Life Insurance For Construction Workers

Insurance Hero has helped construction workers operating in higher-risk activities find life insurance, income protection and critical illness coverage.

Why will getting a quote from Insurance Hero save you money?

We have a strong network of underwriters who specialise in underwriting higher-risk occupations.

We are not tied to any one underwriter. This is what ensures that we can provide you with the most competitive insurance quote if you work in building and construction jobs with varying degrees of risk, including:

- Crane operators

- Roofers

- Iron and Steel Workers

- Electricians

- Power Tool Operators

Compare Quotes From The UK’s Top Providers, Completely Free Quote Service, Save Money Now

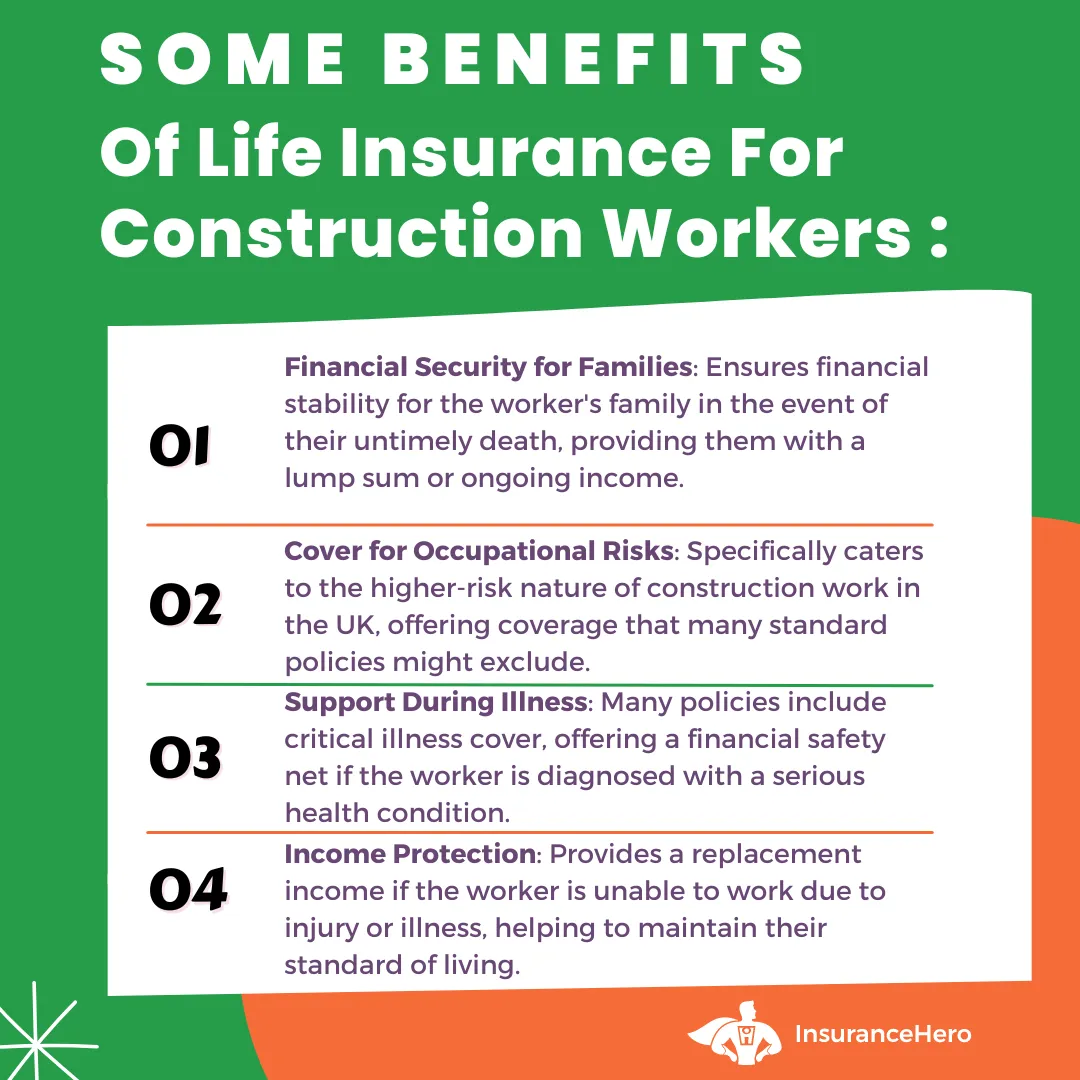

Life Insurance, Income Protection and Critical Illness Cover for Construction Workers

For those working in construction, also known as the building industry, the nature of the work is considered higher risk than in other areas.

Dangerous activities often undertaken on a building site include:

- Demolition

- Handling hazardous materials or waste

- Operating dangerous equipment

- Working at a significant height

Types of Life Insurance Policies for Construction Workers

| Policy Type | Description | Ideal For |

|---|---|---|

| Term Life Insurance | Provides coverage for a specified term, typically 10 to 30 years. It pays out a death benefit if the insured dies during the term. | Construction workers seeking affordable, temporary coverage. |

| Whole Life Insurance | Offers lifetime coverage with a death benefit and a cash value component that grows over time. | It provides coverage for a specified term, usually 10 to 30 years. It pays a death benefit if the insured dies during the term. |

| Income Protection Insurance | Workers who are looking for long-term coverage. | Workers who are concerned about loss of income due to workplace accidents. |

| Critical Illness Cover | Pays out a lump sum upon diagnosis of certain critical illnesses listed in the policy. | Workers who are seeking financial security in case of more serious health issues. |

Factors Affecting Life Insurance Premiums for Construction Workers

| Factor | Description | Impact |

|---|---|---|

| Occupation Risk Level | The level of risk associated with specific construction roles. | A risky lifestyle can increase premiums. |

| Health and Lifestyle | The insured’s health condition, smoking status, and lifestyle choices. | Poor health can lead to higher premiums. |

| Age | Age of the insured at the time of policy purchase. | Older people typically face slightly higher premiums. |

| Coverage Amount | The amount of money the policy will pay out. | Higher coverage amounts lead to higher premiums. |

Common Exclusions in Life Insurance for Construction Workers

| Exclusion Type | Description |

|---|---|

| High-Risk Activities | Certain high-risk job functions may be excluded, such as working at extreme heights or underwater. |

| Pre-existing Conditions | Illnesses or conditions that existed before the policy was purchased may not be covered. |

| War and Terrorism | Deaths resulting from acts of war or terrorism might be excluded. |

| Illegal Activities | Deaths occurring while engaging in illegal activities are typically not covered. |

Steps to Obtain Life Insurance Coverage

| Step | Description |

|---|---|

| 1. Assess Your Needs | Determine the amount of coverage needed based on your financial obligations and family situation. |

| 2. Compare Providers | Research and compare different insurance providers and policies. Insurance Hero can help make this simple for you. |

| 3. Understand the Policy | Carefully read the policy details, including coverage, exclusions, and premiums. |

| 4. Apply for Coverage | Complete the application process, which may include a medical exam and answering questions about your occupation. |

| 5. Review and Update Regularly | Regularly review your policy and update it as needed to reflect changes in your life or occupation. |

What Is Building / Construction Life Insurance Cover?

Life insurance cover is a lump-sum payment to beneficiaries upon the policyholder’s death, in return for regular premiums.

The cost of life insurance will vary with the specific type of activities undertaken in a construction job.

For example, if you are a surveyor whose role involves periodic visits to a construction site, this would be deemed lower risk than the crane operator who operates at height.

This will require additional underwriting from an insurer, resulting in higher insurance premiums.

Questions that you will be expected to respond to as part of the quote process may include:

- Do you handle hazardous materials such as asbestos?

- Does your job involve working at height?

- Do you work with dangerous machinery?

- What are the typical daily activities that you are involved in on the construction site?

As well as detailed fact-finding information, to provide an accurate construction worker life insurance quote, you will need to specify:

- The level of life insurance cover required

- How many years is the policy required to last

- Who are the beneficiaries of the life insurance cover?

For a fast, free, no-obligation quote for building and construction life insurance coverage, please get in touch with us here at Insurance Hero. You can speak directly to one of our friendly team on 0203 129 88 66

About Income Protection Cover for Construction Workers

Insurance Hero can provide competitive income protection cover quotes. If you cannot work due to illness or injury, you will be paid a regular income through income protection cover.

Typically, the policy will pay out after a pre-agreed period, which can range from 1 month to 1 year after you make a claim.

As with life insurance cover, the riskier your occupation on a construction site, the higher the perceived risk.

If you work in demolition or work with hazardous materials, your income protection cover premiums are likely to be higher than for a civil engineer due to the additional underwriting required by the insurer.

Some of the common questions asked to formulate a quote can include:

- What level of income will you require?

- What is your current occupation in the building industry?

- Outline tasks involving working at height with hazardous materials or dangerous machinery

Critical Illness Cover for the Building Industry explained

By paying regular premiums, Critical Illness Cover is structured to pay a lump sum if you undergo a medical procedure or are diagnosed with a critical illness and survive at least 10 days from diagnosis.

The lump sum is designed to assist dependents financially, allowing them to concentrate on their diagnosis and recovery without having financial worries.

Life insurance for carpenters is also available via Insurance Hero, so if you work in this field or are self-employed, please feel free to contact us.

The list of illnesses that are part of critical illness cover includes, but is not limited to some of the following:

- Some types of cancer

- Heart attack

- Stroke, including Cryptogenic, Brain Stem and Transient

- Alzheimer’s disease

- Multiple Sclerosis

- Blindness

To provide an accurate quote, Insurance Hero will need to ask several questions, including:

- How long do you want your policy to last?

- Do you want level or decreasing cover?

- Do you want to add a terminal benefit to your critical illness cover?

Get a free, no-obligation quote today for Building and Construction Life Insurance cover – Protect your family as you undertake high-risk building site work.

Insurance Hero wants to help you get the best quote for you and your dependents. Contact us now for a no-obligation quote on 0203 129 88 66

Steve Case is a seasoned professional in the UK financial services industry, with over twenty years of experience. At Insurance Hero, Steve is known for simplifying complex insurance topics, making them accessible to a broad audience. His focus on clear, practical advice and customer service excellence has established him as a respected leader in the field.