Life Insurance For Parents How It Works

Have you ever sat down to think about the amount of time you spend bringing up your kids, and how much monetary value that would translate to?

Probably not because it’s the nature of the job. You bring your kids up out of love and don’t treat it as a financial chore.

Life Insurance For A Parent In Summary:

Securing life insurance as a parent is a financially wise decision to protect those close to you if the worst should happen.

Insurance Hero can help you find the most comprehensive and cost-effective parents’ life policies.

Here’s why it is worth considering:

- Comprehensive parental protection: Life insurance for parents provides a financial safety net, covering mortgage repayments, childcare, funeral costs, outstanding debts, and living expenses in the event of a parent’s unexpected death.

- Choose options by age and stage: From life insurance for new parents (from just 18p/day) to policies designed specifically for parents over 70. Coverage options include level term, decreasing term, family income benefit, over‑50s, and whole of life policies.

- Single, joint or parent-parent cover: From single parent life insurance, joint life insurance (covering two lives with one payout, cheaper than two singles), or taking out a policy on a parent in later life.

- Flexible protection levels: Determine how much life cover for parents you need by factoring in your mortgage, living costs, childcare, university fees, debts, and funeral costs; tailor the term length to suit life stages.

Parents, Help Protect Your Family’s Future · Compare Top Insurers · Find Your Cheapest Quote

Before discussing life insurance for parents in detail, let’s discuss some of the costs of raising a child.

Insurance Hero has surveyed parents to offer a glimpse into the reality of family-raising costs. The findings will surprise you.

A mother’s perception is that she will spend, on average, eight and a half hours weekly caring for a child and doing chores. The reality is it’s nowhere near that. It’s more like 65.5 hours a week.

When Dads were asked how much time they spent on childcare and associated household chores, they reported spending more time than mothers, averaging 12 hours. In reality, it’s lower at 47.5 hours per week.

How much life insurance cover do you need?

How much life insurance coverage you require will depend on what aspects of your life you are trying to protect if the worst happens.

We all want to protect our family’s financial future, but not many of us take the time or realise how important it is to get the right life insurance policy.

The more coverage you have for yourself and those closest in your life, the more peace of mind you’d have knowing that anything can happen at any time, which means there’s always some sort of protection available if something unexpected should happen.

A financial breakdown could be as follows: Your outstanding mortgage + family living expenses + cremation/funeral costs + university and college fees = The sum assured.

If you’re unsure what amount of family insurance coverage you’ll need, get in touch.

We will be able to discuss your specific needs and provide all the details you need to make an informed decision.

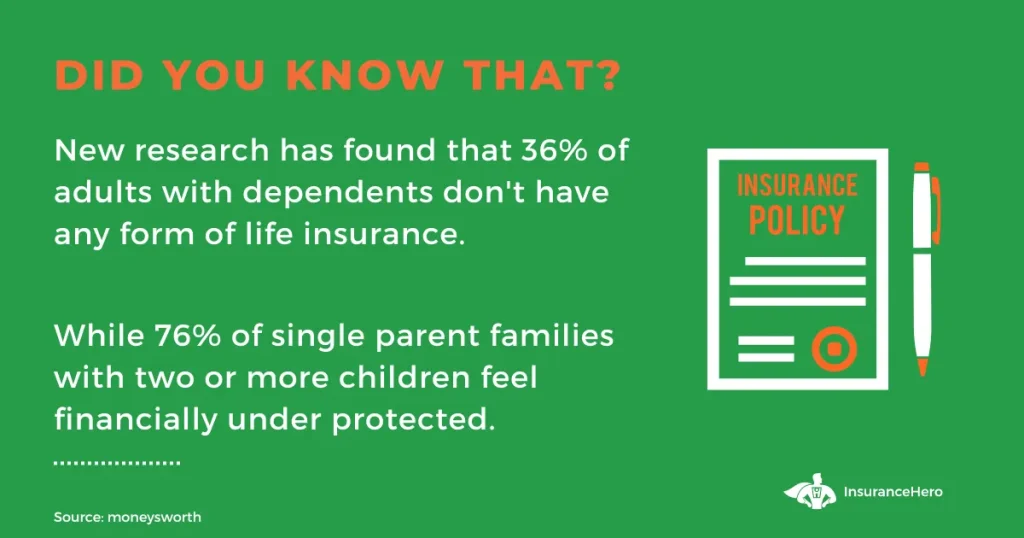

What types of life insurance policies are parents using?

The statistics revealed that the most popular choice by a comfortable margin is that of family life insurance. 53% of parents surveyed have this in place.

Second is critical illness cover, with 28%, followed by 19% of families having income protection, with the lowest of 13% of families with family income benefit protection.

A life insurance plan for new parents is essential to protecting your family.

We help new parents compare quotes to find the most cost-effective financial support possible while also protecting their bank accounts.

Suggestions for new parents to buy life insurance:

- Always compare quotes to get a preferential deal. When you purchase life insurance, it’s important to compare as many quotes as possible to ensure you’re getting the best deal. Doing this could save a significant amount of money on your premiums.

- Think about the best family life insurance policy type to avoid paying for cover that is surplus to requirements. Many types of family life insurance policies are available, so it’s essential to consider which one is best for you and your loved ones. Otherwise, you could end up paying for a life insurance cover amount you don’t even need.

- Adopt a healthy lifestyle. One way to reduce your life insurance costs is to live a healthy lifestyle. This includes eating healthy, exercising regularly, and avoiding risky activities.

- Have your life insurance policy written into a trust at no cost. Inheritance tax can be a significant burden for your loved ones after you pass away. However, if you write your life insurance policy in trust, your beneficiaries could avoid or reduce inheritance tax by up to 40%.

Critical illness cover for parents

Critical illness life insurance is a type of insurance policy that pays out a lump sum if you are diagnosed with a critical illness.

The illnesses qualifying for critical illness coverage vary from provider to provider, but typically include cancer, heart attack and those at risk of stroke or post-stroke.

Critical illness cover can be an essential safety net for you and your family. It can help protect your finances if you become seriously ill.

For example, if you have to take time off work to recover from an illness, the lump sum life insurance payout from your policy could help to cover your mortgage payments or other essential outgoings.

If you’re wondering if you should add critical illness cover to your policy, it’s important to compare offers from different providers.

Term life insurance cover for new parents

Term life insurance is a type oflife insurance that offers financial protection for a set period, usually between 10 and 30 years.

The death benefit is paid only if the policyholder dies during the policy term. If the policyholder does not die during the term, there is no death benefit payout, and the policy expires with no value.

There are two main types of term life insurance in the UK

Level term life insurance and decreasing term life insurance. Level-term life insurance offers a constant death benefit payout for the term, regardless of when death occurs.

Decreasing term life insurance offers a death benefit that decreases yearly, typically in line with Mortgage repayments.

Level-term life insurance for parents

It is often used to protect against an unexpected death that could leave loved ones struggling to make ends meet.

For example, suppose you have young children and a mortgage. In that case, you may want to consider taking out a level-term life insurance policy to ensure that your family can still maintain their current lifestyle if you die unexpectedly.

Decreasing term life insurance for parents

It is usually used to protect against debt repayment, such as a mortgage.

The value of the policy decreases each year in line with the decreasing balance of the mortgage, so that if you die before the mortgage is paid off, your family will not be left with any additional outstanding debts.

While term life insurance provides financial support for your loved ones upon your death, it is essential to remember that it does not cover you for other risks, such as illness or injury.

For this reason, it is important to consider your overall financial needs when choosing the right type of life insurance.

Whole-of-life insurance for parents

Whole-of-life insurance pays out a death benefit when the policyholder dies, regardless of when that may be. It is a type of life insurance policy that provides coverage for the entire lifespan of the insured individual.

Most whole-of-life policies have a fixed premium payable for the policy’s life, and the benefits paid out are also guaranteed for the policyholder’s lifetime.

This makes whole-of-life insurance policies popular for those seeking guaranteed coverage and peace of mind.

Family income benefit cover

Family income benefit cover is insurance that pays a regular income to help meet everyday living costs if you cannot work due to illness or disability.

It is designed to replace a proportion of your lost earnings to maintain your standard of living. Family income benefit cover is usually paid tax-free and is not counted as part of your taxable income.

Family income benefit coverage usually pays out until you retire, die, or return to work.

It shouldn’t be confused with the family support allowance, a government benefit for low-income families.

Family income benefit cover is an insurance policy you take out or as part of your employee benefits package. The family support allowance is means-tested and is only paid for a limited period.

It can be an invaluable safety net for you and your family if you cannot work due to illness or injury. It can help you maintain your standard of living and make ends meet while you recover or adjust to your new circumstances.

Parents’ joint life insurance policy

Joint life insurance is a policy that covers two people, usually a married couple. Its main benefit is that it can be cheaper than two separate policies.

This is because insurers recognise that couples are less likely to die simultaneously than two unrelated individuals. Depending on the policy, it can either pay out on the first or second death.

Some joint parents life insurance policies also offer a ‘survivorship benefit’. This means the policy will pay out if both insured people die during the term.

Joint life insurance can be a helpful way to make sure your loved ones are financially protected in the event of your death.

Life Insurance For Parents Over 50:

| Insurance Company | Policy Type | Coverage Highlights | Ideal For |

|---|---|---|---|

| Legal & General | Term Assurance | Flexible terms, critical illness cover option | For those seeking customisable coverage |

| Aviva | Whole of Life Insurance | Guaranteed acceptance, fixed premiums | Parents over 50 looking for lifelong coverage |

| LV= | Fixed Term Life Insurance | Fixed premiums, including terminal illness cover | For people seeking certainty and affordability |

Life Insurance For Parents Over 60:

| Insurance Company | Policy Type | Coverage Highlights | Ideal For |

|---|---|---|---|

| SunLife | Guaranteed Over 50 Plan | No medical required, fixed premiums | For those focusing on funeral costs |

| Royal London | Over 60s Life Cover | Guaranteed acceptance, cash sum payout | Parents over 60 with health concerns |

| Saga | Term Life Insurance | No medical exam for ages 50-85, fixed premiums | For people seeking straightforward coverage |

Life Insurance For Parents Over 70:

| Insurance Company | Policy Type | Coverage Highlights | Ideal For |

|---|---|---|---|

| British Seniors | Over 50s Life Insurance with Gift | Guaranteed acceptance, includes a free gift | Parents over 70 looking for added benefits |

| Zurich | Whole of Life Assurance | Flexible premiums, potential cash value growth | Parents over 70 desiring comprehensive coverage |

| Age Concern | Funeral Plan | Covers funeral costs, price lock option | The over 70s preparing for end-of-life expenses |

Life Insurance For Parents Living Abroad (UK Citizens):

| Insurance Company | Policy Type | Coverage Highlights | Ideal For |

|---|---|---|---|

| William Russell | Life Insurance for Expats | Designed for UK expats, worldwide coverage | UK parents living abroad seeking extensive coverage |

| Bupa Global | International Life Insurance | Flexible international coverage, critical illness option | UK expat parents needing global and health coverage |

| AIG Life | International Term Assurance | Tailored for UK citizens abroad | UK parents abroad desiring customisable term coverage |

Considerations For Buying Life Insurance For Parents In The UK:

| Consideration | Description | Importance |

|---|---|---|

| Consent and Insurable Interest | Must have parent’s consent and prove financial loss | Legal and policy validity |

| Health Declarations | Health status and medical history affect premiums | Cost and coverage availability |

| Policy Type and Terms | Choice between term, whole life, or specific over 50s plans | Matches coverage needs and affordability |

| UK Regulation Compliance | Policies should comply with UK insurance regulations | Ensures legal protection and claim validity |

Secure your family’s future with tailored life insurance for parents. We offer peace of mind at unbeatable value and protect your loved ones.

How much does it cost to raise a child?

…This is based on each child and not a family.

Our research indicates:

- Accumulative daily costs until a child turns eighteen are £123,365.

That being said…

- Parents don’t expect their kids to leave the nest until they are 22, when they should be financially independent.

- The actual cumulative daily costs accrued for the daily upbringing per child is £184,392, so the average parent is massively undervaluing the total costs by £61,000 per child. (That’s a deposit on their first home.)

- Translated into a weekly cost, it equates to £197.

- £4.82 is the average cost for insurance to ensure your child’s upbringing costs are covered.

What does unpaid work in the house equate to?

- A mother’s monetary value of unpaid work in the family home is estimated to be £29,535.

- It’s not quite as much for the dads, but it still costs a hefty £21,601.

Regular activities that parents spend on include:

- Pocket money

- Entertainment

- Activities and outings

- Treats

The cost for the above comes in at a very pricey £2429.96 annually.

There’s a huge underestimate placed on the cost of raising a child and the amount of time you spend on associated chores around the home.

Should the worst happen and either parent is not around to play their part in the home, the associated costs to hire in help are estimated to be £248 to do the childcare work a Mum does, and for a Dad £169 per week.

That is a lot of money and something you likely wouldn’t be able to comfortably afford without a family insurance policy in place to protect your family’s financial wellbeing.

It is better to be safe than sorry. With family life insurance and parents life insurance, even if a parent dies, the children and the surviving parent can be sure their financial situation will not deteriorate significantly.

Loving someone means taking care of their safety, so providing financial protection to your loved ones is crucial when you still have time.

Women, in particular, should consider securing a comprehensive woman’s life insurance plan. There has never been a better time to get covered and choose the best life insurance plan for you and your family!

External resources you hope you’ll find helpful:

- https://www.aviva.co.uk/insurance/life-products/life-insurance/knowledge-centre/protection-for-parents

- https://ifamagazine.com/new-research-from-lg-swerving-the-money-missteps-blended-families-twice-as-likely-to-take-out-protection-insurance/

Steve Case is a seasoned professional in the UK financial services and insurance industry, with over twenty years of experience. At Insurance Hero, Steve is known for his ability to simplify complex insurance topics, making them accessible to a broad audience. His focus on clear, practical advice and customer service excellence has established him as a respected leader in the field.