Compare Whole Of Life Insurance Quotes 2026

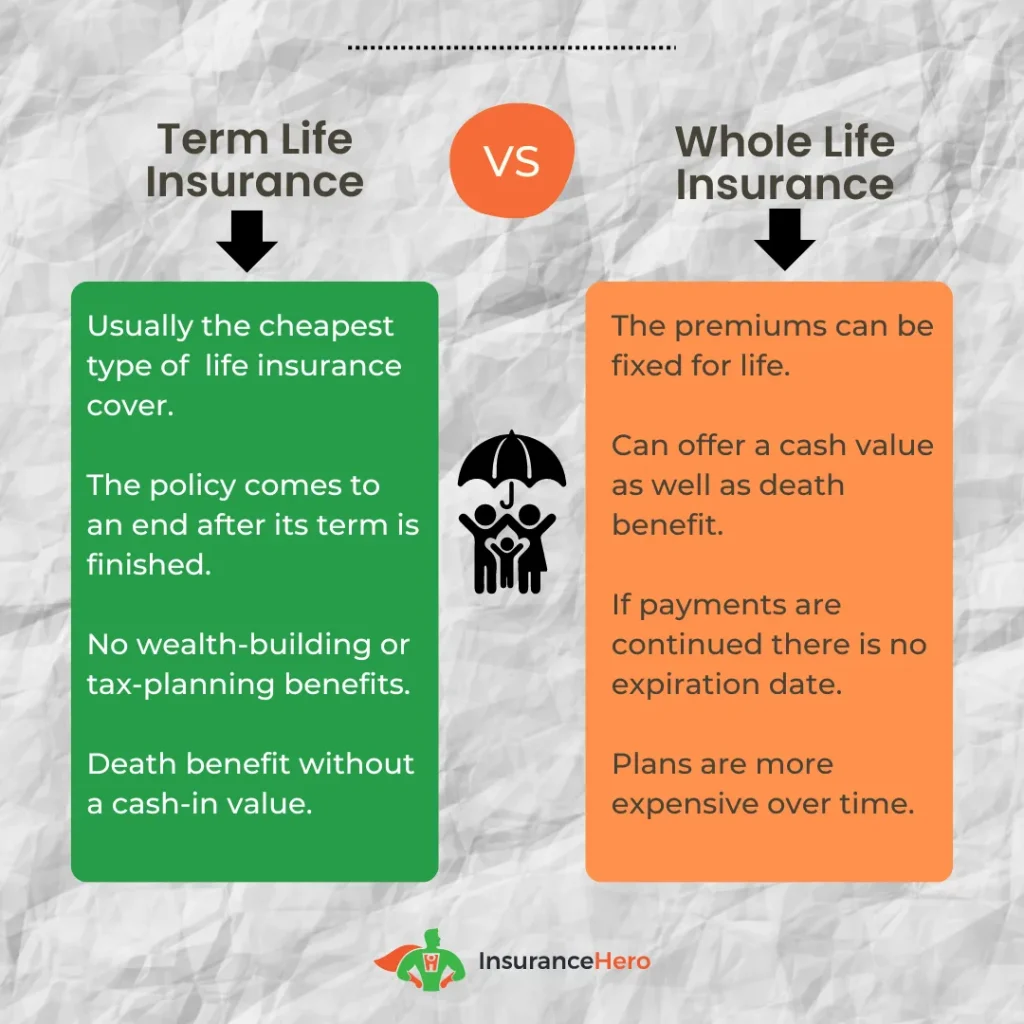

While a term life insurance policy lasts for a specific timeframe, a whole of life insurance policy lasts for the lifetime of the insured.

How a Whole of Life Policy Works in 2026

A whole-of-life insurance policy will always pay out, providing beneficiaries with a lump sum of money. Since payment is guaranteed, this coverage can be more expensive than term life insurance.

However, it is a convenient way to provide surviving family members with funds, and it can be combined with other insurance, such as a term policy, to cover specific debts.

The insurance company invests the monthly premiums paid for a whole-of-life plan. For the first ten years of the policy, premiums and coverage levels do not increase. After that time, the insurance company reviews the plan and may increase the premiums.

Whole Of Life Insurance In Summary:

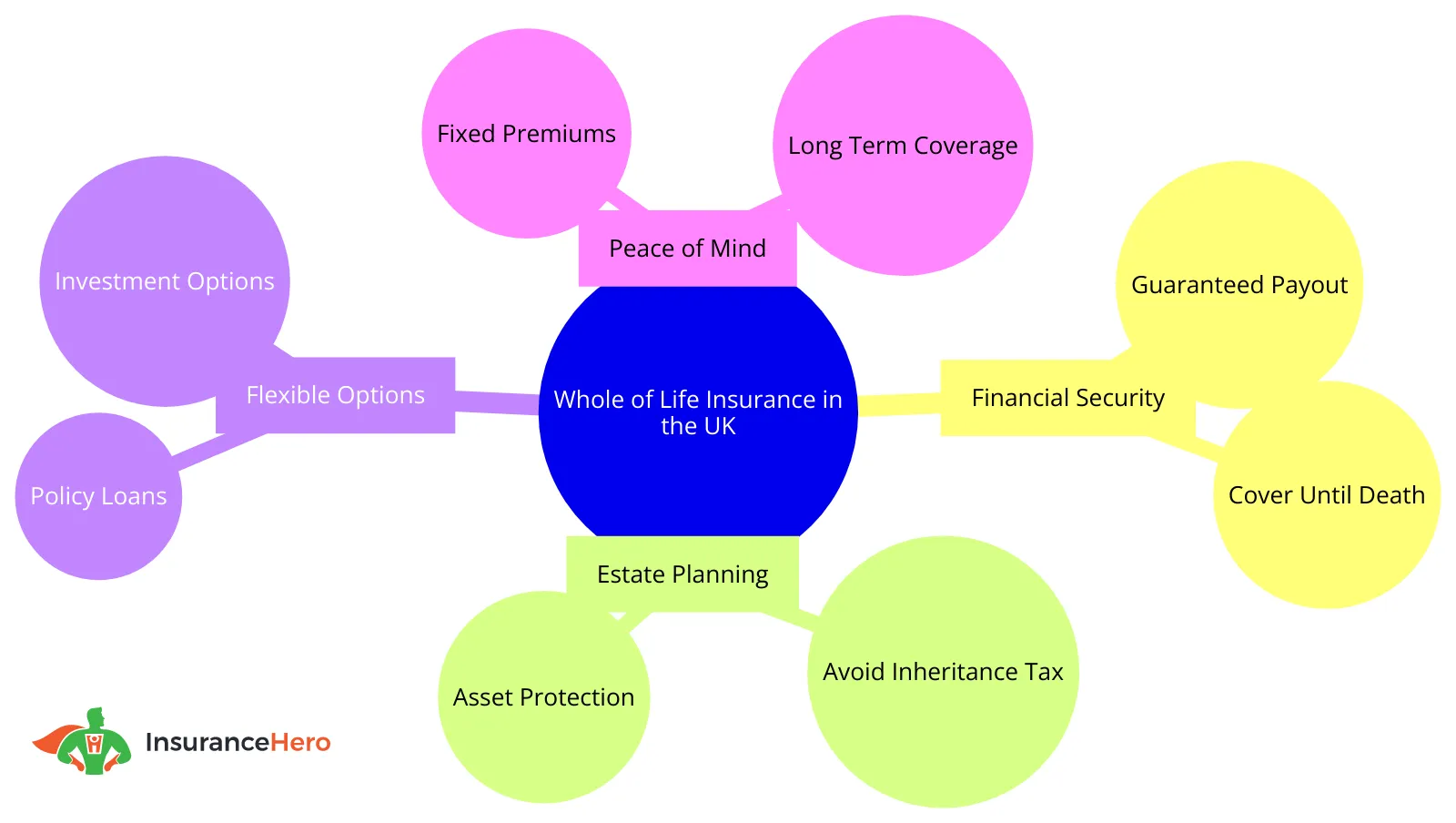

Secure your financial future and ensure peace of mind for your loved ones with a policy that guarantees a payout no matter when you pass away.

Insurance Hero can help you find the most comprehensive and cost-effective policies available, including insurers not often seen on the usual comparison websites.

Here’s why it’s worth considering this type of insurance:

- Guaranteed Security for Your Family: A whole-of-life insurance policy provides a lump-sum payout to your beneficiaries, helping them cover expenses such as debts, funeral costs, and maintaining their lifestyle.

- Flexible Premiums with Fixed Option Available: You can choose a premium payment structure that suits your financial situation, including fixed premiums that do not increase over time. This makes it easier to plan your financial future without worrying about rising costs.

- Potential for Additional Coverage: It can be combined with other policies, such as critical illness cover, to provide comprehensive protection. It’s also possible to place the policy in a trust to avoid inheritance tax, ensuring your beneficiaries receive the full financial benefit.

Compare The Best Whole Life Insurance Providers. Find The Right Life Insurance Now.

Increases are typically made in five-year increments

As the insured ages, premiums may increase. This could eventually make the coverage more expensive for some people. We aim to make the whole life insurance quote process as streamlined and straightforward as possible.

Whole life insurance offers a fixed premium option. Though the premium will not increase, it will be higher from the start.

This concept is based on assumptions about the growth in the investment value resulting from premium payments.

If the fund performs poorly or related charges increase, the premium may need to be raised to maintain coverage.

Whole-of-life premiums are based on the age, sex, smoking status of the insured and the level of coverage. Older or retired people will pay higher premiums than younger people.

Women generally pay lower premiums because they tend to live longer. A nonsmoker, commonly defined as an individual who has not smoked in the past 12 months, will pay a lower premium than a smoker.

To prevent the cash benefit from being included in an estate and subject to inheritance tax, a whole of life policy must be written in a trust. Insurance companies provide this service at no charge or for a small fee.

Individuals should seriously consider placing the policy in a trust because it may affect the overall value of the estate.

The policy payout can be used to pay for funeral expenses, final bills, and the mortgage balance to maintain the lifestyle of the beneficiaries.

Which Whole Life Insurance Is The Best?

After thorough research, we have determined that the UK life insurance companies in the table below were often suggested to be the best for Whole-Of-Life Insurance:

| Company | Plan Name |

|---|---|

| ⭐Vitality | Whole of Life Protection Plan (Our best value life insurance firm in this category for 2026) |

| Royal London | Pegasus Whole of Life Plan |

| NFU | AIG Whole of Life Insurance |

| Zurich | Adaptable Life Plan |

| Scottish Widows | Protect Whole of Life Cover |

| Aegon | Whole Life Plans and Critical Illness |

| AIG Life | Whole Life Insurance or Care Coverage |

| LV= | LifeTime+ |

| Old Mutual | Protect Guaranteed Whole Of Life Plans |

Benefits of Whole of Life Coverage

A guaranteed lump sum payout is the primary benefit of these plans. With a term life insurance plan, a payout occurs only if the insured dies within the stated period.

Older people in poor health often choose a whole-of-life plan because it does not require a medical examination. Though they will pay higher premiums due to age, their health status will not affect this figure.

This type of policy can be combined with other coverage, such as critical illness, to protect the insured in life and death.

However, a policy may provide only a single payout if death occurs after a critical illness diagnosis, so consumers should ask about this before purchasing coverage.

Buying whole-of-life and critical illness policies separately may be a better decision because two payouts will be made if a critically ill insured dies.

Whole Life Insurance Cost In The UK

The table below indicates example costs. The best whole life insurance quote is based upon a non-smoker in good health needing £100,000 of cover:

A cheap whole life insurance policy is possible, but compared to other types of coverage, these plans will always cost more, mainly due to their long policy durations and guaranteed payouts.

| Your Age | Whole Of Life Cover Cost |

|---|---|

| 30 | £71.03 |

| 35 | £82.91 |

| 40 | £100.89 |

| 45 | £122.64 |

| 50 | £124.36 |

How Many Years Do You Pay A Whole Life Insurance Policy For?

In the UK, the duration of premium payments can vary depending on the policy and insurer.

Generally, there are three primary premium payment structures for whole life insurance policies:

- Pay premiums for life: This is the most common premium payment structure for whole life insurance policies in the UK. In this case, policyholders must pay premiums until death or the policy is surrendered. The policy remains active as long as premiums are paid, and the beneficiaries will receive a lump-sum payout upon the insured’s death.

- Limited payment term: Some insurance providers offer a limited payment term for whole life insurance policies. With this structure, policyholders pay premiums for a predefined number of years, such as 10, 15, or 20. Once the payment term is complete, the policy is considered paid up, and no further premiums are required. The policy remains in effect for the insured’s entire life, and the lump-sum payout will be paid to the beneficiaries upon the insured’s death.

- Age-specific premium payment term: In this structure, policyholders pay premiums until a specific age, such as 65, 75, or 85. Once the insured reaches the specified age, the premium payments stop, but the policy remains active for the rest of their life. The beneficiaries will receive a lump-sum payout upon the insured’s death.

Reviewing the terms and conditions and understanding the premium payment structure are essential when looking for the best whole life insurance policy.

Each insurance provider may have different options and requirements, so comparing policies and choosing one that suits your financial goals and circumstances is important.

What are the drawbacks of whole-of-life coverage?

Policy premiums are higher than term life premiums because they include a guaranteed payout. If a policy has been in place for a long time before the insured’s death, the premiums paid may exceed the monetary benefit.

Our whole vs term life insurance guide goes into great detail, and you might want to read it if you are still undecided.

Therefore, though whole of life insurance premiums will be less expensive for a younger insured, this individual may end up paying much more than the policy value if he or she has a long lifetime.

Most policies require premium payments until the insured reaches a specific age. This means that some individuals will pay premiums until their death.

Failing to include this policy in a trust may delay payouts to beneficiaries and substantially increase the inheritance tax owed on the estate.

Types of Whole of Life Insurance Policies:

| Policy Type | Description |

|---|---|

| Non-investment Whole of Life | Provides a guaranteed lump-sum payout upon the insured’s death with no investment component. Premiums are generally fixed and based on factors such as age, gender, and health. |

| Investment-linked Whole of Life | It offers a guaranteed lump-sum payout and an investment component, where a portion of the premiums is invested in various funds. The policy’s value can grow or decrease depending on the performance of the selected funds. |

Whole of Life Insurance Riders

| Rider | Description |

|---|---|

| Waiver of Premium | Covers the policyholder’s premium payments if they are unable to work due to illness or injury. |

| Accidental Death Benefit | Provides an additional lump sum payout if the insured’s death is due to an accident. |

Further Considerations

Since this insurance is also an investment, people should review the historical performance of the funds the insurance company uses.

If performance was poor in the past, this might increase the likelihood of poor performance. In some cases, an increase in the monthly premium may be required to maintain the coverage level.

If the plan features a fixed premium, the insured should inquire about the rate of investment growth used to calculate the policy premiums.

A lower rate is viewed as positive because it is the minimum growth rate required to maintain a given premium.

Comparing whole-of-life insurance quotes from the top providers is just the beginning of the research required.

Policy terms and conditions vary, so consumers should understand what their coverage includes, how premiums are calculated, whether premiums will increase, and, if so, how often.

Consumers can learn more about whole life insurance by reading information on our site and reviewing the documents provided by the quoted insurance companies to compare whole life insurance rates.

Factors Affecting Whole of Life Insurance Premiums:

| Factor | Impact on Premiums |

|---|---|

| Age | Older individuals typically pay higher premiums due to their shorter life expectancy. |

| Gender | Women generally pay lower premiums than men because they tend to live longer. |

| Health | Pre-existing conditions and poor health management of health issues can lead to increased premiums. |

| Occupation | Risky occupations and sports may lead to higher premiums due to an increased likelihood of accidents or health issues. |

| Lifestyle | Smoking, excessive alcohol consumption, or dangerous hobbies can result in higher premiums. |

Compare Whole Of Life Insurance (Top 3 Companies)

Aviva

| Topic/Feature | Notes |

|---|---|

| Policy Name | Whole of Life Protection Plan |

| Purpose | No payout for suicide, intentional and serious self-injury, or in the event where the life insured took their own life (in the insurer’s reasonable opinion) |

| Lump Sum Payment | Yes, after the policyholder’s death |

| Access to Wellbeing Support | Included as standard |

| Fast Underwriting Decisions | 83% receive an instant decision |

| Joint Policies Options | Joint life first death or joint life second death basis |

| Accidental Death Benefit | Included |

| Changing Your Policy Option | Additional cost: no premium payment is required after 26 weeks if the client can’t work due to illness or injury |

| Waiver of Premium Option | Remains the same until a claim is made, unless increasing cover (indexation) is chosen |

| Protection Against Inflation | Option to choose increasing cover in line with Retail Prices Index |

| Wellbeing Support | Personalised, practical, and emotional telephone support from a registered nurse (provided by RedArc Assured Limited) |

| Minimum Cover | Set by minimum premium |

| Maximum Cover without Increasing Cover Option | Up to age 69 – £5 million; Age 70 to 79 – £2 million; Age 80 to 84 – £1 million |

| Maximum Cover with Increasing Cover Option | Life insurance cover up to the age of 70 – £2 million; Age 71 to 84 – £1 million |

| Type of Cover | Guaranteed unless the increasing cover option is chosen at the outset |

| Term | Covers the client for the whole of their life |

| Minimum Age | 18 years old (life of another policy can be taken on a 17-year-old by an adult with insurable interest) |

| Maximum Age | 84 years old |

| Premiums | Guaranteed unless the increasing cover option is chosen at the outset |

| Trusts | Policies can be placed in trust |

| Increasing Cover (Indexation) | Optional, increases each year with RPI changes up to 10%; if chosen, the premium also increases using the change in RPI multiplied by two |

| Waiver of Premium | Optional, can be included for an additional cost (eligibility criteria and restrictions apply) |

Vitality

| Topic/Feature | Notes |

|---|---|

| Product | Whole of Life Insurance |

| Company | Vitality |

| Rating | 5 Star Defaqto-rated cover |

| Payout | Guaranteed when you die |

| Premium Payment Options | Monthly or annual premiums |

| Payout Amount | Stays the same throughout your life |

| Reasons for Whole of Life Insurance | Peace of mind, help with inheritance tax |

| Cover Options | LifestyleCare Cover, Premium Step, Traditional Whole of Life |

| Discount | 40% of the estate value is over £325,000 |

| Claims Paid | 99.8% (2023) |

| Inheritance Tax | 40% of the estate value over £325,000 |

| Additional Products | Serious Illness Cover, Income Protection Insurance, Term Life Insurance, Mortgage Protection Insurance |

Royal London Whole Of Life Cover Plan

| Topic/Feature | Notes |

|---|---|

| Plan Name | Whole of Life Plan – Royal London |

| What does it cover? | Whole of Life Cover pays an amount of money if you die or develop a terminal illness. |

| Features | Payout as a lump sum, option to increase or maintain cover, possible cover increase without further medical evidence, Helping Hand service, and an optional Waiver of Premium add-on. |

| Age to apply | UK residents aged between 18 and 89 |

| Plan continuation | Continues until you die or stop making the monthly payments |

| Partner Insurance | Stays the same over the full term of the plan unless you choose reviewable payments or increasing cover |

| Medical questions and examination | Your plan can be used to insure you and your partner if needed |

| Cash-in value | There is no cash-in value at any point in time |

| The whole of Life Plan – Royal London | Your plan can be used to insure you and your partner if required |

| How to buy | Whole of Life Cover can be arranged through a financial adviser |

| Royal London | A mutual company with a focus on customers offers the Helping Hand service with every Whole of Life plan and has received several awards |

| Claims | 99.5% of claims were paid in 2025 |

| Whole of Life cover purpose | Helpful for leaving money for the family, paying off a mortgage, or assisting in paying for a funeral |

Is Whole of Life Coverage Right for You?

Life insurance coverage is a serious matter, so it is essential to consider all the options. Whole-of-life coverage is suitable for someone who wants a guaranteed payout to beneficiaries and is willing to pay for it.

Older people with health issues may find this coverage more attractive than a term life policy because it does not feature a medical examination.

Like term life insurance, the lump sum benefit can be used for any purpose, including final expenses and funeral costs.

If you decide that whole-of-life coverage is suitable, complete and submit the whole life insurance quote form on our site.

We will research the market to find the best policies and return them to you with the best whole-of-life insurance quotes.

To compare whole life insurance, you can receive answers to your questions from our experts.

You can then select the policy that best fits your needs and apply for coverage so your family is financially protected, regardless of when you die.

Insurance Hero can help you by providing quotes that fit your individual needs and those of those close to you.

Benefits Of Whole Of Life Cover Mind Map

Alternatives to Whole of Life Insurance:

| Alternative Insurance Option | Description |

|---|---|

| Over-50s Life Insurance | A type of whole of life insurance specifically designed for individuals over 50 years of age, often with no medical examination required. Guaranteed acceptance, but typically offers lower coverage amounts. |

| Endowment Policy | A type of whole-of-life insurance specifically designed for individuals over 50 years of age, often with no medical examination required. Guaranteed acceptance, but typically offers lower coverage amounts. |

| Family Income Benefit | A type of life insurance that provides a regular tax-free income to the beneficiaries instead of a lump sum payout, usually paid monthly or annually for a specified period after the insured’s death, and often used to maintain family income. |

Case Study: The Thompsons – A Young Family’s Journey with Whole of Life Insurance

Meet the Thompsons, a young couple living in the UK with their two children, Emily and Jack.

With the responsibility of raising their kids and caring for Mrs Thompson’s elderly mother, they felt the need to secure their family’s future.

After Insurance Hero conducted a whole life insurance comparison on their behalf, they decided to take out a policy.

Benefits for the Thompsons and Their Loved Ones:

- Peace of Mind: Knowing that their children and Mrs Thompson’s mother will be financially secure in the event of unforeseen circumstances gives the Thompsons significant peace of mind.

- Financial Security: The policy ensures that their loved ones receive a lump-sum payout to cover living expenses, education, and other essential needs.

- Flexibility: The Thompsons can adjust their policy as their needs change, ensuring their coverage always aligns with their family’s requirements.

- Tax Benefits: The payout from the policy is generally tax-free, ensuring that their loved ones receive the full benefit.

The Thompsons’ Journey:

- Research: They started by searching for a whole life insurance quote online. They wanted to get a quote online to save time and compare different options at their convenience.

- Decision: After reviewing various quotes, they wondered if whole life insurance was worth it. They concluded that the long-term benefits, especially the security it provides to their children and Mrs Thompson’s mother, made it a worthy investment.

- Policy Selection: They opted for a permanent life insurance policy, which ensures that their coverage will not expire as long as they pay their premiums.

- Peace of Mind: With their policy in place, the Thompsons now live each day with the assurance that their loved ones are protected.

The Thompsons’ decision to invest in a whole-of-life insurance policy has provided them with the assurance that their loved ones will always be taken care of.

Their story highlights the importance of conducting a thorough whole life insurance comparison and understanding the long-term benefits of such a policy.

Considerations

Entire life insurance can be worth it if you want lifelong coverage and have specific financial planning goals.

However, it’s essential to carefully consider your needs and understand the costs involved to ensure it’s the right choice for your circumstances.

The following points are worth thinking about:

- Financial Goals: If your primary aim is to provide financial security for dependents during your working years, term insurance might be more cost-effective. Whole-of-life insurance is better suited for long-term financial planning, such as estate planning or leaving a legacy.

- Affordability: Assess whether you can afford the higher premiums over the long term.

- Health and Age: Your health and age can significantly affect your premium costs. The younger and healthier you are when you take out the policy, the more affordable the premiums will likely be.

- Investment Performance: If you’re considering a policy with an investment component, it’s important to understand how the cash value is invested and the potential risks and returns.

Whole Of Life Insurance FAQs

Is it worth getting whole-of-life insurance over 60?

Yes, Life insurance is something everyone should have, regardless of age.

Here are a few reasons why having life insurance over 60 is especially important.

First, the older you get, the more likely you are to need it. Second, if something happens and you don’t have life insurance, your loved ones must bear the financial burden.

So yes, it’s worth getting life insurance over 60. Shop around and find the best policy for you and your family.

At what age is it best to buy whole life insurance?

The age at which you buy whole life insurance depends on your circumstances.

However, buying whole life insurance when you are young is usually best, as it ensures you get the most out of your policy.

When you are young, you are likely to be in good health and have fewer commitments, which means you can afford higher premiums.

You will also have more time to build your cash value, which can later help cover your policy costs.

Does whole life insurance have cash value?

UK whole life insurance does not have a cash value component. The policy is designed to pay out upon the policyholder’s death.

However, investment-linked whole life insurance policies available in the UK do offer a cash value component.

These policies allow you to invest your premiums in various funds. If the fund performs well, its value will grow over time. However, there is always the risk of losing money if the fund’s value decreases.

Does a Whole of Life Insurance Payout Incur Taxes?

Lump-sum beneficiaries from a whole life insurance policy are exempt from income and capital gains taxes.

However, if the estate’s total value exceeds the inheritance tax thresholds, a 40% inheritance tax may apply to the payout. To avoid this, placing the life insurance policy in a trust can shield it from inheritance tax.

Is Joint Whole of Life Insurance Available?

Joint whole-of-life insurance policies are available for two people.

These policies provide a single payout upon the death of the first policyholder, after which the surviving individual is no longer covered.

While premiums for joint policies are generally lower than purchasing two individual policies, it is advisable to evaluate whether separate policies are more suitable for your specific needs.buying two individual policies, it is advisable to evaluate whether separate policies are better suited to

Can I get whole-of-life insurance with poor health?

Obtaining coverage for a pre-existing condition is feasible, though it may be more expensive, and fewer insurers may be available.

Over 50s life cover guarantees acceptance regardless of health but includes a 12-24 month claim waiting period.

If death occurs within this period, only paid premiums are returned, not the total payout.

How much more expensive is whole life insurance than term?

Whole life insurance in the UK is generally 5 to 10 times more expensive than term insurance.

This is because whole life insurance offers lifelong coverage and includes an investment component, whereas term insurance covers a specific period.