Impaired Risk Life Insurance Cover

It is well-known that health status affects the premiums offered by most life insurance carriers.

If insurance companies identify you as impaired, it’s important to understand how this might affect your ability to find cost-effective impaired life insurance.

Being considered an impaired risk means you could fall outside the standard qualifications for the most favourable insurance rates.

This is often due to factors like:

- Existing health conditions

- High-risk professions or hobbies

- Lifestyle choices, such as tobacco use or heavy alcohol consumption

Being impaired indicates that you might pose a greater risk and, as a result, are more challenging to insure.

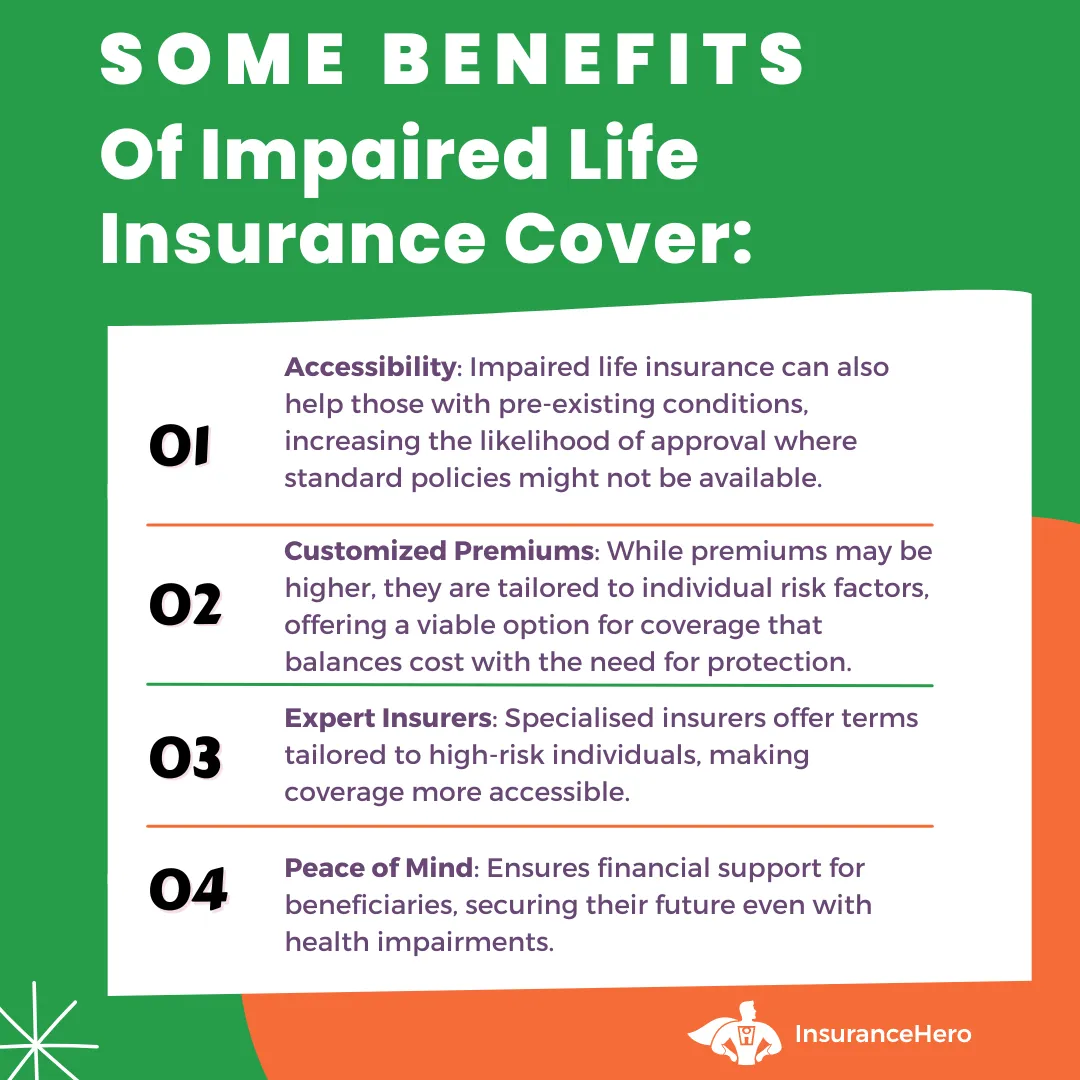

Yet, having an impaired status doesn’t mean obtaining life insurance that adequately safeguards your family is impossible.

Insurance Hero is an impaired risk life insurance specialist. Our dedicated team is well-versed in life insurance for those deemed impaired, helping secure coverage that might otherwise have been challenging to obtain.

Compare The UK’s Top 10 Insurers For Impaired Cover. Find The Best Policy & Save Money Today

What Is Impaired Life Insurance? Some Key Factors

| Topic | Description |

|---|---|

| Impaired Life Insurance | Insurance is designed for individuals with health conditions or lifestyle factors that increase their risk. |

| Impaired Risk | A health or lifestyle factor that reduces an individual’s ability to secure the best life insurance rates. |

| Underwriting | The process by which insurers evaluate the risk of insuring a potential policyholder. |

| Premiums | The amount paid for insurance coverage can be higher due to the increased risk. |

Factors Affecting Impaired Risk Life Insurance

| Factor | Impact on Insurance |

|---|---|

| Health Conditions | Diseases like cancer, heart issues, or diabetes can increase premiums. |

| Lifestyle Choices | Factors such as smoking or engaging in high-risk activities can elevate risk levels. |

| Age and BMI | Older age and higher BMI can lead to increased premiums. |

Underwriting Considerations

| Consideration | Description |

|---|---|

| Medical Records | Insurers review medical history to assess risk. |

| Health-Related Questions | Applicants may be asked about their health status. |

| Medical Examinations | In some cases, a medical exam may be required before offering a quote. |

Which Are The Most Commonly Recognised Impaired Life Insurance Conditions?

The most common conditions that typically qualify as impaired risks for life insurance include:

- Cancer: Various types, stages, and histories of cancer can impact life insurance eligibility and premiums. Many people with skin cancers can, however, secure cover at standard terms.

- Heart Disease: Conditions such as coronary artery disease, heart attacks, and heart failure.

- Diabetes: Both Type 1 and Type 2 diabetes, mainly if poorly controlled or with complications.

- High Blood Pressure (Hypertension): When combined with other health issues or if it is poorly controlled.

- High Cholesterol: High levels can increase the risk of heart disease, which may impact life insurance rates.

- Obesity: A high body mass index (BMI) can lead to various health issues and make insurance more costly.

- Mental Health Issues: Including depression, anxiety, and other mental health conditions that can impact life expectancy.

- Respiratory Diseases: Chronic obstructive pulmonary disease (COPD) and asthma are particularly severe cases.

- HIV/AIDS: While treatment has advanced, HIV can still affect life insurance eligibility and rates.

- Stroke: A history of stroke, including mini-strokes (TIAs), can impact insurance terms.

- Kidney Disease: Chronic kidney disease and those requiring dialysis can impact insurance.

- Liver Disease: Conditions like cirrhosis or hepatitis C can affect life insurance rates and eligibility.

Honesty Is the Best Approach

Cancer patients, heart attack victims, and diabetics may find themselves paying premiums that are more than the typical cost of life coverage.

There is a way around this, which allows people with pre-existing medical conditions to purchase affordable life cover. If health has or continues to suffer, rest assured that loved ones can still be provided for through a life insurance policy.

However, applicants should never lie about their age or medical status on a life insurance application. While they might enjoy easy acceptance and lower premiums now, beneficiaries may be affected.

If the policy was issued based on false information, the insurer will not be obligated to pay out when a claim is filed.

After all those years of making premium payments, the insured could die and leave beneficiaries with nothing. This risk is not worth the temporary reward.

Major life insurance companies have different attitudes toward consumers with pre-existing medical conditions.

Some will consider applications from these individuals, and others prefer to pass due to the increased level of risk. Using an independent broker that provides quotes across the life insurance market can be worthwhile because it may result in some surprises.

When the insurer receives the policy application, it considers medical records, asks the applicant health-related questions, and may question the general practitioner.

Sometimes, the company will require the applicant to submit to a medical exam before providing a quote. The result may be a declined application or a life policy containing no exclusions but an increased premium that reflects the higher risk due to the medical condition.

Most consumers with pre-existing medical conditions can obtain life insurance if they are willing to pay the premiums offered.

Those rejected by mainstream insurers can find acceptance from an intermediary that specialises in non-standard and complex risks. This is where Insurance Hero would be happy to help you.

For example, some companies provide life cover to diabetics who have suffered from both strokes and heart attacks. However, they can decline applications from individuals with certain pre-existing medical conditions, such as Alzheimer’s disease.

Typical Premiums

An individual who is 35 years old and has no health issues should expect to pay approximately £12 a month for £150,000 worth of 25-year term life insurance.

If this individual has a body mass index of 33, premiums increase 50 percent to approximately £17 per month.

Premiums will typically increase 100 percent to £23 per month for a 35 year-old applicant diagnosed with multiple sclerosis who experienced symptoms within three to five years of applying for cover.

Someone who is 35 years old and had a heart attack six months before completing a life insurance application is likely to be declined by a significant life insurance carrier.

However, someone who is 45 and experienced a heart attack six months before applying may be approved after waiting an additional six months.

The typical premium would be at least £46 monthly, a 300 percent increase from the premium offered to a healthy 35-year-old.

A person aged 35 who was diagnosed with Stage 1 breast cancer three years before applying, whose treatment was successful, and who has experienced no spread of cancer will be charged approximately £53 per month for the first five years.

After this period, the premium may revert to approximately £13 monthly, the standard premium for a healthy individual of that age.

Providers Of Impaired Life Cover

Finding life insurance with health issues can be challenging, but the market has become more accessible. Many mainstream and specialist insurers now offer options for individuals with impaired or higher risk profiles.

At Insurance Hero, we work with a wide network of providers to match your circumstances with the most suitable policy, whether you’ve faced rejections before or are applying for the first time.

We also offer guaranteed acceptance plans for those aged 50–90, with no medical questions required.

Please feel free to get in touch with our team today. We’d be delighted to help, and there is no obligation to proceed if you don’t wish to.

Spotlight On Two Top UK Insurers Offering Impaired Cover

These mainstream insurers are generally accessible directly or through brokers such as Insurance Hero, and each has processes in place to assess and offer life insurance to impaired applicants.

Scottish Widows

Scottish Widows is a long-standing UK insurance company renowned for offering life cover, including options for individuals with existing health conditions.

Important Points To Note:

- Their underwriting process takes individual medical histories into account, offering personalised terms.

- Policies are available as term or whole-of-life, with pricing and conditions set according to the assessed level of risk.

- All Scottish Widows Protect policies include access to Scottish Widows Care, delivered in partnership with RedArc.

- This service provides ongoing practical and emotional support to policyholders and their families who are facing illness, loss, trauma, or post-hospital recovery.

Common Factors Across All Insurers

- Costs: Premiums are typically higher due to elevated health risks.

- Medical Review: Providers often request detailed health information and may require medical examinations.

- Exclusions: Certain conditions may be excluded based on your medical history.

- Policy Options: Choices typically include term life, whole-of-life plans, over-50s plans, and sometimes critical illness coverage.

- Eligibility: Acceptance depends on your specific condition and varies between insurers; comparing offers is key.

Scottish Provident

Scottish Provident is a major UK insurer open to applicants with various health conditions. They provide term life, whole-of-life, and over-50s policies.

Important Factors To Consider:

- While premiums may be increased for higher-risk individuals, many are still eligible.

- Applications may involve additional medical questions or assessments, with final terms determined by the nature and stability of the condition.

- They include terminal illness cover as standard with all life insurance policies lasting two years or longer.

- They offer a waiver of premium option, which keeps your life insurance active without requiring payments if you’re unable to work due to illness or injury after a specified period.

Steve Case is a seasoned professional in the UK financial services and insurance industry, with over twenty years of experience. At Insurance Hero, Steve is known for his ability to simplify complex insurance topics, making them accessible to a broad audience. His focus on clear, practical advice and customer service excellence has established him as a respected leader in the field.