Death In Service vs Life Insurance Guide

A common benefit employees can obtain at a workplace is death in service. Theoretically, death in service seems to be similar to life insurance.

Both ensure a person and guarantee a lump payout to the beneficiary of a deceased person. However, upon closer inspection, both types of insurance are quite different and can benefit you in different circumstances.

Our death-in-service vs. life insurance guide will examine how the two differ and whether you should have both.

What Does Death in Service Mean?

An employer usually offers death-in-service benefits at the workplace as a perk. Similarly to life insurance cover, it is paid upon an unfortunate accident that results in your death.

Death in service is a benefit you are not obliged to take out at your workplace – hence, it is usually referred to as a work benefit.

If you decide to purchase death in service insurance, you are protected by it as long as you are employed by the employer who issued it to you.

Consequently, when you quit your work or are fired, you automatically lose the insurance.

To qualify for a death-in-service cover, some employers require their employees to be members of a pension scheme. This does not include a type of pension that was known as SERPS.

Death-in-service payments upon death also vary. It is usually a lump-sum payout between 2 and 4 times the annual salary.

Death-in-service benefits at the workplace can be somewhat limited. Depending on the death in service cover, choosing a preferred beneficiary may be a problem, along with the purpose to which the money will be given (e.g., mortgage or debts). The case is different with the life insurance cover.

In contrast to most life insurance covers, death in service cover doesn’t take your health condition, bad habits, risky hobbies, etc., into consideration.

What Is Life Insurance?

A life insurance plan is a coverage that insures you for life until death. In the event of an unfortunate occurrence, an insurer pays a lump sum to the beneficiary listed in the contract.

Unlike a death in service cover, life insurance is usually purchased individually. Life insurance is an umbrella term that combines different policy types based on age, occupation, and health problems.

You can purchase more than one policy, for example, family income benefit insurance and a life cover for disabled individuals. The covers remain valid as long as you keep paying monthly premiums.

Monthly premiums are the amount you regularly pay, and they are based on specific criteria such as age, habits, occupation, length of coverage, and policy type.

Life insurance providers offer two types of premiums: guaranteed and reviewable. A guaranteed premium remains the same up until the final day of your contract.

On the contrary, a reviewable premium is occasionally reviewed and adjusted (usually increased) by the insurer.

Death in Service vs Life Insurance: Pros and Cons

Death in Service

Pros:

- Provided by an employer for free

- The payout is tax-free

- As long as you are employed, your death is covered by the benefit

- The payout is 2-4 times your annual salary

- You are not underwritten for death in service

Cons:

- You lose your benefits as soon as you leave your job

- If you change your job, a new employer may not provide death-in-service benefits

- The payout is a multiple of your salary, which may not be enough to provide long-term financial stability for your family

- You nominate a beneficiary, but your employer has the final say

- You cannot allocate the payout to cover a mortgage, loan, or debt

Life Insurance

Pros:

- You choose the coverage amount, ensuring the financial security and peace of mind of your loved ones

- There are many types of life insurance

- The payout is tax-free

- You can allocate your payout to pay off a mortgage loan, a credit card debt, etc.

Cons:

- When taking out life insurance, a provider needs you to disclose all information about your health, mental state, habits, etc.

- Your monthly premiums may increase based on various factors (e.g., age, pre-existing health condition, etc.)

Death in Service vs Life Insurance: Key Differences

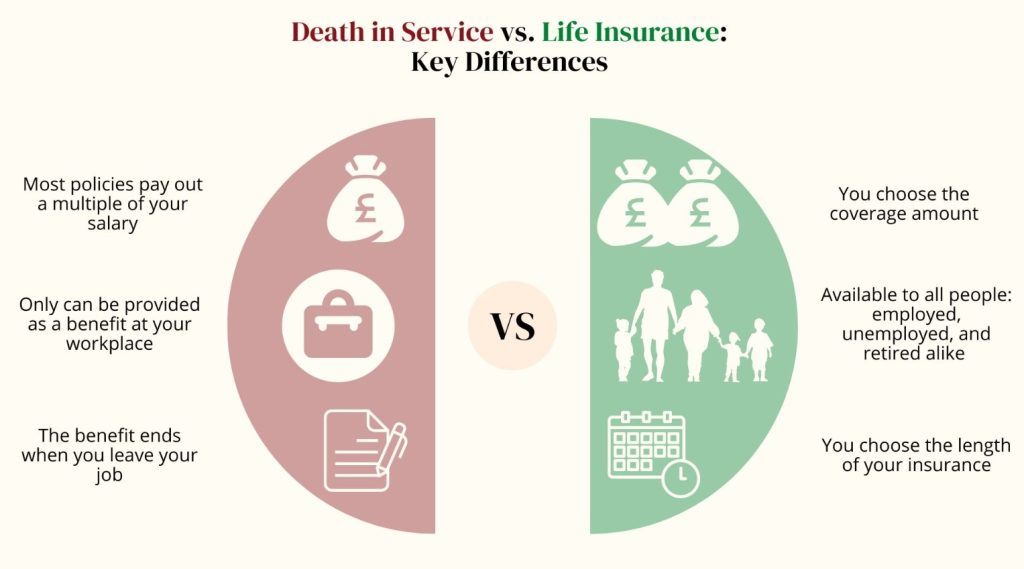

Although both death in service and life insurance are paid at the event of your death, they have three key distinctions: availability, coverage amount and length, along with other somewhat deal-breaking intricacies.

- Availability

Death in service is provided only by an employer; not every workplace has such a benefit. It isn’t mandatory to purchase the cover, but it is a nice addition to your existing insurance.

Life insurance is available to anyone who wants to purchase it. You don’t need a job to get it.

There are no limitations either, as there are many types of life insurance, e.g. over 50’s insurance, critical illness coverage, extreme sports life insurance, etc.

Regardless of occupation, age, or health condition, anybody can take out life insurance.

At the same time, there is no underwriting process when obtaining a death-in-service benefit. However, when taking out life insurance, you will be questioned about your health condition, hobbies, and habits.

- Coverage amount

Death in service is provided by an employer and does not include monthly premiums. This means you don’t have to pay for your insurance, but at the same time, there is little you can influence in its contract.

Since selecting the desired payout sum is not always up to you, your beneficiary may receive less than you would have wanted.

You set the terms for life insurance during the application, including the beneficiary and the desired coverage amount.

Your terms may or may not affect the monthly premiums, but adjusting the final proposition has never been a problem.

Both death in service and life insurance provide tax-free benefits, but it’s important to note that your individual circumstances may affect this.

Additionally, life insurance payouts may be considered a part of your estate and may be subject to inheritance tax.

It’s always a good idea to speak with a financial advisor or tax professional to understand how these policies may impact your situation.

- Insurance length

Death in service is valid as long as you are employed and expires as soon as you leave your job. This means that in the event of your death, your beneficiary will not receive the payout after you are no longer employed.

In contrast, you are protected with life insurance as long as your contract states it, and you keep paying the monthly premiums. Failure to pay monthly premiums may render your insurance invalid.

Death in Service Limitations

We’ve stated that life insurance offers a lot of flexibility regarding the length and amount of coverage. It is not always the case with death-in-service cover.

Unlike life insurance, where you have many options, death-in-service benefits work differently.

You cannot always select your preferred beneficiary (although you can nominate one), but the final work usually goes to your employer.

With the benefit, you cannot specify that the payout will cover specific expenses, such as a mortgage, loan, or credit card debt. However, it doesn’t mean your beneficiary will have any barrier to paying off any credit.

Do I Need Life Insurance and Death-in-Service Cover?

A life insurance policy is beneficial for many reasons, and a death-in-service cover is an additional opportunity to secure your family.

You have an opportunity to shield your family from the financial crisis with two reliable sources of insurance coverage.

Supplementing death-in-service coverage with life insurance will provide financial stability for many years to come.

Whilst death in service is beneficial, it’s not guaranteed that you will always keep working at your workplace. If you change jobs, your new employer may not offer death-in-service benefits.

Taking out life insurance is your safety net in case you have a health problem and won’t be able to work due to limited physical capabilities.

The same applies if your hobby is an extreme sport that may result in an unfortunate accident.

Life insurance is always better to take out earlier because the older you become, the more expensive your monthly premiums will be due to a higher risk of developing health-related problems.

Whilst death in service is a great benefit and secures you as long as you are employed, life insurance guarantees financial stability in the event of your death.

Death In Service vs Life Insurance Frequently Asked Questions

Here are the most common questions regarding death in service vs life insurance coverage:

Is death in service taxable?

No, the death-in-service payout is not taxable.

Is the death of service payout enough?

It is usually your employer who determines the value that will be paid in the event of your death. Commonly, the payout is 2-4 times your annual salary.

Discussing the details with your employer will help you determine whether the lump sum is enough to support your family in the event of your death.

The benefit of death in service is that it is free of charge and valid as long as you are on the payroll.

What is underwriting?

Underwriting is a process that every applicant goes through when applying for insurance coverage. The process is meant to evaluate the applicant’s risk and whether a provider is able to ensure the person’s safety.

The underwriting process also determines the cost of monthly premiums. There are various factors that influence underwriting, including pre-existing health conditions, mental state, age, bad habits, etc.

Applicants marked as high risk tend to pay higher monthly premiums.

Another factor is the insurance length. To make a profit, a provider may charge a higher price to those seeking short-term insurance coverage.

That’s why it is always recommended to opt for extended coverage at a younger age to reduce premium costs.

In short, underwriting is the process of collecting information about an applicant to determine the overall level of risk.

It is important to disclose all the information at this stage and not to hide anything, as it may invalidate your insurance in the event of your death. This means that if you deliberately lie on your application, you risk putting your family in a complicated situation.

Can I take out life insurance when having death in service at work?

Yes, you can. Death in service is provided only by an employer, while anyone can take out life insurance. They will both pay a lump sum to your beneficiary in case anything happens to you.

Death in service is rather a benefit you have only when working for an employer. However, life insurance is available before, during, or after you start working.

Your life insurance may differ from your death-in-service benefit. There are many types of life insurance covers suitable for people of any age and occupation.

Steve Case is a seasoned professional in the UK financial services industry, with over twenty years of experience. At Insurance Hero, Steve is known for simplifying complex insurance topics, making them accessible to a broad audience. His focus on clear, practical advice and customer service excellence has established him as a respected leader in the field.