Best Expat Life Insurance Guide For 2026

A recent study shows more than 13 million British people reside outside its borders, with more than five million permanently domiciled overseas.

More UK residents are living abroad and leaving their home country than 10 years ago, leading to increased demand for expat life insurance.

Residents of one country who live in another are called expatriates, and their reasons for leaving relate to work, education, and personal life. Expats also have life insurance requirements, especially for UK-based financial liabilities such as mortgages.

Key British Ex-Pat Life Cover Benefits, Features, And Criteria

- Life insurance for expatriates, Critical Illness Cover, Whole of Life and Family Income Benefit options.

- Level and Mortgage Decreasing term assurance options and international term life insurance for those living abroad.

- Coverage is provided by a UK-based insurer and priced accordingly, with no cost loading applied.

- The panel includes HSBC, Aviva expat life insurance, and Friends Provident ex-pat life insurance.

- The international life insurance plans we can offer provide financial protection for your loved ones and payout if you pass away.

- Worldwide life insurance cover from £10K to £1.5M. We offer the best price comparison and significant savings.

- Individual & Family Plans.

- International life insurance for expats living in Spain and many other countries

International Life Insurance For Non-UK Residents. Quick Quote Form

Features of International Life Insurance Plan

| Feature | Description |

|---|---|

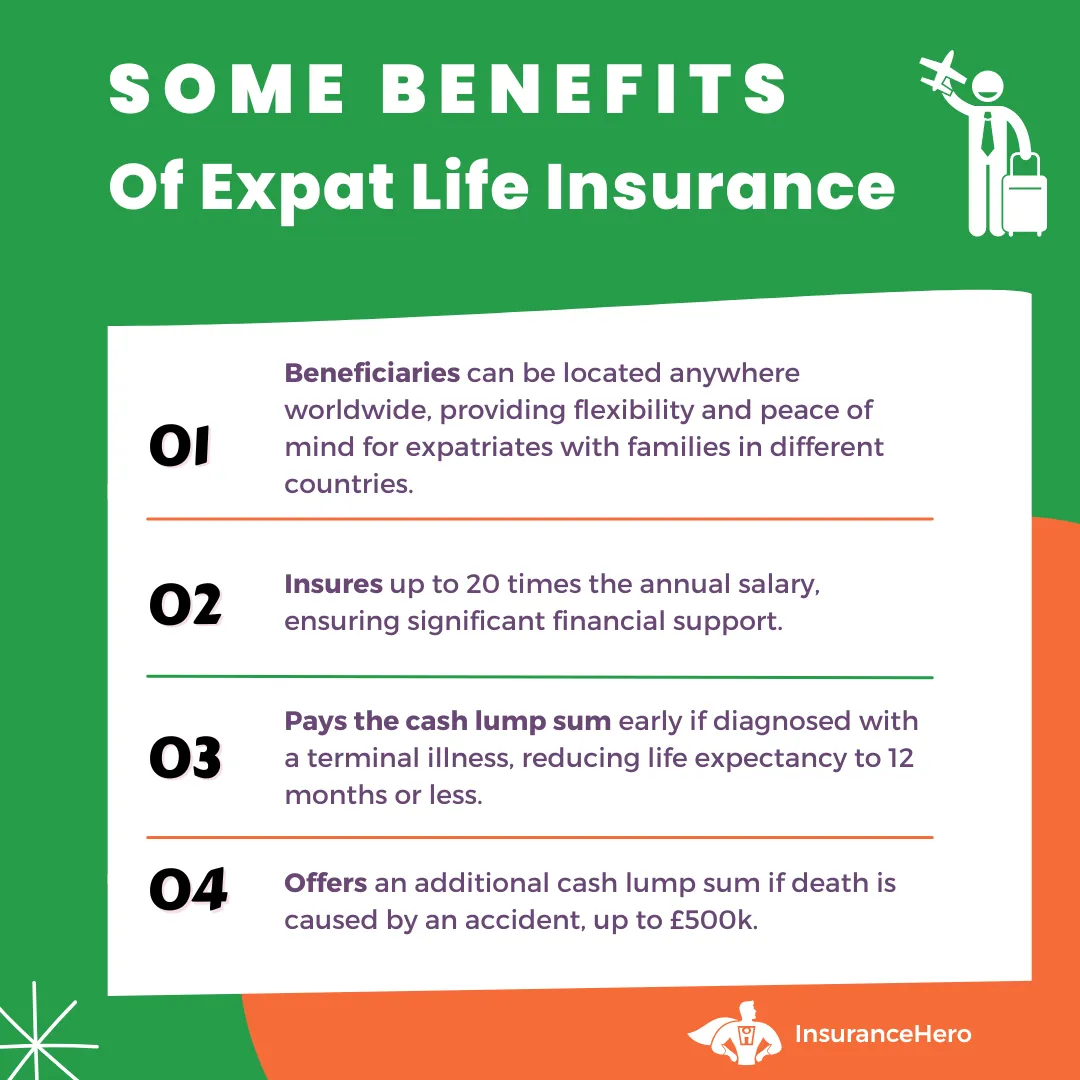

| Financial Security | Provides a cash lump sum to support the family’s living standards or to pay off debts. Insures up to 20x the annual salary. |

| Early Payment for Terminal Illness | Pays the cash lump sum early if diagnosed with a terminal illness, reducing life expectancy to 12 months or less. |

| Optional Accident Benefit | Offers an additional cash lump-sum if death is caused by an accident up to £500k. Also covers serious injury. |

| Dedicated Support | Personal contact for policy help and assistance. |

| Global Beneficiary Support | Beneficiaries can be located anywhere in the world. |

Who Needs Life Insurance?

| Group | Relevance |

|---|---|

| Families | For financial support covering debts, school fees, and funeral costs. |

| Home Owners | Often required by mortgage lenders. |

| Business Owners | Helps pay employees, recruitment fees, and settle debts. |

How Worldwide Life Insurance Works

| Step | Description |

|---|---|

| 1. Choose a Life Benefit | Insure life for up to £1.5m, not exceeding 20x annual earnings. Optional accident cover available. |

| 2. Choose Beneficiaries | Beneficiaries can be anyone important to the insured. |

| 3. Complete Application | Digital application form with medical history declaration. |

| 4. Coverage Commencement | Coverage starts once the plan is agreed upon, usually within 48 hours for eligible applicants. |

If an expatriate is the primary source of income for the family, and he or she dies, surviving dependents will fall into severe financial distress if life insurance cover is not in force.

An employed surviving spouse may need secondary employment, whereas a nonworking spouse may need a job.

If an adult is out of the workforce due to bringing up a child, alternative childcare arrangements become necessary, and these typically come with a high price tag.

It can be even more challenging to cover living expenses such as groceries, utilities, rent, or a mortgage.

Knowing which areas are covered and which are not in your expat life insurance policy is crucial.

| Is It Covered? | Reason of Death |

|---|---|

| Covered: | Common causes of death could include (cancer, accident, heart attack or disease) Death while you’re living and working in another country. Death while in the country you’re a national of. |

| Covered After Twelve Months: | Suicidal death |

| Not Usually Covered: | Dying from a pre-existing medical condition(s). Death due to recklessness, illegal activities, or abuse of alcohol or drugs. Death because of war/conflict or terrorism in a territory, the Foreign, Commonwealth and Development Office (FCDO) states its nationals should not go to. If we have not received a death report within 12 months Passing away while in either Iran, Libya, North Korea, South Sudan, Syria or Yemen |

Worldwide Life Insurance For Those Living Abroad – Some Case Studies:

Mr Yealm, who lives in Singapore and now rents out his residential property in the UK, wanted over 70 term life insurance to cover the £300k mortgage he still has on the property.

Mrs Toms, who retired to Spain with her partner, has an inheritance tax liability in the UK from assets she holds there.

She wanted a UK-based insurer for peace of mind and to benefit from the cheaper cost of UK cover compared to the Spanish alternative.

This is a great example of how life insurance for ex-pats living in Spain is very easily achievable.

Mr Neald wanted to try living abroad and now lives and works in Dubai. He separated from his wife two years ago and has been paying maintenance for his 7- and 9-year-old children.

He wanted some life and critical illness cover if he could not work, so that this could continue to be paid.

For many ex-pats and people working abroad, many insurance companies provide complicated and pricey plans with exclusions.

At Insurance Hero, we prefer to do things more personally. Our insurance policies are flexible to match your new lifestyle, such as the birth of a child or buying a new home.

Life Cover Including Term Life Insurance Plans For Non-UK Residents

Before UK residents move abroad, they should determine whether their life insurance policies will accompany them. If not, they should consider purchasing a new international life insurance policy.

Unstable political conditions make it risky to live in many foreign countries. Even temporarily residing in one of these countries could be dangerous because it can increase health and overall well-being risks.

Insurance for expatriates is a unique cover for individuals brought up in one country but who live and work in a different one. Some international insurance companies offer these policies, but their availability varies based on geographic region.

For example, British expats living in the Middle East have relatively few options regarding providers and policies.

Friends Provident International, Eagle Star International, Scottish Provident International, and Royal & Sun Alliance are the major international insurance companies offering life cover to ex-pats in this region.

An ex-pat may find local cover, but many insurance professionals are wary of this approach. Beneficiaries of ex-pats who die outside of the UK often find it difficult to make claims with insurers local to where the deceased lived.

Experts recommend that expats select an internationally recognised insurance company instead.

Specific Re-locations

After relocating to the Middle East, residents of Britain and northern Europe can find international life insurance policies through Friends Provident at British rates.

Other providers offer investment-linked whole life policies, which are usually a little more expensive but have value upon surrender if the plan is no longer needed.

A UK expatriate relocating to Lebanon, Israel, or other regions may discover that insurance policies do not include war risks.

When living abroad and shopping for cover, people should carefully review the conditions, terms, and exclusions of each available policy and ask questions that arise during the process.

It will prevent unexpected gaps in cover and surprises if a claim becomes necessary.

Existing cover, including benefits for death in service included in employer-provided pensions, should also be reviewed.

The benefits are typically a multiple of the salary, but may not be enough to provide surviving beneficiaries with a comfortable lifestyle.

Flexible Life Insurance For Expatriates International Plans Suitable For Individuals & Families. Get A Quote Today

International Life Insurance (Providers) Companies List Includes:

- HSBC

- Friends Provident

- Liverpool Victoria

- Aviva

- Scottish Widows

- Scottish Provident

- Canada Life

- Standard Life

- Lutine

- Aegon/Scottish Equitable

- Face to Face

- William Russell

- Zurich

What Should A Robust Expat Policy Include?

As we have highlighted in our case studies, expat life insurance can provide essential financial protection for those based overseas in various ways.

A key reason concerns the coverage of financial liabilities within the UK, including outstanding mortgages, dependents, or tax liabilities.

Discussing your circumstances with an international life insurance provider is crucial so that you have coverage for what you need.

Regarding your destination country, your insurer needs to understand the nature of your occupation, country-specific risks, the country’s tax legislation, and any other health and personal risks you may face.

As a rule of thumb, enough cover should be put in place to pay off all your debts should you die overseas.

As part of your fixed-term policy, a separate investment pot should grow in parallel to provide a lump-sum investment for the plan’s designated beneficiaries.

When living abroad, you can also consider income protection insurance for expats, which will protect you if you get sick and cannot work.

Another plan that might interest people who work abroad is a level-term life insurance policy. In this plan, premiums remain the same during the policy term.

Beneficiaries receive a fixed cash sum payout in case of death or other challenging circumstances.

Total permanent disability insurance for ex-pats is a plan to secure individuals in case of permanent disabilities or illnesses that prevent them from working. It might be a good cover for those with high-risk professions.

Specific features that should be part of your international insurance policy include the following:

Repatriation of mortal remains

If an insured person under an expat life insurance policy dies overseas, the body must be repatriated back to the UK if the request is for a home burial.

There may be complicated formalities for the repatriation. Logistical issues also need to be considered. A robust policy needs to include extensive assistance for this critical policy definition.

Full geographical extension

The purchase of international life insurance provides financial protection for your UK financial liabilities and is tailored to your circumstances and needs.

A robust plan should include a full geographical extension for those living overseas. Suppose you work abroad as an expatriate and relocate to further international locations as part of your job.

In that case, your plan will be transportable and allow updates to reflect your new circumstances.

International assistance

Extensive 24/7 multilingual telephone assistance must be part of your international life insurance for expats policy. Access to expert staff when you need it most is essential.

As the insured person, you may have an urgent change in circumstances for which you need guidance. If you die, designated beneficiaries may need immediate advice on issues such as repatriating your body. Choose one of the international life insurance companies that offer such a service.

Child Concierge Service

If you die overseas and have dependents living with you, including children, a child concierge can be essential to provide services, including counselling and bereavement support.

New Cover for 2026

Life insurance benefits are numerous. Financial liabilities, such as an outstanding mortgage or any dependents remaining in the UK as you work abroad, are essential considerations when considering life insurance for non-UK residents.

Additionally, it is crucial to get expert guidance before you take out a policy due to the added complexity of working or living in another country; this includes life insurance for women policies and life insurance after retirement.

The financial peace of mind that comes with having a bulletproof policy is incalculable. Knowing that should you die, there will be no financial burden for your dependents to shoulder is immeasurable.

FAQ: Life Insurance Policy For Non-UK Residents

Can I change the designated beneficiaries on my policy?

You can change, remove, or appoint as many beneficiaries as you like on your policy. A beneficiary designation form must be completed for any updates; the last update on record is considered your current appointment.

Should I get expat life insurance if I already have coverage through my employer?

It may be wise to get private insurance and an occupational plan if your employer offers them.

There are two reasons for this:

- Your occupational cover may not provide enough protection for your needs, especially if you have substantial financial liabilities in the UK.

- If you work overseas as an expat and change employers, your new insurance policy may not be sufficient.

Do I need a medical examination in the UK to get life insurance for expats?

You do not need to return to the UK to undergo medical examinations for life insurance purposes. Most providers will permit the required medical tests in the country where you stay.

The doctor performing the examination might be obligated to speak English to implement a policy.

Do I need a UK address and bank account to get international life insurance?

Having a UK address is not required to purchase expat insurance. However, a UK, Channel Islands, Gibraltar, or Isle of Man bank account is.

Regular insurance premiums paid by direct debit cannot be paid without a UK bank account.

Can a third party own my policy?

A related third party can own your life insurance policy. A relevant party can be your spouse, company, or trust structure. When a third party holds the life insurance for expats plan, they are on record as the policyholder, and you are recorded as the life assured.

How are my international life insurance monthly premiums calculated?

Premiums for expat insurance have additional factors to consider beyond a domestic life insurance policy.

Factors include other health and personal risks you face in the country you stay in. Political stability and whether the country is considered a conflict zone are all additional calculation considerations.

Can my domestic UK life insurance remain valid?

If you work extensively abroad but remain a UK resident as you still reside in the country for more than 183 days a year, your domestic insurance can remain valid.

You will need expat life insurance if you work more than 183 days from the UK and become a resident elsewhere.

If I get divorced, does my life insurance need to change?

When you sign up for life insurance for non-UK residents with many insurers, you agree to inform them of any changes in circumstances. If you get divorced, you may need to reassess your needs in case something bad happens.

Consider life insurance cover for dads or life insurance for single mums, and or read our top 10 life insurance companies charts to get advice about the level of cover that is most appropriate.

Expat Life Insurance – Final Thoughts

If you’re debating whether or not to get expat life insurance, consider whether your employer’s coverage is adequate. If it isn’t, purchasing a policy is a good idea.

Choosing the right life insurance can give you peace of mind, knowing that you and your family are financially protected if something happens to you.

Are you living in Europe, the UAE, or Asia and need cover? We can help! Insurance Hero is an independent price comparison site that helps customers find affordable life insurance coverage for expatriates and their families by comparing rates from top providers.

Life insurance can be a complicated and confusing topic. The good news is that there are many options for British expatriates who want to get life cover abroad.

If you need help finding what might work best for your needs, our team of experts is ready to answer any questions and walk you through all the steps in getting insured (including filling out paperwork).

Insurance Hero has partnered with many companies and can provide valuable insight into your needs and situation.

We would love to help out in any way we can. Let us know if you need assistance finding an affordable policy today.

We offer free consultations, so contact us today if this sounds like something you might need or want more information about.

Does Relocating from UK Invalidate Life Insurance?

Whether you are an expat or considering moving out of the UK for another reason, consider the many consequences. …

What Does Brexit Mean For Expats In The UK And The EU?

Brexit is a word that has been on everyone’s lips for years. It’s a subject that has generated endless debate, sparked h…

Research Data:

- Living abroad (GOV.UK)

This includes tax, state pension, benefits, and UK government services abroad. - Guide To Moving Abroad – Moving Overseas | (HSBC Expat)

Research where you’re going · Check the country or region’s entry requirements · Work out your moving costs - Brits who have moved abroad guide (Reddit)

Steve Case is a seasoned professional in the UK financial services and insurance industry, with over twenty years of experience. At Insurance Hero, Steve is known for his ability to simplify complex insurance topics, making them accessible to a broad audience. His focus on clear, practical advice and customer service excellence has established him as a respected leader in the field.