Life Insurance For Smokers – Lower Rates Are Possible

Estimates in the UK still indicate over 9 million people smoke despite smoking restrictions in indoor public places. Smoking-related deaths are also still elevated at close to 100,000 per year.

Are you a UK resident who smokes? Do you ever worry that your habit will impact your family should you die early from a smoke-related illness?

Despite what you may have heard, cheap life insurance for smokers is still available and may not cost as much as you think.

Reasons To Take Out Life Insurance For Smokers:

Life insurance for those who smoke is essential. It offers peace of mind that your loved ones are financially protected should the worst happen.

Here are the top reasons for smokers to consider life insurance:

- Financial Security: Life insurance provides crucial financial support to your family, helping cover daily living costs and outstanding debts after you’re gone.

- Health Risks Mitigation: Given the health risks associated with smoking, such as higher chances of developing severe health conditions, life insurance ensures that these risks do not translate into financial burdens for your family.

- Cost-effective Options Available: Although premiums can be slightly higher for smokers, comparing quotes can help secure affordable rates, particularly when arranged earlier.

- Policy Flexibility: Smokers can access various policy options, such as level-term and decreasing-term life insurance, tailored to meet their personal and financial circumstances.

- Future Planning: This ensures your family can maintain their lifestyle and cover significant expenses like mortgage payments or education costs without your economic contribution.

We are confident that we can offer smokers a significantly better life insurance policy than they are likely to find through commission-driven and often biased comparison engines.

Life Insurance For Ex And Current Smokers. No-Obligation Quote Form

Reasons To Get A Quote Today

- Fair Premiums – Reliability – Honesty – Caring – Trustworthy – UK-Based Staff.

- Life Insurance Coverage From Only £4.15 per month. Yes, cheaper life insurance is a possibility.

- Specialist Life Cover gives your family protection without straining your bank balance.

- Excellent customer reviews for customer service. We’ll help you get the cover you want today.

- Non-discriminatory rates are provided for smokers and vapers

- Are you looking for joint life insurance coverage? Multiple life insurance policies can be easily arranged

Can You Get Life Insurance If You Are a Smoker?

If you are a person who smokes regularly, it is possible to get life insurance.

A premium is likely higher than a standard insurance policy, reflecting the increased health risks of lung cancer, other cancers, heart attack and profound health implications.

It means you may die younger due to your smoking-related activities compared to a tobacco or vape-free adult.

Life insurance companies have different ways of classifying someone who smokes than a non-smoker.

The aim is to implement a policy that accurately reflects your habit to minimise any risk of a payout dispute with an insurer should you die.

The main difference between life insurance for smokers and non-smokers is the cost and how likely you will be accepted for cover.

Although rejection is uncommon, insurers will look at pre-existing health conditions related to your smoke-related activities.

Why You Should Consider Life Insurance as A Smoker

Smoker’s life insurance provides a financial lump sum for your dependents should you pass away and is funded by paying monthly pre-defined premiums throughout a life policy.

If you have any of the following financial commitments, which your loved ones may struggle to pay if you die, then you should consider life insurance:

- An outstanding mortgage or equity release loan

- Unsecured personal loans

- Credit card debt

- Childcare or other education fees

- No savings

- One family income

Who Do Insurers Classify as A Smoker?

An insurance company will classify someone who smokes as anyone who has smoked or used nicotine replacement products like nicotine patches within the last twelve months.

Depending on the life insurance provider, a classification for someone who smokes can exist for up to five years after stopping.

Some insurance companies are willing to look at how much you smoke. There is a thin dividing line between classification as a full-time and an occasional smoker for life insurance purposes.

Compare Life Insurance For Smokers Quotes >> 60 Second Form

The table below compares Term and Decreasing Term coverage costs for smokers. The quotations are based on £100,000.00 of cover over 20 years.

| Age | Level Term (20-year term for Smokers) | Decreasing Term (20-year term for Smokers) |

|---|---|---|

| 20 | £4.15 | £3.49 |

| 25 | £5.14 | £4.25 |

| 30 | £6.97 | £4.96 |

| 35 | £10.01 | £6.32 |

| 40 | £14.26 | £9.58 |

| 45 | £22.84 | £14.63 |

| 50 | £38.68 | £27.61 |

Classification of Smokers by Insurers

| Criteria | Classification |

|---|---|

| Cigarettes | Smoker |

| Cigars | Smoker |

| Vapes/E-cigarettes | Smoker |

| Nicotine Replacement Products (e.g., patches, gum) | Smoker |

| Time since last use | Typically, 12 months to be considered a non-smoker, but it can vary up to 5 years. |

Tips for Securing Affordable Life Insurance for Smokers

| Tip | Explanation |

|---|---|

| Compare Quotes | Find the most affordable life insurance by comparing quotes from different insurers. Insurance Hero can simplify this process for you. |

| Quit Smoking | Reducing or quitting smoking can help lower life insurance premiums. |

| Be Honest | Always be open and honest about your smoking habits during the application process. |

| Apply Sooner | The younger and healthier you are when you apply, the lower your premiums will be. |

| Consider Over 50 Plans | Compare quotes from different insurers to find the most affordable life insurance. Insurance Hero can simplify this process. This is an excellent option for life insurance for smokers over 50. We discuss coverage for the over-50s in more detail below. |

| Use Resources for Quitting | NHS and other UK organisations offer support for those looking to quit smoking. |

Is Vaping Classed as Smoking for Life Insurance?

As mentioned in the table above, if you vape with e-cigarettes regularly, you are considered a smoker by underwriters, even if you use e-liquid that is non-nicotine based.

Vaping, like cigarette and tobacco consumption, depending on insurance companies, can also result in your premium classification and smoker life insurance rates staying in place for up to five years from when you stop vaping and certainly for a minimum of twelve months.

How much more is life insurance for smokers?

The life coverage cost difference between someone who smokes and a non-smoker is not as marked as you may think.

There will be an increase in premiums if you are someone who smokes; however, if you are young, in your twenties, and smoke ten cigarettes a day, the premium increase is quite negligible.

Someone in this age category can expect to pay around £4-6 a month in premiums, with a similarly aged non-smoker paying around £3.51 a month.

Insurance companies look at the likelihood of you dying from your smoking-related activities.

The number of cigarettes smoked a day, the length of time you have smoked, and your age at the time of applying will all be factors in determining premiums.

If you are someone who smokes and is aged 50 when applying for life coverage, a quote is likely to be double that of a non-smoker. It may start at £40 a month, depending on the extent of your smoke-related activities.

How Can Insurance Hero Help?

Insurance Hero is an independent broker with experience providing term life insurance for smokers. We have relationships with underwriters specialising in offering cover to those in higher-risk insurance categories.

As an independent broker, we compare the best life insurance quotes from many underwriters, ensuring affordable life insurance for smokers and one that closely aligns with your circumstances.

If you have stopped smoking, we can also help you put a non-smoking life cover in place after twelve months of being habit-free.

Compare The UK’s Top 10 Insurers for Smokers. Find the Best Policy & Save Money Today

What Is the Best Smokers Life Insurance?

The best life insurance policies are not just those with the most competitive premium quotes. The best insurance for smokers’ life policy closely aligns with your smoke-related activities.

A close alignment is essential because it reduces any possibility that a lump sum payout is withheld due to discrepancies in a smokers life insurance policy quote’s accuracy over your activities and personal circumstances.

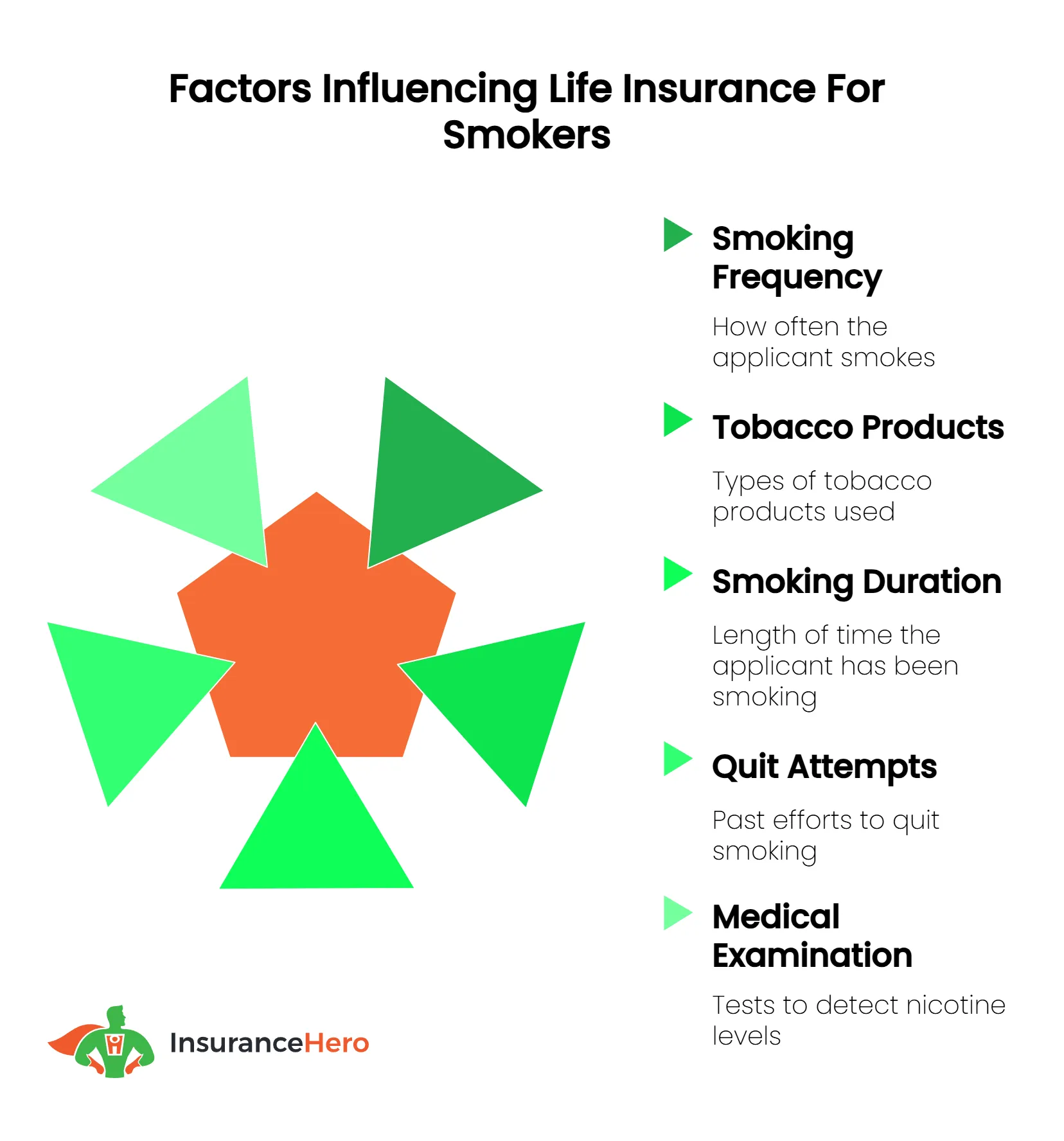

What are the key questions insurers will ask about Smoking?

When contemplating smokers life insurance, you must answer questions honestly regarding the extent of your habit.

Underwriters can request that you undertake a cotinine test if a pre-policy medical is required. The test is how life companies know if you are someone who smokes.

Typical questions you will be asked as part of a fact-finding questionnaire regarding your smoking activities can include the following:

- What type of nicotine or tobacco products do you use?

- How many cigarettes or vapes do you get through a day?

- Do you have any pre-existing health conditions resulting from your habit?

- How long have you been a smoker?

What Happens If You Stop Smoking After You Get Life Insurance?

If you stop smoking after starting a plan as a smoker, you will not see an immediate reduction in premiums.

As mentioned, depending on the insurer, an adverse status can be retained for up to five years once you stop a habit.

You must advise your insurer when you stop smoking. Sometimes, once you stop, it is worth checking quotes from other insurers to see if it is possible to reclassify as a non-smoker.

What Happens If You Start Smoking After You Have Life Insurance?

If you have a standard non-smoking life insurance policy, it is crucial to advise your insurer if you start a habit, as it will affect the terms of the plan and the cost of cover.

Suppose you should die from smoking-related activities, having failed to advise your insurer of your habit. In that case, it may invalidate any payout due to your loved ones being named beneficiaries on your life cover plan.

The bottom line is that quitting cigarettes will have a real financial upside in the long term, not to mention the benefits to your health.

If you took out life insurance when you were a smoker, you could request a review of your premiums due to a change in circumstances, provided you’ve been smoke-free for at least one year.

Not all insurers will lower the premiums, but it’s certainly worth asking because you could very well find that you can save substantially on your life insurance premiums.

Can You Be Denied Life Insurance If You Smoke?

No, you can’t be denied life insurance if you smoke. However, life insurers can charge you higher premiums and deny coverage for other health problems.

All life insurance companies use your risk pool to determine your eligibility for coverage and premiums.

That is the likelihood of your death before receiving all benefits. Insurance companies compare smokers’ life expectancy with non-smokers when determining how much to charge for life insurance premiums.

As most people realise, smoking can affect your health, leading to conditions such as cardiovascular disease.

Do You Have to Tell Life Insurance Companies If You Start Smoking?

No, you do not have to tell your life insurance company if you start smoking.

The insurance company will only consider your smoking if you already have a condition that puts you at risk for certain kinds of cancer or heart disease, or if you have a family history of those conditions.

They will generally not consider your tobacco use if you are healthy.

How Do Insurers Know If You Smoke?

Most insurers ask about smoking as part of the quote or application process. You can add “non-smoker” or “smoker” to your insurance application.

They can also check your medical records. Some insurance companies have recently used lifestyle questionnaires to assess their customers’ risk.

Life Insurance for Social Smokers

The boundary between an occasional smoker and a smoker for life coverage varies among insurers.

In most cases, being a social smoker will not give you a smoker’s classification.

However, if you smoke occasionally, comparing quotes with an independent broker like Insurance Hero is vital to ensure that you are considered for standard terms.

Life Insurance for Smokers Over 40

If you are over 40, the life cover cost will be higher than for a younger smoker, and the acceptance criteria will be more rigorous.

The insurer will likely require additional information on your medical history, possibly from your GP, and a medical examination before being accepted for a plan.

For those over 40 who smoke, it is vital to apply as soon as possible for a life plan. The longer you leave it, the more premiums will escalate in cost.

What About Life Insurance for Other Types of Smoking Activities?

Two other types of smoking activities include cigars and cannabis.

Cigar smoking is another form of nicotine intake, the extent of which will affect the level of premium. Again, there is a blur between what is classified as social and regular smoking.

Cannabis, although a form of smoking, is classified as recreational drug-taking. Subsequently, you will need to declare cannabis use when you complete an application form.

Failure to disclose recreational drug-taking will void a payout should you die from drug-taking activities.

What About Smokers Critical Illness Cover?

Many life policies include critical illness cover as add-on protection for your life plan or a stand-alone policy. Critical illness pays out a lump sum should you no longer work following the diagnosis of a critical illness.

For smokers, thorough medical screening, including a chest x-ray, is often an essential step to be accepted onto a policy.

Over 50s Life Insurance for Smokers

- Designed specifically for men and women aged 50 to 85, this type of life insurance provides lifetime protection with no medical exams required.

- UK residents within this age range are guaranteed acceptance, making it a straightforward option for people looking to secure coverage later in life.

- Although some providers may ask whether you smoke, not all do.

- Once the initial waiting period of 12 to 24 months has passed, a guaranteed payout is made upon your passing. The amount can reach up to £20,000, depending on factors such as your budget and personal situation.

- This cover can ease the financial burden on your loved ones by helping with funeral expenses or offering a modest inheritance.

Insurance Hero offers competitive premiums tailored to smokers, making this type of plan more accessible.

How Does Smoking Affect Life Insurance for Joint Policyholders?

One way that smoking affects life insurance is through joint life insurance policies. When two people are insured under the same policy, both people’s health histories are considered when determining premiums.

In addition, many insurance companies offer a discount to a person with a non-smoker status. As a result, being a smoker can significantly impact the cost of a joint life insurance policy.

| Key Points | Details |

|---|---|

| Smoking Statistics in the UK | Over 9 million people in the UK smoke, leading to nearly 100,000 smoking-related deaths annually. |

| Life Insurance for Smokers | Life insurance for smokers is available and might be more affordable than anticipated. It provides financial security for families in case of early death due to smoking-related illnesses. |

| Classification of Smokers by Insurers | Insurers classify someone as a smoker if they have smoked or used nicotine products within the last twelve months. This classification can last up to five years after quitting. |

| Importance of Life Insurance for Smokers | Smokers should consider life insurance if they have financial commitments like mortgages, loans, debts, childcare fees, or a single income family. |

| Vaping and Life Insurance | Insurers often classify vapers as smokers, even if they use non-nicotine-based liquids. This classification can impact premiums for up to five years after quitting. |

| Cost Difference for Smokers | Life insurance premiums for smokers are higher than for non-smokers. Factors such as the number of cigarettes smoked daily, duration of smoking, and age at the time of application influence the premiums. |

| Insurance Hero’s Role | Insurance Hero is an independent broker that helps find suitable life insurance for smokers, considering their specific circumstances and needs. |

| Questions Insurers May Ask | Insurers may inquire about the type of nicotine products used, daily consumption, pre-existing health conditions related to smoking, and the duration of the smoking habit. |

| Changes in Smoking Status After Getting Insurance | If one quits smoking after getting a policy, premiums may not immediately decrease. However, if one starts smoking after getting a non-smoking policy, it’s crucial to inform the insurer. |

| Life Insurance for Various Smoking Activities | Insurers consider cigar smoking and cannabis use differently. Cigar smoking can be classified based on frequency, while cannabis use is seen as recreational drug use, which must be disclosed during the application. |

Smokers Life Insurance Summary

Suppose you have read this smoker life insurance guide and are a smoker or vaper considering life insurance.

In that case, you should be heartened that, although premiums are higher than for a non-smoker, a proficient broker focuses on cost and establishing a watertight policy.

It means that, should you die, having a plan that closely matches your smoking activities means your loved ones will get the financial payout they deserve.

Suppose you’d like to explore more life insurance guides. In that case, our website offers various resources to help you learn more about life insurance specific to your job, health condition or personal circumstances.

Nobody likes to think about their death, but it’s essential to consider it. No one knows when their time will come, so it’s best to be prepared.

Smoking life insurance can give you and your loved ones peace of mind, knowing they will be financially secure if something happens to you.

We can help you find the right life insurance policy for your needs to live a longer, healthier life with the people you love. Get a no-obligation-free life insurance quote today, and let us help you protect your loved ones.

Life Insurance For Smokers UK Case Study:

The Thompson Family is looking for life insurance quotes for smokers

Meet Jake and Melissa Thompson, a young couple living in East London with their two kids, Emma (age 6) and Sam (age 3). Jake is a full-time accountant, while Melissa is a stay-at-home mum.

Jake has been an occasional smoker since his university days. Even though he tries to limit his smoking habit, he’s always worried about his family’s financial security in case anything should happen to him. After a lengthy discussion with Melissa, they decided to consider their life insurance options.

One major concern they shared was, can you get life insurance if you smoke? After some research, they discovered that insurance providers offer coverage for smokers, although the premiums are typically higher.

This fact led them to the following crucial question: How much more is life insurance for smokers?

Their search led them to a handful of insurance providers offering what they claimed to be the cheapest life insurance for smokers.

However, Jake and Melissa wanted to ensure they got the most affordable option and the best coverage.

Their goal was to find the best life insurance for smokers that could provide sufficient coverage while fitting within their budget.

After comparing various options with help from the Insurance Hero team, they reviewed a plan offering affordable life insurance for smokers.

The company had good reviews, and customers liked the policy’s structure. However, it was not the absolute cheapest life insurance for smokers.

Still, it offered better coverage, including critical illness coverage and a feature that allowed Jake to increase his coverage if his health improved or if he quit smoking.

Finally, they felt relieved when they realised they could get cheap life insurance for smokers without compromising the quality of coverage.

Jake now has peace of mind, knowing his family would be financially secure if anything should happen to him.

Melissa feels the same, acknowledging that the insurance provides financial security for their children and her dependent father.

Their life insurance policy provides a safety net for Jake’s smoking habit. It ensures the continuity of their children’s education, the care of Melissa’s father, and the stability of their family’s financial future.

This case emphasises that it’s possible to find affordable life insurance for smokers policy that provides comprehensive coverage without breaking the bank.

The Thompsons’ experience serves as a helpful guide for other young couples navigating the process of securing life insurance, especially for those with a smoking habit.

Although the process may require some research, the peace of mind and security it offers are more than worth it.

Starting in July 2025, Insurance Hero will have a new insurer that treats vapers differently from tobacco smokers.

Research Resources:

- https://www.aviva.co.uk/insurance/life-products/life-insurance/life-insurance-and-smoking/

- https://www.nhs.uk/common-health-questions/lifestyle/what-are-the-health-risks-of-smoking/

- https://ash.org.uk/resources/local-toolkit/datacostcalculators

- https://www.ons.gov.uk/peoplepopulationandcommunity/healthandsocialcare/healthandlifeexpectancies/bulletins/adultsmokinghabitsingreatbritain/2021#

Steve Case is a seasoned professional in the UK financial services and insurance industry, with over twenty years of experience. At Insurance Hero, Steve is known for his ability to simplify complex insurance topics, making them accessible to a broad audience. His focus on clear, practical advice and customer service excellence has established him as a respected leader in the field.