Best Life Insurance For Over 50 In 2026

Welcome to our best over 50s life insurance guide. If you are over 50, you may wonder whether your financial circumstances will be satisfactory if you die unexpectedly.

Considerations may include whether you can pay for your funeral costs, pay off small loans, or leave your loved ones a financial gift.

If you want to remove any financial uncertainty over your estate, an over 50 life insurance plan can provide financial protection and peace of mind that your affairs will be taken care of should you die.

Unlike some other insurance products, over 50s life insurance policies do not accumulate cash value. This article will explain how over 50s life insurance works and whether it may be relevant to your circumstances.

It’s important to determine how much cover you need based on your circumstances and specific financial needs. Tools like life insurance and funeral cost calculators can help you estimate the appropriate amount of coverage by considering factors such as age, smoking status, and budget constraints.

Looking For The Best Over 50 Life Cover? Compare The Leading Life Insurance Companies Below – 60 Sec Form

Best Over 50s Life Insurance Companies

Life insurance for over 50s provides the option of a tax-free, fixed cash payout, typically between £ 25,000 and £1,000,000, when you pass away.

The funds go to the named beneficiary, typically families, and may be used to pay for funerals or other minor costs.

Unlike standard Life insurance plans, this policy type has no health screening or medical questions.

The money is guaranteed for as long as the payments are made on time. The cash is zero-rated for any capital gains or income tax.

The Insurance Hero team has concluded that the UK life insurance companies listed below were recommended to be the most suitable for life over 50 insurance.

Click the link beneath the table to receive free quotes on your insurance. Remember that the average cost of over-50 life insurance premiums can vary based on your health history and lifestyle, such as whether you smoke or have an ongoing medical condition.

| Company | Plan Name |

|---|---|

| ⭐Smart Insurance | OUR TOP CHOICE – Smart Guaranteed Life Insurance Coverage (For Over 50s) ‣No medical exam required or health questions ‣Flexible policies – make a change without hidden fees ‣Global cover – you get covered in any part of the world ‣Three times your benefit sum up to £60,000 – if death was accidental ‣ A Will Kit is included with all policies |

| Foresters Friendly Society | 50+ Life Cover ‣Bonuses are a possibility ‣Pay only until 85 years of age ‣£35 M&S gift card |

| Sainsbury’s Bank | Over 50s Life Insurance Plans ‣Coverage from only £5 per month, depending on your age ‣£100 of Nectar points † You’ll receive your points within 60 days after you’ve paid 5 months of premiums ‣Entry to Legal & General Wellbeing Support Facilities |

| Onefamily | Over Fifties Life Coverage ‣Defined payments. They guarantee that these won’t increase ‣Guaranteed to be accepted if 50 to 80 years old and UK-based ‣Payment Holidays of up to six months ‣Immediate cover for accidental death within the first year |

| Post Office | Over 50s Life Coverage ‣For UK residents aged between 50 and 80 ‣Include a Funeral Benefit option at no extra charge ‣No medical is needed ‣Level term or increasing coverage |

| Sunlife | Guaranteed Over 50 Plan ‣Guaranteed to be accepted if you’re between 49 and 85 ‣Cash payments up to £18,000 ‣They payout 100% of claims, usually within three days or less ‣Monthly premiums that don’t increase, from £3.70 a month |

| Royal London | Guaranteed Lifelong Protection Plans ‣100% of claims are paid swiftly, often within 3-5 days ‣Coverage duration is for life. After passing 90 or after 30 years, no further payments ‣50% of their customers pay £30 each month or less for over 50 life insurance |

| Aviva | Guaranteed Lifelong Protection Plans ‣100% of claims paid swiftly, often within 3-5 days ‣Coverage duration is for life. After passing 90 or after 30 years, no further payments ‣50% of their customers pay £30 each month or less for over 50 life insurance |

| Santander Bank | Over 50s Life Insurance ‣Life cover from Aviva, the UK’s biggest insurer ‣Monthly premiums don’t increase after the policy has been set up ‣You are guaranteed to be accepted without health questions |

| LV= Liverpool Victoria | 50 Plus Plan ‣Guaranteed to be accepted if residing in the UK ‣Coverage starts from only £7 per month based on your age ‣Entitlement to a free gift card within 30 days of paying your third premium |

What Is Over 50 Life Insurance?

Many people have asked us what the best over 50s life insurance is. This type of insurance is a protection plan for UK residents aged 50 or over, broadly targeting the 50 to 80-year age bracket.

It is a specific life insurance plan initially made famous by SunLife, but it has gained popularity across the life insurance sector.

Definition and Purpose of Over 50’s Life Insurance

This insurance provides a guaranteed cash sum to help cover essential expenses such as funeral costs, outstanding debts, or other financial obligations when the policyholder passes away.

The primary purpose is to offer financial protection and peace of mind to both the policyholder and their loved ones.

By covering unexpected costs, this type of insurance helps alleviate the financial burden during a difficult time.

Who is Eligible?

To be eligible, you must be a UK resident aged between 50 and 80. One of the key advantages of this type of insurance is that the application process typically does not require medical checks or health questions, except for whether you are a smoker.

This makes it an attractive option for individuals who may have had health issues in the past or are concerned about the cost and complexity of traditional life insurance.

With over 50’s life insurance, you can secure coverage without the hassle of medical examinations, making it a convenient and accessible choice for many.

How Does an Over 50s Life Insurance Policy Work?

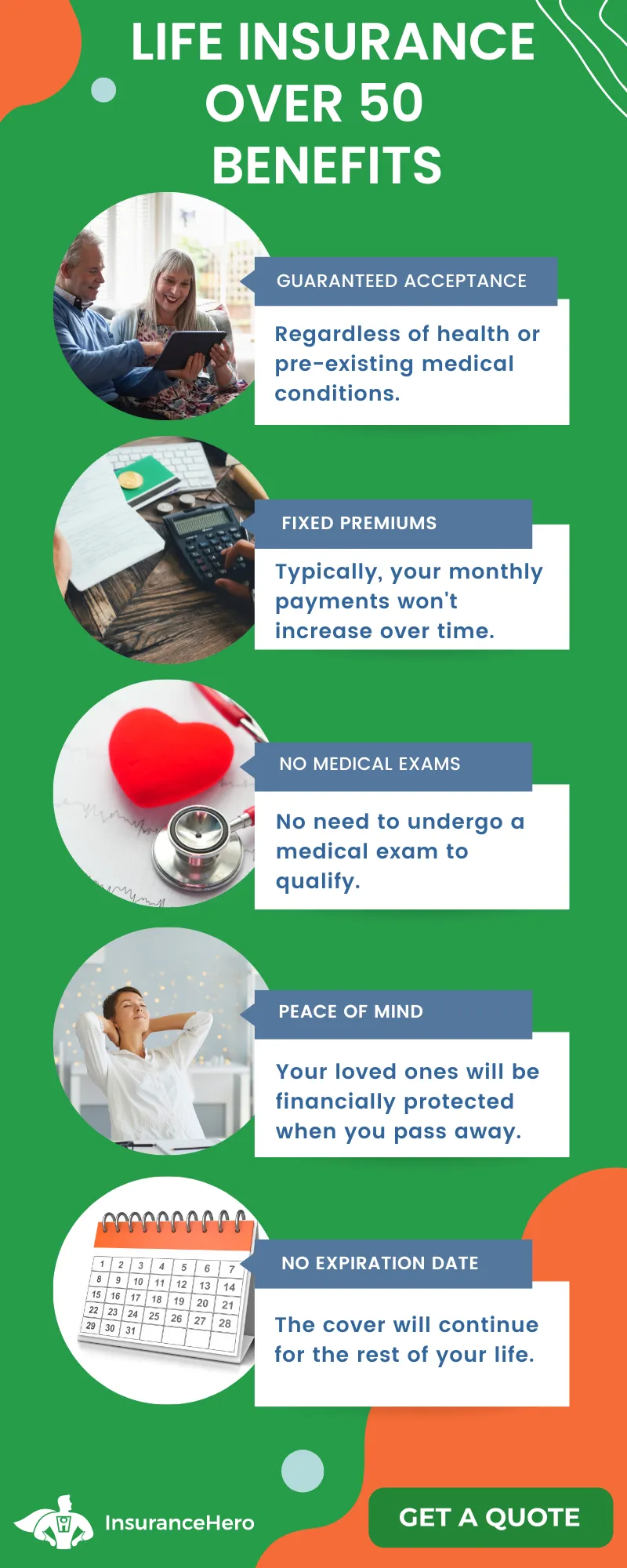

Over 50s life cover works similarly to other life insurance options, with regular monthly premiums required to get cover.

Suppose you are a UK resident, and you pass away. In that case, the life insurance provider will provide a financial cash sum to the family or other designated beneficiaries if the nature of your death meets the policy terms and conditions.

How to Apply

To get started, you can obtain a quote by providing some basic information, such as your name, date of birth, and address. You will also need to decide on the level of cover you require and the monthly premium you are willing to pay.

Once you have chosen your plan, you can apply online or over the phone. One significant benefit is guaranteed acceptance, provided you meet the age criteria.

This means you can secure your life insurance policy without worrying about being declined due to health issues.

How Does Over 50 Life Insurance Differ from Traditional Life Insurance?

As previously mentioned, Over 50 life insurance plans do not require a pre-policy medical for insurance cover to be provided. It is a policy known as guaranteed acceptance, as your physical and mental well-being do not affect your eligibility.

Since pre-existing medical conditions do not need to be declared, the cash payout from an over 50s life cover policy is much smaller than that from traditional insurance, which requires medical screening.

In return for guaranteed acceptance insurance, insurers typically cap the cash sum amount at between £20,000 and £30,000, depending on the insurer.

Subsequently, the funds paid out are intended for smaller financial obligations, not significant commitments such as repaying a mortgage or paying an inheritance tax bill.

If I am over 50, why should I Consider Life Insurance?

If you are over fifty, life insurance may serve a different purpose than younger people, who will often get cover against an outstanding long-term debt, typically a mortgage.

For over 50s who may be established in their own home, likely reasons for taking out life insurance are the following:

Funeral expenses

If you should die suddenly, your family may be unable to pay your funeral costs. A lump-sum payout can help cover funeral costs.

While over-50s life cover usually doesn’t include specific funeral benefits, some policies also include an additional funeral plans payment if your loved ones use the insurer’s recommended funeral director.

To discover more about the differences between over 50s and funeral plans, please read our over 50 life insurance vs funeral plans guide.

Pay off outstanding debts

If you die, will your family likely be responsible for paying off your outstanding financial obligations?

A lump-sum payout from a policy can help pay off personal loans, credit cards, and store cards. It will provide the financial peace of mind that your financial affairs will be all in order when you pass away.

Charitable donations

The cover can serve a purpose beyond just financial protection. When you die, a sum of money could be donated to a favourite charity or worthy cause close to your heart.

Financial gifts for loved ones

You may have children, grandchildren, or other loved ones if you are over fifty. It can be a nice gesture to leave a financial gift from a life insurance policy.

A beneficiary can use a monetary amount for any purpose, such as helping pay for higher education or purchasing a car.

Very low cost

An over 50s life insurance policy is very low cost, as the cash sum payout is much lower than in traditional life insurance, typically capped at £30,000.

Subsequently, a policy can provide financial security for as little as £6 a month, ensuring your monetary affairs are in order when you pass away.

Employer cover may be coming to an end.

If you are over 50, retirement from your job may be on the horizon. As part of your employment contract, there may be a death-in-service benefit.

A life insurance policy would ensure that cover continues in a private capacity when you leave the workplace.

Features Of Life Insurance For The Over 50s Include:

- Comprehensive critical illness cover is available

- Great terms for all age groups – not just over 50-year-olds

- Life cover for those divorced or separated

- Policies for UK ex-pats

- Cover for mortgage payments

- Over 50 life insurance with no medical exam

- Some policies include well-being services such as mental health support, nutritionists, and health checks.

What Should You Expect To Be Covered?

Guaranteed acceptance

A policy should be guaranteed to be accepted for an over-50s life insurance plan. This means that the insurer does not consider pre-existing medical conditions, even for smokers, and no medical examination is required.

A payout guarantee

Typically, a payout guarantee means a sum of money pays out as long as you have paid at least 50% of the monthly payments.

The calculation is made from the policy start date to the policy anniversary date after your 90th birthday.

A cease of premium limit

A reputable insurer will allow a policyholder to stop making monthly payments after reaching a certain age, while remaining covered. The period varies between insurers but is usually from 85 to 90 years of age.

Flexible payments

Have you been searching for the cheapest life insurance for over 50? Suppose you face financial hardship and are at risk of missing a payment.

In that case, reputable insurers will allow a reduction in monthly payments as long as you maintain a minimum payment and continue to pay.

It ensures your policy remains active and that any payout remains valid.

Immediate accidental death cover

Insurers offering cover will often include accidental death coverage in the first year of the policy. Other causes of death do not result in a payout in the first year of a new policy.

Full insurance cover after a year

A reputable insurance provider will payout after the first full year of paying into a new life insurance plan, as long as you do not miss a payment or stop paying.

Although not common, any provider that extends this payout period beyond the first year should be avoided.

Funeral benefit option

Many insurers offer a funeral benefit option that includes additional payment to help pay funeral costs. A specific funeral director is often required when a funeral plan option is included.

How Can I Compare the Best Over 50 Life Insurance Policies?

When considering life insurance for the over 50s, you must compare policies like-for-like. It must be judged against other over 50 life insurance, not traditional life insurance, which requires medical screening.

The best life insurance policies are not always the cheapest, but they are plans that, once implemented, align with your circumstances.

Key Considerations

Important areas for consideration form the basis of a robust policy. Below is a list of the key points you should consider before taking out an over 50s life insurance policy.

How long do you need the cover for?

The reason why you are taking out insurance in the first place should dictate how long you need coverage.

For example, if you are an older parent, you might plan to ensure that your children can still afford to finish their education if something happens to you.

How can I work out how much life insurance I need?

Calculating the amount of coverage you need involves considering several factors.

Here is a step-by-step guide to help you determine the appropriate coverage:

- Evaluate your mortgage balance: Determine the remaining balance on your mortgage. Although over-50 life insurance plans have coverage caps (usually around £20,000), a payout could help keep your family in their home.

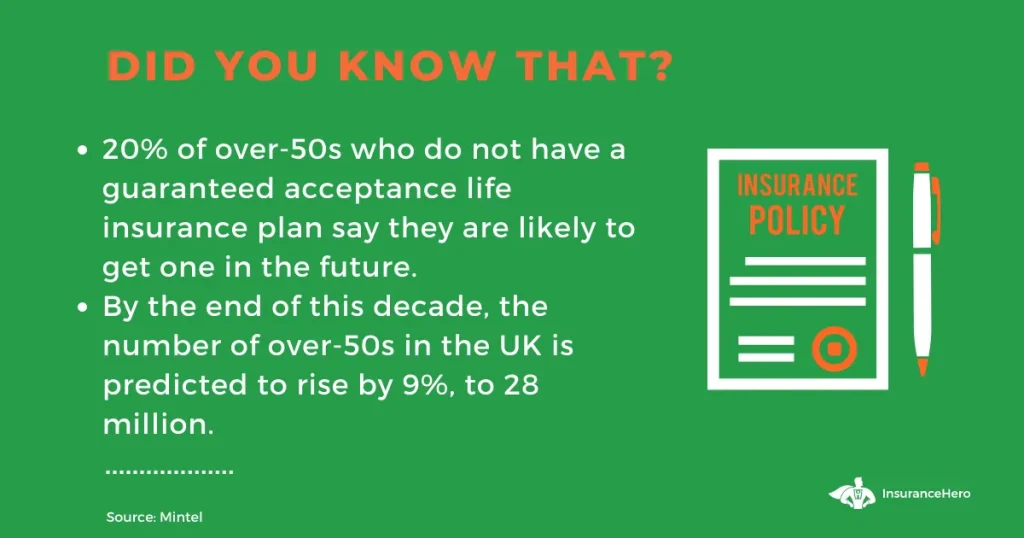

- Assess your debt: Consider any outstanding loans, credit cards, or other personal debts you currently have. Research suggests that many over 50s owe money on credit cards and loans, with average debt totalling around £12,000. While over 50 life insurance plans may not cover the total amount, they can assist in paying off some of your debts.

- Calculate the cost of your funeral: The average cost of a basic funeral is approximately £3,952, with the overall cost of dying reaching around £9,300. Life insurance can help cover these expenses, providing financial support to your loved ones during a difficult time.

- Plan for your partner’s retirement: Consider their financial situation, especially if they rely on their pension for income. Life insurance can provide an additional financial cushion for your partner, ensuring they have support beyond their pension.

- Consider leaving an inheritance or making a charitable donation: Consider leaving a cash gift to your loved ones. Alternatively, you may want to allocate a portion of your payout to a charitable organisation with personal significance.

- Account for existing insurance, funeral plans, or savings: If you already have life insurance coverage, a funeral plan, or personal savings, factor these into your overall coverage estimate. By considering existing financial protection and savings, you may be able to reduce the level of coverage needed and potentially save some money.

What is the cost of cover?

The cost of cover refers to the monthly premiums you pay into a policy, corresponding to a certain payout level.

For a small payout to cover funeral costs, the cost of life cover may start at £6 a month.

What is the maximum entry age limit?

Insurers will set a maximum age for policyholders. An over 50s life insurance plan is typically 80 years old, although this can range slightly lower or higher depending on the insurer.

What is the claims process?

When selecting a particular insurer’s policy, it is prudent to consider how long it takes to pay out once a claim is made.

The claims process is available in the policy terms and conditions. If additional comfort is required, it is worth considering the insurer’s payout level, expressed as a percentage; a higher payout is preferable.

Insurance Hero is a leading independent life insurance broker with extensive experience providing life insurance to older people. Contact one of our friendly yet professional staff on 0203 129 88 66 for a no-obligation quote tailored toyour circumstances.

I Need A Higher Level Of Life Cover- Are Other Options Available?

If you are over 50 and require a more substantial level of life cover than is available under an over 50s life insurance plan, you may have to look at other life insurance products.

Two scenarios where this may apply are to provide cover for an outstanding mortgage or to ensure sufficient funds are in place to pay an Inheritance Tax Bill.

Mortgage Repayment

If you are over 50 years of age, you may have decided to take on a new mortgage, equity release, or another type of secured borrowing.

Such a significant financial obligation will require a protection policy. The debt is repaid in full should you die, and dependents are not left with an estate saddled with creditors.

Inheritance Tax

If you are a UK resident and have a substantial estate that you will pass on to your family, there will be an inheritance tax bill to pay to the UK government.

A life insurance policy can be tailored to pay off an IHT bill when you die, so the beneficiaries inherit your estate free and clear of debt.

If you have significant financial commitments, there are two life insurance options that you will need to consider.

Fixed-term insurance

Fixed-term life insurance is the most common life insurance product for people over 50, whereas for younger policyholders, it typically covers a mortgage.

It is available for the over fifties, but as a traditional life insurance product, it may require a stricter medical examination and the disclosure of pre-existing medical conditions to be accepted for a policy.

Term life insurance provides insurance coverage for a set duration, meaning once the policy expires, no payout will be due should you die.

As mentioned, fixed-term insurance is typically used in conjunction with a mortgage or a fixed-term loan, such as equity release, meaning that if you pass away, the debt is repaid in full.

Other uses for fixed-term insurance include paying an Inheritance Tax Bill or covering the cost of private or further education for your children.

Whole-of-Life Insurance

Whole-of-life insurance is the most costly insurance type, especially if you are over 50. Full medical screening and the disclosure of medical conditions are mandatory to be considered for this insurance product.

Unlike term insurance, where a policy lapses after a fixed payment term, whole-of-life does not have a fixed duration and will continue until you die, whenever that is.

Like term insurance, whole-of-life policies typically aim to cover significant financial obligations should the insured die.

Both term and whole life insurance become increasingly expensive as you get older, as there is a higher risk of something happening to you than to a young and healthy policyholder.

The cost may be higher for those over 50, but you should not let this deter you. It is still crucial to look around, as specialist insurers offer competitive life insurance quotes.

How Can Insurance Hero Help You?

Insurance Hero is an Independent Life Insurance Broker with extensive experience getting cover for the over 50s and for those entering into retirement.

Insurance Hero does not align with a particular provider but works with an extensive network of specialist underwriters.

We know the application and claims processes intimately to ensure those over 50 have the best policy aligned with their circumstances.

The Importance Of Healthy Living For The Over 50s

Here are a few suggestions:

- Maintain A Balanced Diet: Incorporate plenty of fruits, vegetables, lean proteins, and whole grains into your daily meal plans. Stay hydrated and limit saturated fats and processed foods.

- Regular Exercise: Exercise is key to keeping your body and brain healthy. This can include brisk walking, swimming, weight training, yoga, or dancing.

- Regular Health Check-ups: Routine screenings for blood pressure, cholesterol levels, and other potential health issues can help you manage your health better and prevent major illnesses.

- Mental Stimulation: Keep your brain exercised with puzzles, reading, writing, or learning a new language or skill to help prevent cognitive decline.

- Adequate Sleep: Lack of sleep can contribute to various health problems, like memory issues and obesity. Aim for 7-9 hours of sleep per night.

Our healthy ageing tips for those 50 or over guide offers many more actionable suggestions.

If you are over 50 years old, you may already be a homeowner, you may take out life insurance to clear small debts, leave a financial gift, or cover your funeral costs.

Of course, if your needs are more substantial, such as paying off inheritance tax, a policy that requires medical vetting rather than guaranteed acceptance will be more relevant.

In all cases, it is essential to be clear about why you are taking out insurance and then use the services of a reputable broker to ensure that any policy closely aligns with your circumstances.

In many cases over 50 life insurance with immediate cover is available without a medical. Is life insurance worth it after 50? We certainly think so and welcome any questions you might have.

Steve Case is a seasoned professional in the UK financial services and insurance industry, with over twenty years of experience. At Insurance Hero, Steve is known for his ability to simplify complex insurance topics, making them accessible to a broad audience. His focus on clear, practical advice and customer service excellence has established him as a respected leader in the field.