HSBC Life Insurance Review

Life insurance is an important financial product that can help provide financial security to your loved ones in the event of your death or terminal illness.

HSBC offers a range of life insurance products that can help provide financial protection and peace of mind for individuals and their families.

Please read the comprehensive HSBC life insurance review below to learn about the company’s offerings and decide whether it meets your needs and expectations.

Compare HSBC With Other Top Insurers. Find The Best Cover For You & Help Provide Your Family With Financial Security

Online review companies aggregate customer experiences with HSBC.

| Review Platform | Review Quality And Number |

|---|---|

| Trustpilot | 9,899 Total Reviews |

| SmartMoneyPeople | A Score Of 3.42 Out Of 5. Based on 2,008 Reviews. |

| Fairer Finance | A claims score of 81.65% and an overall rating of 73.65% |

| Defaqto | The expert review platform Defaqto has given HSBC’s level term policy 4 out of 5 stars, while their decreasing term policy received an average rating of 3 stars. |

Who Is HSBC?

HSBC is one of the world’s largest banking and financial services organisations, providing life insurance solutions through HSBC Bank and more comprehensive personal insurance plans through the bank’s financial advisers, selected intermediaries, and brokers.

HSBC Life (UK) Limited is a subsidiary of HSBC Bank PLC and is authorised and regulated by the Financial Conduct Authority and the Prudential Regulation Authority.

As a member of the Association of British Insurers, HSBC Life (UK) Limited is committed to maintaining high standards in the insurance industry.

In 2025, HSBC Life (UK) Limited paid 99% of life insurance claims and 95.5% of critical illness insurance claims, indicating a solid track record of delivering on its promises to customers.

| Provider Overview | HSBC is a major UK bank offering term-based life insurance policies via HSBC Life (UK) Limited. |

| Policy Types | Level Term: Fixed payout; Decreasing Term: Reduces over time, ideal for mortgages. |

| Eligibility | Available to individuals aged 17–70; coverage ends by age 80. |

| Payout Rate | A high payout rate of 97% for claims in 2025. |

| Additional Benefits | Includes free terminal illness and accidental death cover. |

| Critical Illness Cover | HSBC is a major UK bank that offers term-based life insurance policies through HSBC Life (UK) Limited. |

| Income Protection | It covers up to 50% of pre-tax income (up to £50,000/year) and offers deferred periods of 4 to 52 weeks. |

| Joint Policies | An optional add-on covering 36 conditions with payouts from £10,000 to £1,000,000. |

| Policy Costs | Joint life insurance pays out once, typically upon the first policyholder’s death. |

| Trust Options | Policies can be written in trust to reduce inheritance tax and simplify payout processes. |

| Strengths | Affordable premiums, high payout reliability, and mortgage protection for HSBC customers. |

| Limitations | Limited product range (no whole-of-life policies) and fewer value-added benefits than competitors. |

| Cancellation Process | You can call 0345 745 6125 during business hours; consider alternatives before cancelling. |

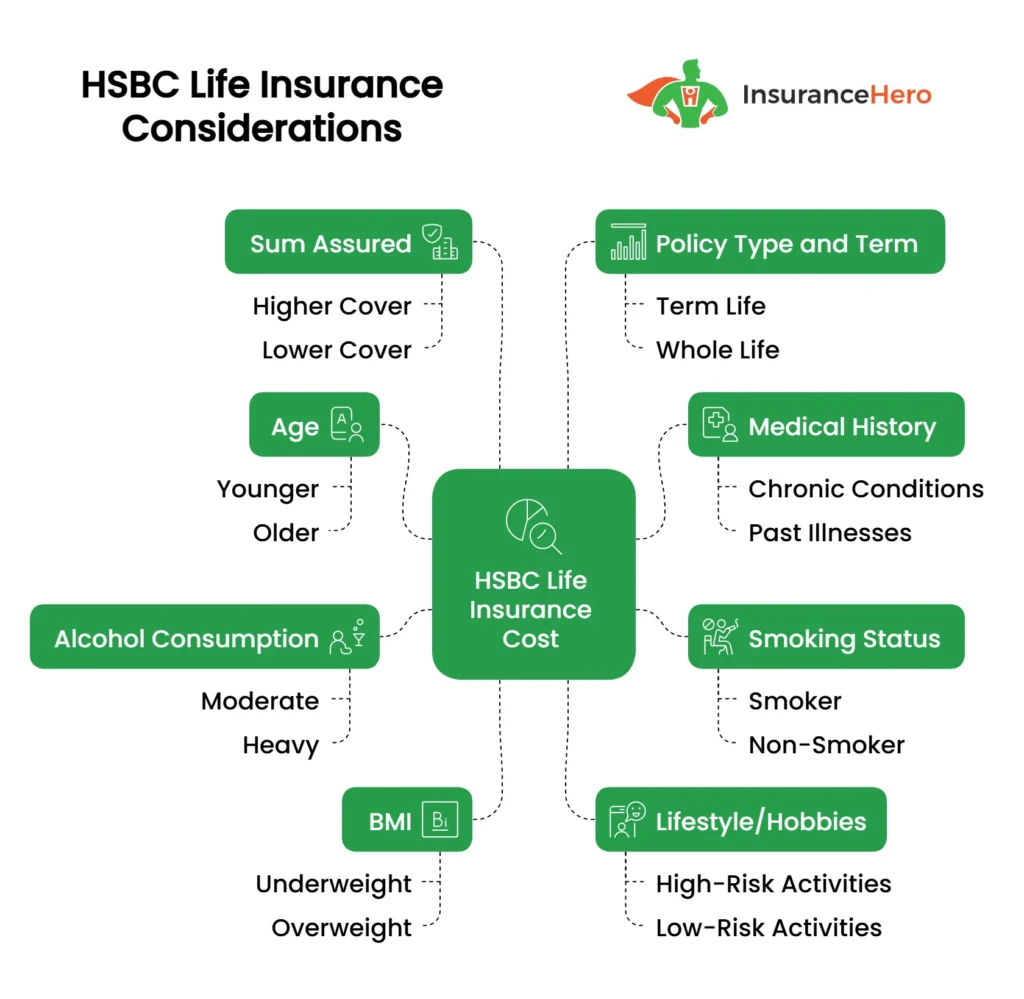

How Much Does HSBC Life Insurance Cost?

The HSBC life insurance cost will depend on your circumstances, including the following:

• Your age

• Your overall health condition

• Your lifestyle

• Your occupation

• Your smoking habits

Age and smoking habits are among the most important factors in determining the initial quote for HSBC life, as well as for critical illness and income cover policies.

However, other factors, such as your overall health, medical history, lifestyle, and occupation, can influence the final price.

This is why it’s essential to disclose all relevant information to the insurance provider so that they can provide an accurate and fair quote.

If you have any pre-existing health conditions or work in a high-risk job, finding a policy that offers comprehensive coverage at an affordable price may be challenging.

An insurance specialist can help you understand your options and find the best policy for your individual circumstances.

It’s always better to be upfront and honest about your health and occupation when applying for life insurance, as this will help ensure that your policy provides coverage in the event of a claim.

The table below illustrates sample monthly quotes from HSBC for both level and decreasing-term life insurance plans.

So, how much is HSBC Life insurance per month? The table below breaks down current policy costs and is updated often by the Insurance Hero team.

These numbers are based on a non-smoker in fair health requiring £200,000 of coverage over 20 years.

| Persons Age | Decreasing Term Cover | Level Term Cover |

|---|---|---|

| 25 | £3.87 | £4.25 |

| 30 | £5.09 | £6.52 |

| 35 | £6.72 | £9.33 |

| 40 | £9.87 | £13.75 |

| 45 | £14.23 | £19.17 |

| 50 | £20.46 | £26.78 |

| 55 | £23.71 | £25.16 |

Types of HSBC Life Insurance Policies

HSBC offers both level life insurance and decreasing life insurance, with coverage of up to £2,000,000, a minimum term of 5 years, and a maximum term that extends to age 80.

The monthly premiums for HSBC life insurance are fixed for the duration of the coverage, providing customers with predictability and stability.

Terminal illness benefits are also included with HSBC life insurance. An early death claim can be made if the policyholder becomes terminally ill and is appropriately assessed to have less than 12 months to live.

This benefit can provide additional financial support to the policyholder and their loved ones during times of difficulty.

HSBC Level Term Life Insurance Policy

Level-term life insurance is the simplest insurance plan for HSBC banking customers. It is available as a joint policy for couples or partners, and only one person needs to have an HSBC bank account.

A level cover life insurance policy pays a lump sum of money if the policyholder dies within the term of the cover, and the payout amount is always the same.

This can provide financial security for the policyholder’s loved ones in the event of the policyholder’s unexpected death and help cover costs such as outstanding debts, funeral expenses, and ongoing living expenses.

Individuals should carefully assess their life insurance needs and select a policy that suits their specific circumstances.

Insurance experts, such as Insurance Hero, can provide guidance on the best life insurance options, helping you compare plans and choose the one that best suits your needs.

HSBC Decreasing Life Insurance Policy

HSBC Life Insurance Company also offers a decreasing life insurance cover, designed to cover an outstanding repayment mortgage balance.

The sum assured decreases each month in line with the balance, assuming an interest rate of no more than 7%.

This type of life insurance can provide a cost-effective way to ensure that an outstanding mortgage balance is paid off in the event of the policyholder’s death.

The decreasing cover amount is designed to match the repayment mortgage balance over the policy term, ensuring that the outstanding balance is fully covered at all times.

HSBC Critical Illness Cover Policy

HSBC critical illness cover provides a lump sum payment if the policyholder is diagnosed with one of the conditions listed in the policy terms and conditions.

This lump-sum payout can be used to pay off or pay down the policyholder’s mortgage or to cover other expenses related to their illness.

Adding critical illness insurance to a life insurance policy can provide additional financial protection for the policyholder and their loved ones in the event of a serious illness or death.

The premiums for this type of cover are typically fixed for the duration of the policy, providing customers with predictability and stability.

HSBC’s critical illness insurance covers 35 critical illnesses and surgical procedures. Some of the examples are:

- Cancer (apart from less advanced cases)

- Benign brain tumour

- Blindness

- Heart attack

- Major organ transplant

- Multiple sclerosis

- Parkinson’s disease

- Stroke

Critical illness insurance – what are you not covered for?

While HSBC’s critical illness insurance policy covers a range of serious illnesses, some conditions are not covered.

These include:

- Aplastic Anaemia

- Loss of independent existence

- Chronic lung disease

- Ulcerative colitis

- Early-stage cancers

It’s important to carefully review the terms and conditions of any critical illness insurance policy before purchasing it to ensure that it meets your individual needs.

It can be helpful to speak with a professional life insurance broker to better understand the different critical illness insurance policies available and what they cover.

An expert can help you compare different policies and find one that fits your unique circumstances and budget. Get a quote and compare plans to find the one that suits your needs.

Partial payments for critical illness are not covered under HSBC’s critical illness insurance policy, but they may be covered under other policies offered by other insurers.

These partial payments, also known as “additional benefits” or “extra cover,” can provide financial support for less severe conditions that may not meet the full definition of a covered critical illness.

This can be particularly helpful for individuals diagnosed with a condition that affects their ability to work and earn income but may not meet the full criteria for a lump-sum payout.

HSBC Whole of Life Insurance Policy

HSBC does not offer a whole life protection policy as a life insurance product.

HSBC Income Cover Policy

HSBC income cover protects against periods of incapacity to work where you suffer a loss of income.

This type of insurance is designed to replace a portion of your income if you cannot work due to illness or injury.

The income protection policy provides a regular monthly benefit, paid to you after an agreed waiting period and can continue until you return to work or until the end of the policy term.

The waiting period, or deferred period, is the time you have to wait before you can start receiving the benefit.

HSBC income cover offers two options: a 2-year or full-term cover option. The 2-year cover option benefits up to 2 years per claim, while the full-term cover option provides the benefit until the end of the policy term or incapacity ends.

The policy covers up to 50% of pre-tax earnings, with a maximum annual limit of £50,000.

You can choose an initial waiting period of 4, 8, 13, 26, or 52 weeks. The policy also includes a rehabilitation or proportionate benefit, which can supplement your income if your income is reduced due to working fewer hours or changing the type of work because of incapacity.

HSBC Terminal Illness Benefit

HSBC’s terminal illness benefit is a common feature in many life insurance and critical illness insurance policies.

It provides policyholders with the peace of mind that they will be able to access some of their policy’s benefits if they become terminally ill and are not expected to survive for long.

The payment can help with medical expenses or support loved ones financially during a difficult time.

However, it’s important to note that the terminal illness benefit applies only if the illness is deemed terminal and the policyholder is expected to live for 12 months or less.

Advantages of HSBC Life Insurance

- HSBC allows you to take out a life insurance policy and a mortgage or loan, and your premiums and payout will be linked to your outstanding debt.

- HSBC offers a free accidental death benefit that will cover you for accidental death while your life insurance application is being considered. Your loved ones would receive up to £250,000 if you died from an unintentional injury while waiting for the policy to be approved.

Disadvantages

- HSBC does not offer an increasing cover policy, which will increase your premiums and payout over time.

- Other insurers may cover a wider range of illnesses and conditions under their Critical Illness protection policies.

- As with most life insurance cover, if you stop paying your premiums, you won’t get any money back, and your coverage will likely stop.

HSBC Life Insurance Calculator

Like many banks, HSBC offers a life insurance calculator, a valuable tool for determining the amount of life insurance you need.

HSBC’s life insurance calculator uses the following information to calculate your life insurance:

- Your and your partner’s income

- Your children and their ages

- Debts

- Savings

- Mortgage balance

- University fees planned

- The period of time you wish to be covered for

While life insurance calculators like the one provided by HSBC can be a helpful starting point for determining your life insurance needs, it’s important to remember that they are typically based on general assumptions and don’t take into account all of your circumstances.

The calculator’s recommended amount of life insurance is just an estimate and should be considered a general guide rather than a definitive answer.

Your unique circumstances and priorities may influence the amount and type of life insurance appropriate for you, so it’s a good idea to speak with an insurance expert to get a more personalised assessment of your needs.

FAQs

How much does HSBC life insurance cost?

The cost of life insurance from HSBC or any other provider will depend on various factors such as the level of cover, the type of policy, and your circumstances.

In general, life insurance costs tend to increase with age, as older individuals are considered a higher risk to insure.

Other factors that can impact the cost of life insurance include your health status, your family’s medical history, your lifestyle habits (such as smoking), and the policy term length.

Some policies may also require a medical examination before approval, which could impact the cost of coverage.

Can I make changes to my HSBC life insurance policy?

Yes, you can. If your circumstances have changed, contact HSBC to request an amendment to your current agreement.

For example, if you have kids and would like to increase coverage, or conversely, if your children move out and you would like to lower your protection.

HSBC may also invalidate your policy if you fail to inform them about specific changes. So even if you have started a new job or hobby or started smoking again, you might need to contact HSBC.

Is the lump sum payment taxable?

Life insurance payments are free from income and capital gains tax for UK residents at the moment, but depending on the value of your estate, they may be subject to inheritance tax.

It’s also worth noting that tax rules may change in the future, which, as a result, can affect the tax implications on your payout.

How does the claims process work for HSBC’s life insurance?

You can claim your payment by phone by calling 0345 745 6125. If you’re based outside of the UK, you can call +44 1226 261 010.

To ensure the process proceeds smoothly and efficiently, it is advisable to have the policy number and the policyholder’s name readily available, along with other relevant details such as proof of death.

Life Insurance HSBC contact details:

Customer Services Centre HSBC Life (UK) Limited

PO Box 1053

St. Albans

Hertfordshire

AL1 9QG

Web: https://www.hsbc.co.uk/insurance/life/

Claims: 0333 745 6125; Email: life.claims@hsbc.com

AA Life Insurance UK Cover Review 2026

Various life insurance products are available, including level term, decreasing term, and 50-plus. AA life insu…

AEGON Life Insurance Reviews 2026 – Compare Quotes

If you want to provide financially for surviving loved ones upon death, AEGON life coverage may be the solution. …

AIG Life Insurance UK Reviews 2026 Update

AIG (American International Group) is synonymous with the insurance industry. AIG’s UK protection business wa…

ASDA Life Insurance Review 2026

ASDA Financial Services offers travel, home, motorist, pet, life insurance, personal loans, trade, gift, and credit card…

Aviva Life Insurance Review For 2026

Aviva is the largest UK insurance services provider and the fifth largest insurance group, with more than 45 million cus…

Axa Life Insurance Cover Review

The AXA Group has been in the insurance business since the 18th century. Acquisitions, mergers, and name changes among l…

Barclays Life Insurance Review For 2026

Barclays PLC is a major financial services company backed by more than 300 years of history. Welcome to our new…

British Seniors Over 50 Life Insurance Reviews 2026

Find out about British Seniors Over 50 Life Insurance Reviews, Customer Experience, and Policies Available. Abou…

Direct Line Life Insurance Review 2026

Direct Line is a household name for insurance products. At the outset, their core offering was vehicle insurance with a …

Ageas Protect Life Insurance Review

Fortis Life is now Ageas Protect, the financial protection arm of Ageas within the UK. The company offers produ…

Friends Life Life Insurance Reviews

Since 1810, Friends Life has been providing financial services. Founded in Yorkshire as Friends Provident in 1832, the c…

LV Life Insurance Reviews – Liverpool Victoria 2026

In 2007, Liverpool Victoria rebranded their company name to use LV=. The LV= brand is a visual play on the word…

Nationwide Life Insurance Review 2026 Cover & Costs

Nationwide Building Society offers insurance, banking, investment, loan, credit card, and mortgage services to residents…

NatWest Life Insurance Review From £5.46 Per Month

Welcome to our newly updated 2026 Natwest life insurance reviews page National Provincial Bank was established i…

One Family Over 50s Life Insurance Reviews

One Family over 50s life insurance offers UK residents aged 50 to 80 a straightforward way to take out life insurance co…

Post Office Life Insurance Review

Welcome to our Post Office life insurance review. In the United States, the Post Office is where residents mail letters …

Prudential Life Insurance UK Reviews

The international financial services group Prudential plc serves over 25 million customers and manages approximately £3…

Royal London Life Insurance Reviews

Royal London is the largest mutual life and pensions company in the UK. It comprises several specialist businesses desig…

Scottish Provident Life Insurance Review

Scottish Mutual Assurance Limited provides healthcare and protection products under the brand name Scottish Provident. …

Scottish Widows Life Insurance Reviews

Scottish Widows is a nationally recognised financial services provider that has served families with financial protectio…

Shepherds Friendly Over 50s Life Insurance Review

The Shepherds Friendly Society is one of the longest-running insurers in the world. In 1826, they began by establishi…

Smart Life Insurance Reviews, What Buyers Should Know

Welcome to our newly updated Smart Life Insurance reviews guide. Smart Life Insurance offers people a range of flexible,…

The Exeter Life Insurance Reviews

Do you have pre-existing medical conditions? Do you want to put in place a robust life insurance policy that will provid…

Virgin Money Life Insurance Review

Virgin Life Insurance is one of the over 400 companies in Virgin Group Limited, the British-branded venture capital cong…

Vitality Life Insurance Review – Should You Buy?

Vitality Life takes a more active role than most insurance providers do by helping people to live active and healthy lif…

Zurich Life Insurance Reviews

Zurich Financial Services Group, commonly referred to as Zurich, was founded in 1872. Headquartered in Zurich, …

Saga Life Insurance Over 50 Reviews

Welcome to our Saga Life Insurance Over 50 Reviews. Many people over 50 are concerned about choosing the right life insu…

Lloyds Bank Life Insurance Review

“Lloyds Bank is likely at the forefront of your search if you’re in the market for life insurance. But how does this maj…