusions can vary between policies, certain elements commonly apply across the board.

One common exclusion is related to deaths caused by substance abuse, such as drugs or alcohol, as well as deaths resulting from suicide. These are typically not covered by most life insurance policies.

Additionally, those who work in high-risk occupations, such as those in the armed forces or the oil industry, may face complications when applying for life insurance.

Engaging in dangerous sports or activities is another factor that might lead to a rejected life insurance application.

For example, people involved in motorbike racing or mountaineering might find it more challenging to secure coverage.

It is important to note that the specific exclusions can vary depending on the policy and insurance provider.

Therefore, it is advisable to thoroughly review and understand the terms and conditions of any life insurance policy to determine what illnesses or conditions may not be covered.

Can I get Life Insurance at work?

Yes, it is possible to obtain life insurance coverage through your employer. This type of life insurance, often called death in service benefit, provides a lump sum payment to your beneficiaries in the event of your death while employed by the company.

However, it is essential to note that relying solely on this coverage may not be sufficient for everyone.

You might consider supplementing your employer’s life insurance with additional coverage for a few reasons.

Firstly, if there is uncertainty about the longevity of your employment with the company, having your life insurance policy ensures uninterrupted coverage regardless of your employment situation.

When evaluating the adequacy of your employer’s life insurance offer, you should consider factors such as your outstanding mortgage, any other debts you may have, and the daily living expenses of your dependents.

It is essential to thoroughly assess whether the coverage amount will be sufficient to meet these financial obligations and provide your loved ones with the necessary financial security in the event of your death.

If I already have life insurance, can I still save money?

During the past decade, life insurance premiums have drastically declined. If you purchased coverage several years ago, you will probably find the same level of coverage now offered at a reduced cost. However, this may require switching to a new insurer.

A thorough market search is necessary to find the best deal; we do this for you at no charge.

Will a life insurance policy always pay a benefit?

Many policies feature payout exclusions, including suicide. Insurers also may not payout due to a situation the insurer has not been informed about.

For example, a life insurance policy would be voided for an individual claiming to be a non-smoker who begins smoking after being insured but does not notify the insurance company.

Does the policy have to be paid out all at once?

No, the policy does not always have to pay out the money all at once. Family income benefit is an option, where your dependents receive the payout in regular monthly instalments.

This ensures that your family does not have to worry about managing too much money at once. Individuals who prefer a steady income stream for their loved ones often choose this option.

Additionally, family income benefit policies usually have lower premiums than other types of life insurance, resulting in a lower payout amount.

Can I take out a joint life Insurance policy with my partner?

Yes, you can indeed take out Joint Life Insurance with your partner. Joint life insurance is a type of policy specifically designed for couples.

It provides coverage for both individuals under a single policy. In the event of one partner’s death, the insurance company will pay out a lump sum to the surviving partner.

However, it’s essential to understand that joint life insurance policies typically have some specific considerations.

Firstly, the policy will only pay out once when one partner dies. This means that after the payout, the surviving partner will no longer have coverage under the same policy.

Secondly, it’s worth noting that the surviving partner may face challenges in obtaining life insurance coverage again.

This is because the surviving partner will now be older than when they initially applied for the joint policy. As age is a factor in determining life insurance premiums, it may be more difficult or expensive to secure independent coverage in the future.

Should I make amendments to my existing Life Insurance policy?

It is crucial to regularly assess whether your life insurance policy aligns with your evolving life circumstances and needs.

Changes happen over time; you may get married, buy a new home, or have children, which can significantly impact what you seek from your life insurance coverage.

Regularly assessing your life insurance can identify gaps or areas where adjustments may be necessary.

For instance, if you have recently married, you might want to consider adjusting your policy to include coverage for your spouse.

Similarly, if you have become a homeowner, it is wise to assess whether your coverage is sufficient to protect your mortgage or other financial obligations associated with homeownership.

If you have children, you may want to consider increasing your coverage to provide financial security for their future.

Remember to keep your insurer informed about any significant life changes. While making amendments to your policy based on these changes is crucial, it’s essential to understand that it might result in higher premiums.

However, overlooking necessary updates or failing to adjust your coverage to your current needs could leave you underinsured or without adequate protection.

Can I structure a life insurance policy to make continuous monthly payments instead of a lump sum?

Yes, this is typically done by purchasing a family income benefit policy. This coverage makes a monthly payment to beneficiaries, designed to replace the wages of the deceased (or possibly critically ill) insured.

A family income benefit policy usually costs less than one that pays a lump sum because the insurance company does not fund the entire benefit at once.

What if I require my Life Insurance plan to cover me until I die?

Whole-of-life insurance would be a suitable option if you intend to have life insurance coverage until the end of your life.

Unlike term insurance, this plan guarantees a payout regardless of when you pass away, providing you and your family with financial security.

It is important to note that whole-of-life insurance tends to be more expensive than term insurance because the payout is practically assured.

Nevertheless, the benefit is that it ensures that your loved ones will be fully taken care of after you pass away.

When determining life insurance policy benefits, should funeral arrangements be considered?

Pre-paid funeral plans can be purchased separately, but these can be expensive. Adding funeral arrangement costs to the coverage level for a life insurance policy can be less costly.

What are the main types of life insurance?

Term life insurance provides only protection, while whole of life insurance is also an investment. Our website provides detailed information regarding each type of policy.

What is critical illness cover?

Critical Illness Cover, also known as critical illness insurance, is an optional add-on to regular life insurance that provides additional financial protection in case of a severe illness or disability diagnosis.

Unlike traditional life insurance, which pays out a lump sum to your loved ones upon your death, critical illness cover pays out a lump sum directly if you are diagnosed with a qualifying medical condition during the coverage period.

This type of insurance is particularly beneficial if you rely on your salary to support yourself and your dependents.

Suppose you are diagnosed with a critical illness or disability. In that case, the lump sum payout can alleviate some of the financial burdens associated with medical treatments, loss of income, or any other expenses that may arise during this challenging time.

It’s important to carefully review the medical conditions covered by your critical illness policy before purchasing. Our comprehensive critical illness list will hopefully be a helpful guide and is regularly updated.

Policies may differ in the number and types of illnesses, disabilities, or medical conditions they cover. Additionally, it’s worth noting that some policies may restrict the number of times they will pay out.

For instance, specific policies only provide a one-time lump sum payment upon diagnosis. If you receive this payment during a critical illness, your loved ones will not receive any benefits upon your death.

By choosing critical illness cover, you can find reassurance in knowing that you have an extra layer of financial protection in place should you experience a serious medical condition.

Why do some companies refer to term insurance as temporary insurance?

This wording is used because term insurance provides coverage for a specific timeframe, referred to as the term, not the lifetime.

What are increasable term and increasing term life insurance, and how do they differ?

Both policies accommodate increased costs that an insured may want to cover during a policy period. An increasable term policy can increase premiums at specific times, like the policy anniversary date or when a particular event occurs.

With an increasing term policy, the premium is automatically increased by a pre-determined amount, such as a fixed percentage per year or based on current inflation levels.

As the premiums increase on each policy, the coverage amount also increases. For example, if a £100,000 policy features a five per cent premium increase, the coverage will increase by the same amount, resulting in £105,000 worth of coverage.

What is decreasing term life insurance, and when is it appropriate?

With a decreasing term life policy, premiums and coverage decline over time. A person who wants life insurance coverage that protects mortgage payments typically selects a decreasing term policy because the amount owed to the building society or bank decreases each month throughout the policy term.

A lender may refuse to provide a mortgage without proof of life insurance, but a lender may not force an individual to purchase its life coverage.

Glossary Of Life Insurance Terms

We have compiled a glossary of life insurance terms commonly used in our industry. Refer to this section as you read the…

Insurance Premiums Frequently Asked Questions

What are the main factors affecting life insurance premiums? Read on to find out Policy type and coverage amount…

What Are The Differences Between Life Assurance And Insurance?

Life assurance sounds like life insurance, but it is not the same concept. Both were created to help beneficiar…

What UK Life Insurance Policy Makes Bonus Payments For No Claims?

While thinking about our own death is not a happy topic, it is necessary to consider how loved ones will carry on. It is…

How Are Life Insurance Companies Affected by Economic Changes?

When the economy experiences changes, many industries feel the effects. Risk management, a significant aspe…

Will My Life Insurance Be Subject To Inheritance Tax?

Inheritance tax is paid on some gifts or trusts and on the estate of an individual who dies. Not all UK res…

Joint Mortgage Life Insurance Policy Guide 2026

Several types of mortgages are available to UK residents, and a joint mortgage features the names of two people. …

Will I Save Money With a Term Life Insurance Policy?

Life insurance policies come in various policy options, so you have plenty of choices when looking for a policy that can…

Is Life Insurance Available Through My Employer?

While there will be some companies that offer life insurance policies as a benefit to employees in the UK, this is the e…

Am I Owed a Life Insurance Payout In 2026?

When taking out life insurance policies in 2026, most people name others as their beneficiaries. Some do no…

The Increasing Cost of Dying

Death is an inevitable conclusion to life, and when someone dies, surviving loved ones often hold a funeral as a formal …

Common Reasons Life Insurance Does Not Pay Out

People buy life insurance policies to ensure their family’s well-being once the person isn’t around to provide. For ot…

What Happens When Family Members Do Not Provide Life Insurance Policy Details?

Families are social units, and they can reflect all of such groups’ positive and negative aspects. While some f…

Why Do Quotes from Insurance Comparison Sites and Advisors Differ?

After deciding on a suitable type and level of life insurance, consumers should compare prices offered by different prov…

Can My Children Be Added To An Existing Life Insurance Policy?

You must look at your policy to see if a clause allows children to be added after the initial signing. If this …

When Should I Buy My First Life Insurance Policy?

If you are wondering about the best age to purchase life insurance, you recognise the importance of this cover, which me…

Reasons to Purchase Life Insurance In 2026

Upon initial consideration, paying to insure your life may seem unnecessary and expensive. A closer look re…

Should I Have Life Insurance If I Am A Single Person?

For those of you still single, you may be asking if you need some type of insurance coverage. After all, you ar…

Association Of British Insurers ABI And Life Insurance

The Association of British Insurers (ABI) provides general information regarding savings and insurance products and serv…

Does Relocating from UK Invalidate Life Insurance?

Whether you are an expat or considering moving out of the UK for another reason, consider the many consequences. …

How Much Life Insurance Do I Need In 2026?

It’s a common question: how much life insurance do I need if I’m single or part of a family unit? A general guid…

Four Great Ways To Compare Life Cover

Buying life insurance is never going to be an easy purchase as there are so many variables Ultimately, the same…

How To Find Lost Unclaimed UK Life Insurance Policies In 2026

Time stands still when a loved one dies, but much must be done. After making funeral and burial arrangements, i…

Life Insurance Change Of Circumstances 2026

Life is full of surprises. You may have been happily married for 25 years, but life throws you an obstacle, and a family…

What Is A Waiver Of Premium In Life Insurance?

Did you know that you can insure your life insurance policy premiums? A Waiver of Premium addon or “rider” insu…

How Do Life Insurance Companies Make Money?

If you are shopping for life insurance, it might have crossed your mind how do insurance companies make their money? Aft…

Do You Need Life Insurance For A Mortgage?

If you’re considering buying a house, there are a lot of essential factors you need to consider before doing so. One o…