Average Cost Of Life Insurance Per Month In 2026

Based on Insurance Hero’s analysis of quotes from our panel of FCA-authorised insurers in January 2026, the average cost of life insurance in the UK is approximately £8 per month for every £100,000 of cover for a healthy person who doesn’t smoke.

We recommend a cover of around ten times your annual salary. For example, based on the current UK median full-time salary of approximately £35,000 (ONS, 2025), this suggests you may need coverage of around £350,000.

- Based on our data, a non-smoking 30-year-old could secure £300,000 of level term cover for under £25 per month, with entry-level premiums starting at £3.57 per month for £100,000 of coverage.

- UK life insurance companies paid out a record £5.32 billion in individual protection claims during 2024, with 97% or more of all claims accepted across major providers (ABI, July 2025).

Are you considering taking out a life insurance policy, or do you think you’re paying too much for your existing coverage? We partner with top UK insurers, both well-known names and niche experts, to bring you the best value life insurance.

Complete The Form Below To Find Your Cheapest Quote

Average Life Insurance Cost Per Month UK Tables

Disclaimer: The quotes indicated below are from FCA-authorised insurers, including Aviva, Vitality, Zurich and Royal London. The figures are based on Insurance Hero’s own sales records covering a full 12-month period.

Our data includes customers across all eligible age groups. Pricing information reflects policies sold to men and women, including smokers, vapers, and non-smokers. We also consider joint applicants, level term and decreasing term life insurance, and whole-of-life plans.

So, what’s the average cost of life insurance? The price of life insurance goes up with your age, and many other factors could affect the cost of your life insurance.

Our average life insurance cost per month UK tables should give you a fair indication of the costs for term, joint, whole-of-life, and smoker policies. People are often surprised at how low policy prices can be.

As shown in the life insurance rates by age charts, coverage is available for under £5 per month. A smoker in their 30s can also secure cover for under £10 per month.

The Insurance Hero team frequently monitors and updates these prices to ensure we can offer policies that suit every budget.

Below is an example price comparison of a term policy with a decreasing term insurance policy. These are quotes for a £100,000 policy. This covers a 30-year period and assumes a healthy, non-smoking individual.

| Your Age | Level Term Life Insurance | Decreasing Term Life Insurance |

|---|---|---|

| 20 | £3.57 | £4.65 |

| 25 | £3.61 | £4.84 |

| 30 | £4.48 | £5.13 |

| 35 | £5.81 | £6.02 |

| 40 | £8.12 | £7.89 |

| 45 | £11.28 | £10.81 |

| 50 | £18.73 | £17.08 |

For ages 40 and up, decreasing term life insurance is usually more affordable than level term coverage.

If you are younger, level term plans may offer lower premiums. It is worth noting that decreasing term coverage may still be the better choice depending on your needs (for example, if your mortgage balance is decreasing over time).

The average life insurance cost of a joint policy

A joint life insurance policy covers two people, usually a married couple. If one person dies, the other person will receive the death benefit.

This type of policy can benefit couples who want to ensure their loved ones are taken care of financially in the event of their death.

A joint policy is generally 25% cheaper than two singles. It will always result in a single payout rather than two.

When deciding whether to purchase joint coverage, it is important to consider the monthly savings compared with the loss of a single sum assured to your loved ones in an emergency.

Below is an example of a price comparison between single policies and one joint policy.

These quotes are based on a policy that provides £100,000 of coverage over 30 years for non-smoking, healthy individuals.

| Age Of Person | Cost of One Joint Policy (£ per month) | Cost of Two Single Policies (£ per month) |

|---|---|---|

| 20 | 5.25 | 7.14 |

| 25 | 6.30 | 8.62 |

| 30 | 7.58 | 8.71 |

| 35 | 10.22 | 11.23 |

| 40 | 14.28 | 16.20 |

| 45 | 20.53 | 22.31 |

| 50 | 29.71 | 33.50 |

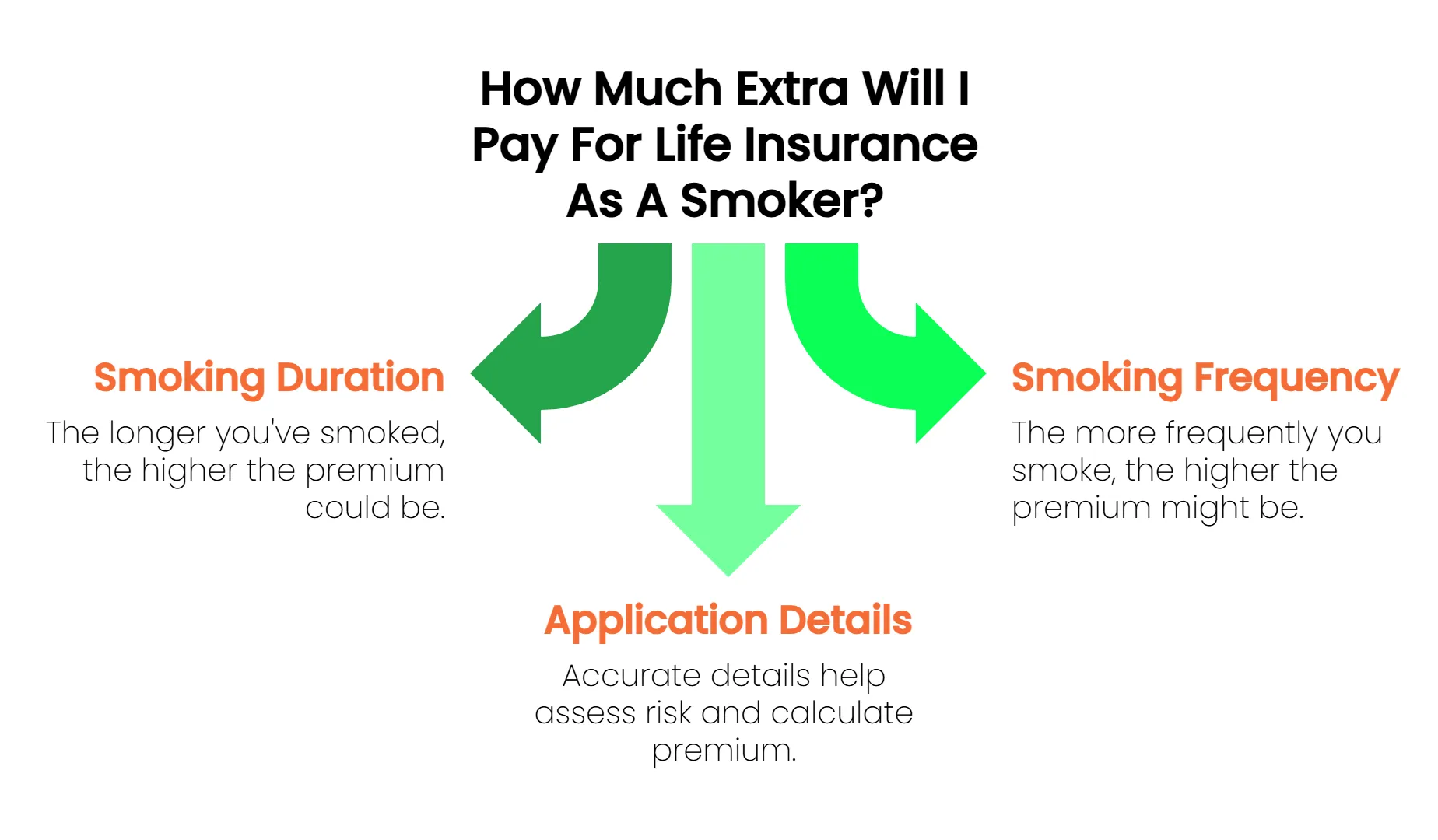

The Average life insurance cost for a smoker

Smokers’ life insurance policies are specifically designed for smokers.

These policies typically have higher premiums than regular life insurance policies, but they can still be a great way for smokers to get the coverage they need.

So, as we mentioned above, because of the additional health consequences, the average life insurance cost for a smoker can be higher than for someone who is not a smoker.

This could be up to 50% higher for someone over 50.

Smokers pay an average of 64% more than non-smokers in the UK for standard life insurance. The average monthly cost of life insurance for smokers is £14.19 per month, compared to £7.99 for non-smokers.

Your smoking status is just one of the factors that will be considered when you arrange your life insurance.

Life insurance providers may request additional information, such as the frequency and duration of your smoking habit.

The data will be used to assess the potential impact on your health and the effect on your eligibility for a claim.

Below is an example of a monthly price comparison between a smoker and a non-smoker in good health.

The quotes are based upon a £100,000.00 level term policy over a 30-year period.

Smokers pay an average of 64% more (Source: Insurance Hero analysis of 250+ quotes across seven age brackets, January 2026).

| Your Age | Cost (Smoker) | Cost (Non-Smoker) | (%) Cost Increase |

|---|---|---|---|

| 20 | £4.31 | £3.53 | +22% |

| 25 | £5.29 | £3.56 | +49% |

| 30 | £7.48 | £4.45 | +68% |

| 35 | £10.46 | £5.96 | +78% |

| 40 | £16.31 | £8.33 | +96% |

| 45 | £26.52 | £12.29 | +116% |

| 50 | £43.89 | £23.73 | +90% |

Average costs of a whole-of-life insurance policy

A whole life insurance policy is a type of life insurance that provides coverage for the policyholder’s entire lifespan.

- It differs from other life policies, such as term life insurance, which provide coverage for a specific period.

- Whole life insurance can be used to cover various needs, such as final expenses, estate planning, and long-term care.

- The premiums for a whole-of-life insurance policy are typically higher than those for other types of life insurance policies.

Still, the policyholder can be assured they will have coverage until death. This type of policy can be a valuable asset for individuals who want to ensure their loved ones are financially cared for after they pass away.

This guaranteed payout is why this type of protection tends to be the most costly.

Like other types of life insurance, the cost of your premiums will be affected by your age, health, and coverage requirements.

The table below shows example costings for whole of life insurance.

The Quotes are based on a non-smoking, healthy individual requiring £100,000 of cover.

| Your Age | Whole Of Life Cover Cost |

|---|---|

| 30 | £64.02 |

| 35 | £73.91 |

| 40 | £82.71 |

| 45 | £91.62 |

| 50 | £108.24 |

The table below provides an overview of the monthly cost of a £250k life insurance policy designed to protect a UK mortgage based on the insured’s age.

The costs increase with age, reflecting the higher risk and premium associated with older policyholders.

| Your Age | Mortgage Life Insurance Monthly Cost (£) |

|---|---|

| 20 | 7.03 |

| 25 | 8.63 |

| 30 | 10.06 |

| 35 | 13.22 |

| 40 | 19.20 |

| 45 | 35.09 |

| 50 | 54.01 |

What is the average cost of an over 50 life insurance policy?

As people get older, the way life insurance is priced and structured can change significantly.

One distinct category for older adults is over-50s life insurance. This is often referred to as guaranteed acceptance life insurance, which differs from standard term or whole-of-life policies.

The main differences are as follows:

- No medical underwriting is required. There is usually no need to answer health questions or provide medical information.

- Premiums are fixed and typically payable until death (or to a defined age).

- Coverage amounts are smaller and often set in bands (for example, £2,000–£20,000)

Based on our data over the last 12 months, the average cost of over-50s life insurance is £28–£30 per month for modest funeral-level coverage.

The table below gives you a more comprehensive range of ages and their corresponding payouts.

| Age | Typical Monthly Premium | Average Lump Sum Payout |

|---|---|---|

| 55 | £15 – £25 | £5,000 – £10,000 |

| 60 | £20 – £30 | £4,500 – £9,000 |

| 65 | £25 – £40 | £4,000 – £8,000 |

| 70 | £30 – £50 | £3,000 – £7,000 |

Costs Of Life Insurance Case Study:

The following case study is an illustrative example based on a typical Insurance Hero customer scenario. Names and details have been created to illustrate how life insurance costs vary across age groups.

Case Study 1: Young Couple with Kids

Meet John and Lisa, a young couple living in Brighton, both 32, with two children, ages 4 and 6. Recognising their responsibilities, they decided to explore life insurance policies.

- Their primary goal was to ensure their children would be financially secure in the event of either of them passing away.

- After research, they found that life insurance costs vary significantly based on several factors, including age, health status, and coverage amount.

- Being young and in good health, John and Lisa realised that life insurance was quite affordable for them.

- They were pleasantly surprised to find that the premiums were well within their budget, debunking the myth that life insurance is always expensive.

- They found that the average premium for their age bracket was around £6-£8 per month for level or decreasing term policies, respectively.

A small price to pay for the reassurance it provided. The pricing of life insurance for their age and health status was a sound investment given the long-term benefits.

Upon choosing a policy, they knew their children would be financially supported should the unexpected occur.

They also discovered the benefits of the life insurance policy for their mortgage payments, ensuring their family would not lose their home.

Looking at the prices of life insurance, they felt reassured that they had made a wise choice in safeguarding their family’s future.

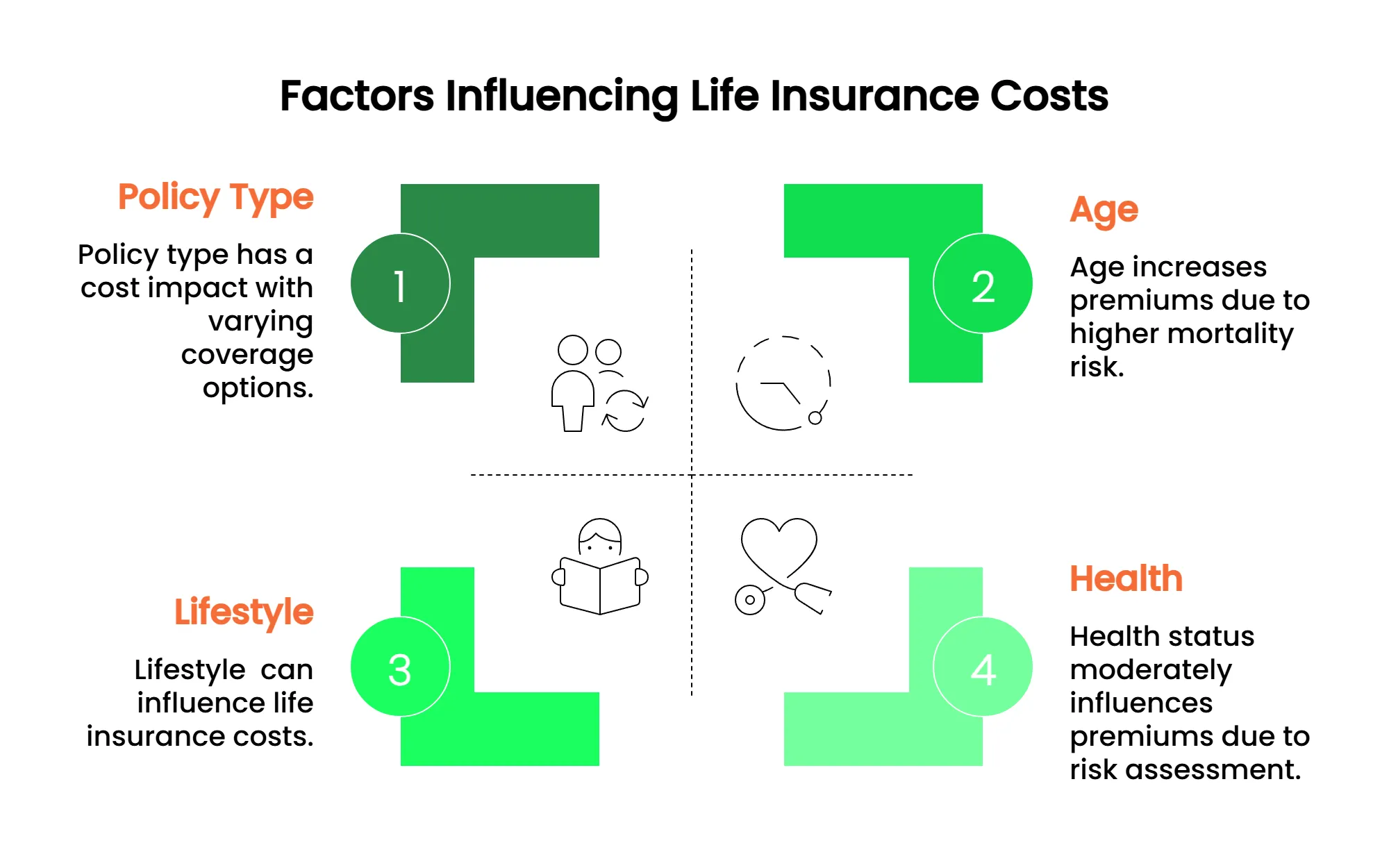

What affects the cost of life insurance?

Many factors affect the cost of life insurance. One of the most important is your age. The younger you are, the cheaper your life cover will be.

That’s because the insurance company expects you to live for a longer period, so they charge you less for coverage.

Another important factor is your health. If you have a history of health problems, are a smoker, or are currently suffering from a critical illness, your life insurance will be more expensive.

Your occupation is also a factor that affects your life insurance premiums. If you have a dangerous job (such as a soldier or a miner), your rates can be higher than someone with a less risky job (such as an office worker).

The reason is that there’s a greater chance that you could die while working, so the insurance company charges more to cover you.

Finally, the amount of coverage you need also affects the cost of your life insurance premium. The more coverage you need, the more expensive your policy will be, as the insurance company is taking on more risk by insuring you for more money.

So, if you’re wondering what affects the cost of life insurance, here are some of the most critical factors.

Personal circumstances such as age, health, occupation, and the amount of coverage you need all play a role in determining your premiums.

Insurance Hero Tip: Smokers are likely to be charged more for life insurance because they add what is known as “smoker loading” to the cost.

However, if you stop smoking, your life insurance price may drop. Some insurers will even remove the smoker loading if you have quit for at least one year.

Insurance Hero can help you find the right policies. When applying for life insurance, you must be honest about your smoking history.

Average life insurance cost – level term vs decreasing term cover

As the policy term length decreases, term insurance becomes the most affordable life insurance option.

Regarding life insurance coverage, there are two main types of policies: level-term and decreasing-term.

Both have unique benefits, making it challenging to decide which is right for you.

Premiums

The key difference between level term and decreasing term cover is the premium structure. With level-term insurance, the premiums remain the same throughout the entire duration of the life policy.

Guaranteed premiums mean that you will always pay the same amount each month, regardless of your age or life expectancy.

On the other hand, decreasing term insurance has monthly premiums that decrease over time. This is often an advantage, as your monthly payments will become more affordable as you age.

Pay Out Amount

Another critical difference between the two types of life insurance coverage is how the death benefit is paid out.

With level term insurance, the death benefit is paid out in a lump sum to your beneficiaries, and the amount doesn’t change with time.

This can help them cover funeral costs, inheritance tax, other debts (e.g., interest-only mortgage), or final expenses you may leave behind.

On the other hand, decreasing term insurance pays out the death benefit in instalments. This can be helpful if your beneficiaries need a regular income to help cover living expenses.

With decreasing term life insurance, the payout amount decreases over time, which is why people tend to choose it when they have a debt that’s being reduced over time, such as a repayment mortgage (although there’s also something called mortgage life insurance available).

So, which type of policy is right for you? That depends on your individual needs and circumstances. If you want coverage lasting for a set number of years, level-term insurance is the best option.

If you want monthly premiums that decrease over time, a decreasing term policy is the right choice. Ultimately, the key is to choose the policy that best suits your needs and budget.

Is Now The Right Time To Get Cover?

Life insurance is not just a choice but a crucial safeguard for your family’s financial future. It’s important to compare quotes to obtain the most affordable rates.

No matter your age, health, or type of life insurance, it’s worth comparing life insurance quotes from different insurers to get the best life insurance policy at a great price.

So, do you need life insurance? The answer is probably yes, especially if you have people who are financially dependent on you.

A life insurance policy can give your loved ones financial security when you’re gone. It can help to ease the burden of funeral costs and other expenses associated with your death.

A life insurance policy is a way to show your loved ones that you care. It can give them peace of mind knowing they will be financially taken care of if something happens to them.

It’s important to remember that life insurance isn’t just for stay-at-home parents or those with young children; it can be vital for anyone with loved ones who would be affected by their death.

You don’t have to worry about finding the right policy or filling out a lot of paperwork – the companies we work with will handle all that for you.

Complete one of our simple forms, receive a no-obligation life insurance quote and receive the best life insurance prices.

£100,000 Life Insurance Policy Cost 2026 – Simplified Quotes

One of the most popular questions that insurance agents and insurance companies are asked is, “How much does £100,000…

£200,000 Life Insurance Cover 2026

A £200,000 life insurance policy can help to provide your family with the financial support it needs if you, the primar…

How Much Does A 500K Life Insurance Cost In The UK?

The Insurance Hero team has studied insurers from the big, well-known brands to smaller, more boutique insurance compani…

How Much Life Insurance Do I Need In 2026?

It’s a common question: how much life insurance do I need if I’m single or part of a family unit? A general guid…

Is Life Insurance More Expensive For Males?

Gentlemen, are you aware that life insurance premiums might be higher for you just because you’re a man? We are …

The tabular data is accurate as of January 2026. Financial product costs fluctuate over time due to inflation andother market forces. All quotes were obtained from Insurance Hero’s panel of FCA-authorised insurers. Individual premiums vary based on personal circumstances.

Sources And References:

[1] IBISWorld, ‘Life Insurance in the UK: Industry Market Research Report,’ 2025–26.

https://www.ibisworld.com/united-kingdom/market-research-reports/life-insurance-industry/

[2] MoneySupermarket, ‘Life Insurance for Smokers,’ accessed January 2026.

https://www.moneysupermarket.com/life-insurance/life-insurance-for-smokers

[3] GlobalData, ‘UK Life Insurance Market Size and Trends,’ 2024.

https://www.globaldata.com/store/report/uk-life-insurance-market-analysis/

[4] Mintel, ‘UK Term Assurance Market Report,’ 2025.

https://store.mintel.com/report/uk-term-assurance-market-report

Steve Case is a seasoned professional in the UK financial services and insurance industry, with over twenty years of experience. At Insurance Hero, Steve is known for his ability to simplify complex insurance topics, making them accessible to a broad audience. His focus on clear, practical advice and customer service excellence has established him as a respected leader in the field.