Life Insurance With High Blood Pressure

Can someone with high blood pressure get life insurance? The simple answer is yes.

We work with UK insurers that offer life insurance to those with high blood pressure. If you die, the insurer will pay your family a lump sum. This payment can help cover essential costs, such as funeral expenses or mortgage payments.

Can you get life insurance cover with high blood pressure?

Yes, you can get coverage if your condition is well-managed with treatment; your application is likely to be approved without issues. Depending on your overall health and medical history, you may even qualify for standard rates.

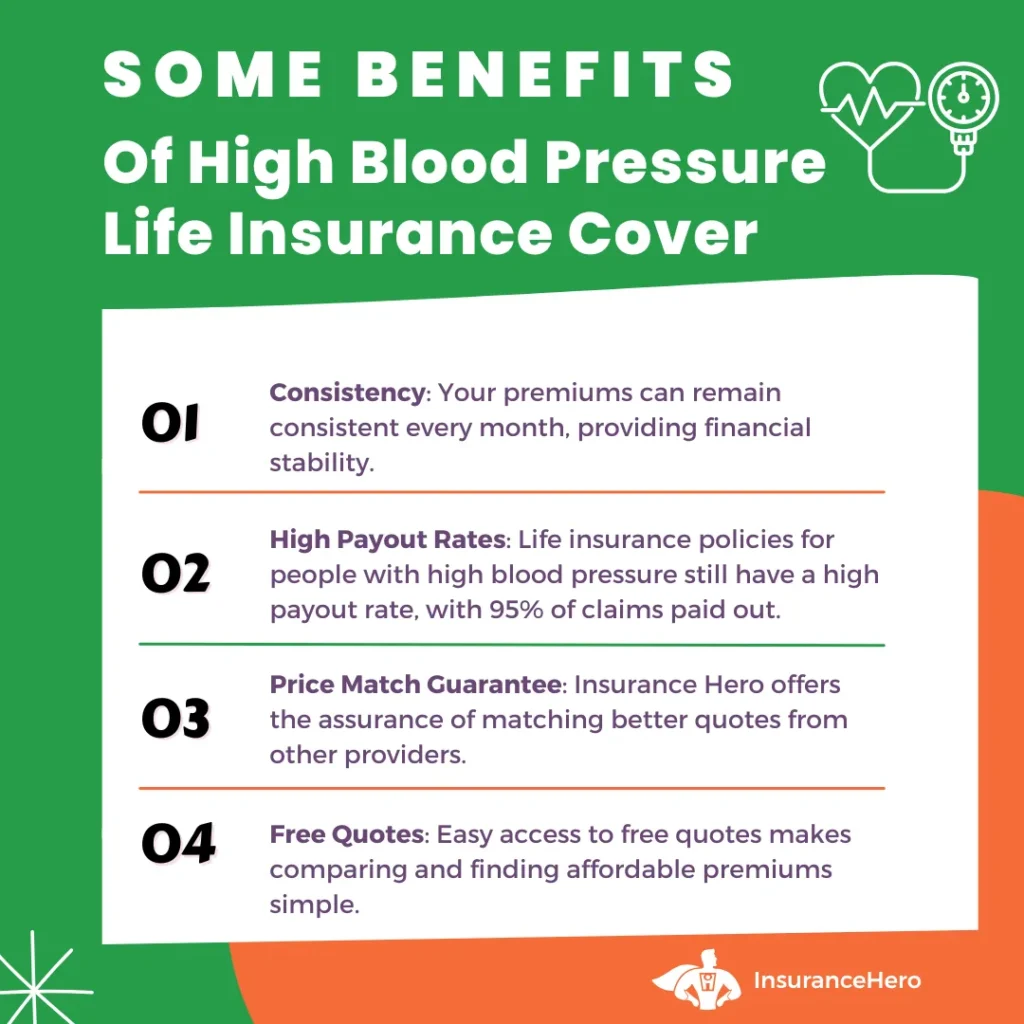

High Blood Pressure And Life Insurance Summary:

This page, compiled by our medical life insurance specialists, provides up-to-date insights on purchasing high blood pressure life insurance cover.

Here’s why you should consider working with us:

- Clarity and Confidence: Getting life insurance with hypertension through general providers can sometimes be difficult. That’s why it helps to speak with a specialist who understands heart-related applications.

- Straightforward Process: You can apply with confidence. Our team handles all inquiries privately and securely.

- Tailored Options: We work with insurers who offer life cover to people with high blood pressure, especially when it’s well-controlled, and there are no other significant health issues.

Compare Life Insurance Quotes For People Living With High Blood Pressure – 60 Second Form

What is considered high blood pressure?

In the UK, blood pressure readings of 140/90 mmHg or higher are typically considered high for life insurance purposes. Insurers use this benchmark to assess health risk during applications.

Impact on Life Insurance

- Eligibility: High blood pressure doesn’t automatically prevent you from getting life cover, but it may affect the policy terms and premium.

- Control: If your condition is managed effectively with medication or lifestyle changes, you may still qualify for standard rates.

- Severity: Readings over 180/110 mmHg are considered severe and can result in higher premiums or restrictions.

- Other Health Issues: Conditions like diabetes, obesity, or high cholesterol may increase your risk profile.

- Recent Diagnoses: If your condition was diagnosed recently and isn’t stable yet, insurers might delay approval.

How to Improve Your Chances

- Keep blood pressure in check through regular monitoring and treatment.

- Follow a healthy routine: exercise, a balanced diet, limit alcohol, and avoid smoking.

- Be accurate and complete in your medical disclosures.

- Work with a specialist broker like Insurance Hero for complex health needs.

- Managing your condition effectively can improve your chances of getting affordable life cover.

| Blood Pressure Ranges | Systolic Reading (pressure in the arteries) | Diastolic Reading (resistance in blood vessels) |

|---|---|---|

| Lower than normal | Below 90 | Below 60 |

| Healthy range | 90 – 119 | 60 – 79 |

| Raised (pre-hypertension) | 120 – 139 | 80 – 89 |

| High blood pressure (hypertension) | 140 or above | 90 or above |

According to a report by Age UK, “21% of older men and 23% of older women have controlled hypertension; the rest are uncontrolled or untreated.“

Kantar – a data and insight company – reports that “…the prevalence of hypertension in the UK is 32%”. That’s a high number, in essence, putting a third of the entire British population at risk of severe heart disease.

Why the jump from high blood pressure to serious heart disease?

There is a link. The British Heart Foundation does not mince its words when it states:

“High blood pressure isn’t usually something that you can feel or notice, but if you have it, you’re more likely to develop coronary heart disease or have a stroke”.

The bolded parts in that statement are where your life insurance policy must be covered. The British Heart Foundation recommends that everyone over the age of 40 have their blood pressure checked regularly by their family GP or community nurse.

The earlier high blood pressure is diagnosed, the sooner steps can be taken to reduce it. However, medications aren’t always required, as lifestyle changes have a significant impact on heart health.

Regular exercise, dietary controls, especially cutting back on salt, and lowering alcohol intake are all ways to lower blood pressure.

A Recent Case Study (With Costs):

| Details for the person seeking cover | Life insurance with a history of high blood pressure |

|---|---|

| Age and whether they smoke or vape? | Born in 1984, doesn’t smoke or use e-cigarettes |

| Bodyweight and height | 5ft 8in tall / Weighs 13stone and 5lbs |

| Health background | Diagnosed with hypertension within the past 4 years |

| Amount of coverage required | £470,000 – Family protection policy |

| Policy term | 35 years |

| Type of premium | Fixed (guaranteed) monthly premiums |

| Monthly Cost | £38.46 each month |

The long-term prognosis after being diagnosed with hypertension is good. If nothing else, it’s a wake-up call to pay close attention to your health and take proactive steps towards improving it.

If you choose to do nothing, such as continuing with high alcohol consumption, smoking, eating fatty foods, and not exercising, your life insurance policy will come with a high price attached.

As recent life insurance news shows, lower premiums go to those who are actively working to improve their health.

Applying for Life Insurance with High Blood Pressure: What You Need to Know

When you apply for life insurance, you must be honest and tick the box to indicate you’ve been diagnosed with a medical condition.

Hypertension is that, so I don’t think high blood pressure is anything. It directly indicates how healthy your heart is, which is a measurement of your life expectancy.

Be honest in your application, or it will be void.

It doesn’t mean you’ll be automatically locked into a higher premium. The older you are at the time of diagnosis, the better. It’s expected to come with age.

However, the time of your diagnosis will be considered. In some instances, if you’ve only just been diagnosed with hypertension, the insurer will postpone your policy.

This is because you cannot instantly improve your blood pressure readings. It takes time and controlled effort to get your blood pressure under control.

In most cases, insurers will want access to medical records when a pre-existing illness is diagnosed. The reason for this is to establish whether your hypertension is controlled or uncontrolled.

If your records show continued improvement in your blood pressure readings over a two-year period or longer, it indicates that you are taking steps to bring your blood pressure under control.

Lifestyle changes or medication may help lower blood pressure. The important factor is that your numbers improve with time.

Is high blood pressure classified as a critical illness?

High blood pressure (hypertension) is not classed as a critical illness on its own.

Critical illness insurance typically covers severe conditions like heart attacks, strokes, or cancer, not risk factors like hypertension.

However, if high blood pressure leads to a serious complication such as a stroke or kidney failure, the resulting condition may be covered.

The Insurer’s Insurance Hero works with us to consider high blood pressure when assessing applications. Poorly managed hypertension can lead to higher premiums or exclusions, while well-controlled cases may have little impact.

So, hypertension isn’t a critical illness itself, but can contribute to ones that are.

Can I get critical illness cover if I have high blood pressure?

You can still qualify for critical illness cover if you have high blood pressure, but insurers may require more details about your health and daily habits.

If you have other health issues besides high blood pressure, the provider might request additional medical documentation. This often includes a report from your GP, which the insurer can obtain directly with your consent.

Is it possible to access near-regular life insurance premiums when you have controlled hypertension?

If you do nothing to control your blood pressure, though, your premiums will increase based on your risk level.

The higher the level of risk you’re deemed to be, the higher all insurers will quote.

One way to access lower premiums could be to consider decreasing term life insurance. As you’ll probably know, there are many types of life insurance policies.

For term insurance, there’s level term, which pays out a fixed amount, and then there’s decreasing term and increasing term.

The aim of decreasing term insurance is to provide an adequate level of cover and ensure that you aren’t overinsured.

With level coverage, you can become overinsured. For example, you have an insurance policy with a £100,000 fixed payout in the event of your death.

This may be adequate cover if you have debt-related costs and a mortgage that must be paid to leave your family with suitable financial cover.

Over time, mortgage payments and debts will decrease, and you may not require £100,000 to meet financial obligations.

With decreasing-term cover, the amount paid out is variable and decreases the longer you live, as your financial obligations decrease over time.

This would mean a lower payout in the long run; however, it can offer significant savings in premiums.

Of course, before deciding on the type of high blood pressure life insurance policy to take out, you should seek expert financial advice to ensure you get adequate coverage and that your policy does not have an exclusion clause preventing payout in the event of a heat-related illness.

The majority of insurance companies offer specialist cover for existing medical conditions. Hypertension is a medical condition that your life insurance policy must cover; otherwise, it may be deemed void.

Declare your situation, explore your options with a financial advisor, and follow your doctor’s advice to bring your blood pressure under control.

You will find that your blood pressure life insurance quotes aren’t as expensive for controlled hypertension as they are for uncontrolled high blood pressure.

Related Reading:

Can People With Heart Problems Get Life Insurance?

Life Insurance Quotes For Individuals With Diabetes

High Cholesterol Life Insurance Quotes

Steve Case is a seasoned professional in the UK financial services industry, with over twenty years of experience. At Insurance Hero, Steve is known for simplifying complex insurance topics, making them accessible to a broad audience. His focus on clear, practical advice and customer service excellence has established him as a respected leader in the field.