Term Life Insurance Quotes 2026

Term life insurance, sometimes called temporary insurance, is life insurance that runs for a specified time.

Life is unpredictable – something can happen at any time, and because of that, we should be prepared for every possibility.

One of the best ways is to get a term life insurance policy. However, given how many different life insurance policies there are, understanding which one is best for you can be quite a hassle.

One of the most commonly chosen options is term life insurance (which also applies to high-net-worth individuals) – this is ideal for those who’d still like to be protected but don’t want to commit to a whole life policy.

How does this type of life insurance work? What does it cover? What can it be used to cover? Find the answers to these questions and more below.

Compare The Top UK Term Life Insurers Now ⏱ Takes About 60 Seconds.

Below is a comparative analysis of the costs associated with a term insurance plan versus a decreasing term insurance plan.

The quotations provided are for a £100,000 policy, spanning 30 years, and are calculated for an individual in good health who does not smoke.

| Your Age | Level Term Life Insurance | Decreasing Term Life Insurance |

|---|---|---|

| 20 | £4.52 | £4.67 |

| 25 | £5.28 | £4.93 |

| 30 | £5.81 | £5.17 |

| 35 | £7.84 | £6.03 |

| 40 | £10.39 | £7.92 |

| 45 | £15.31 | £10.84 |

| 50 | £25.82 | £17.11 |

Quick Guide to Choosing the Best Term Life Insurance

| Criteria | Details |

|---|---|

| Coverage Amount | Ensure the coverage amount meets your family’s needs in your absence. |

| Term Length | Choose a term that covers you until your financial obligations decrease. |

| Premium Cost | Consider both your budget and the potential payout. |

| Policy Features | Look for policies with terminal illness cover and flexibility in terms. |

| Provider Reputation | Research customer reviews and claimed payout rates. |

| Additional Benefits | Some policies offer benefits like funeral pledges or critical illness cover. |

How Does Term Life Insurance Work?

As we mentioned earlier, term life insurance is a type of life insurance policy that is valid only for a specific period.

Typical term lengths for a term policy are 10, 15, or 20 years, although shorter terms are available.

If the policyholder dies during the covered period, the policy beneficiaries receive a lump-sum payment.

The cash sum can cover funeral costs, childcare costs, mortgage repayments, other financial commitments, living expenses, or outstanding debts.

A term policy allows a working individual to ensure that the lifestyle of surviving beneficiaries does not change drastically upon his or her death.

How to Choose the Time Frame

When considering term life insurance, one of the most important things you need to consider is how long you want to be insured.

Consumers should select a term that lasts until dependents reach an age of financial self-sufficiency, and working adults should choose a term that runs until their retirement savings take over.

Due to the current economy, many people have tapped into their savings, so this period may be longer than initially anticipated.

However, spending the extra money to extend the term will be worth it if the insured dies within the coverage period.

| Company | Plan Name |

|---|---|

| ⭐Scottish Widows | Protect Personal with lower premiums (Our best value life insurance provider in this category for 2026) |

| LV= | Flexible Protection Plans |

| Nationwide Building Society | Multi-Protection |

| Sainsbury’s Bank | Level Term Insurance |

| Barclays Bank | Mortgage Protection Plan |

| Zurich Insurance | Life Protection |

| AA (From L and G) | Mortgage Protection and family income benefit |

| Aviva | Life Insurance |

| VitalityLife | Comprehensive or combined cover |

How to Get a Term Life Insurance Policy

You can get a term life insurance policy through your employer or privately. The Insurance Hero team would be happy to help you with this.

Employer Term Life Insurance

Suppose your employer offers a life insurance policy as part of the benefits package. In that case, it is most likely group life insurance, which covers a specific group of people.

There are some advantages to getting an employer’s life insurance. First, the chances of getting declined life insurance cover are lower.

Usually, employers put you on it when you are hired without asking any questions.

This means that factors like your health or family medical history don’t affect your eligibility, unlike when you get your own life insurance policy.

Secondly, depending on your health and age, an employer’s life insurance might be more affordable than buying it privately.

That’s because the premium is based on the state of the whole group, not on individual people.

Finally, you will most likely enrol in life insurance at the same time as other benefits, so you don’t have to fill out any additional documents.

Also, many employers won’t ask you to pay for the insurance separately—they will deduct the right amount from your salary, so you don’t have to remember to pay the monthly premium.

However, employer-term life insurance also has some disadvantages. One of the most important ones is that you usually have a restriction on how much life insurance you can get – depending on your financial obligations, you might need more than what is offered.

Secondly, employer life insurance has a limitation – it is only valid during employment. Once you leave your job, your term life insurance will most likely be stopped.

Private Term Life Insurance

If you’re self-employed or, for whatever reason, you can’t or don’t want to take advantage of employer term life insurance, you can buy one individually.

There are certainly advantages to it. First, you are not restricted by your job, so your life insurance won’t be affected even if you change positions several times.

You also have the option to choose which of the life insurance providers you want to go with. This is usually not the case with an employer’s life insurance policy, as they tend to stick to one insurer.

Finally, suppose you have better health than those you work with (for example, you’re working with many older people with pre-existing medical conditions).

In that case, you will more likely pay lower premiums than if you use the group life insurance policy.

That’s because the healthier you are, the lower your monthly payments will likely be.

Are there any disadvantages? Yes, however, they aren’t that serious.

The one you will probably feel the most is that taking out a life insurance policy on your own, whether term or whole life, requires more paperwork than employer life insurance.

You might also be asked to undergo medical examinations – this is part of the standard life insurance policy process and doesn’t always happen, but you should still be aware that it can.

Types Of Term Life Coverage

Another thing you will have to decide on, which will affect your term life insurance cost, is the type of life insurance.

There are three main types of life insurance: level, increasing, and decreasing term life insurance.

Level term life insurance features fixed coverage and premiums for a specific number of years and makes a full payout for a claim filed within that period.

This type of life insurance is usually the best choice for an individual with an interest-only mortgage or one seeking financial protection for a family.

Increasing term policies cost more than a level term or decreasing term coverage. The premium and coverage increase each year without requiring a health examination.

The coverage increase accounts for income and inflationary increases over the years. This type of coverage is not as popular as the alternatives, but it does have its merits.

Decreasing life insurance is a less expensive option because the monthly premiums start lower and decrease over the years, as does the payout.

A decreasing term policy is designed to reduce the benefit in line with the balance on a repayment mortgage. It is an attractive option for people on a restricted budget who are only concerned with covering mortgage payments upon their death.

Some term policies are short-term, renewable policies. Initially, these policies may be less expensive than the other options.

However, they are usually more expensive over the long term. A particularly attractive feature of this life insurance policy type is that it may be renewed without supplying medical evidence.

Increasing term policies cost more than level term or decreasing term coverage. The premium and coverage increase each year without requiring a health examination.

The coverage increase accounts for income and inflationary increases over the years. This type of coverage is not as popular as the alternatives, but it does have its merits.

Decreasing term insurance is a less expensive option because premiums start lower and decrease over the years, as does the payout. A decreasing term policy is designed to reduce the benefit in line with the balance on a repayment mortgage.

It is an attractive option for people on a restricted budget who are only concerned with covering mortgage payments upon death.

Some term policies are short-term policies offered on a renewable basis. Initially, these policies may be less expensive than the other options, but are usually more costly over the long term.

A desirable feature of this policy type is that it may be renewed without supplying medical evidence.

Premium Calculations For Term Policies

Insurance companies consider many factors when calculating the premium for a term life policy.

Here are some of the personal circumstances that can (and most likely will) affect how much you will have to pay each month for your life insurance:

- Age– The older you are, the more you might have to pay for your life insurance. Also, depending on your age, finding a life insurance provider might be more difficult, as some providers have a maximum age limit for policies.

- Sex – women tend to have lower monthly payments because their life expectancy is longer than men’s.

- Your medical history – It is not uncommon for a life insurance provider to ask you to undergo a medical examination (it won’t always happen, but it can). Those with pre-existing medical conditions such as high blood pressure, cancer, or diabetes might have to pay higher monthly payments.

- Your family’s medical history – while your health is important, your family’s health history is also crucial. If multiple family members experienced serious illness (for example, if both your mother and your grandmother had breast cancer), your life insurance premiums might be higher.

- Lifestyle– Your lifestyle is another factor affecting your monthly life insurance payments. For instance, if you’re a fan of dangerous activities such as mountain climbing or skydiving, you might face more expensive life insurance. The same goes for not taking care of yourself, such as smoking or excessive drinking.

- Occupation—Depending on your job, you might be faced with higher life insurance costs. Some professions that pay more for it include firefighters, miners, policemen, and construction workers.

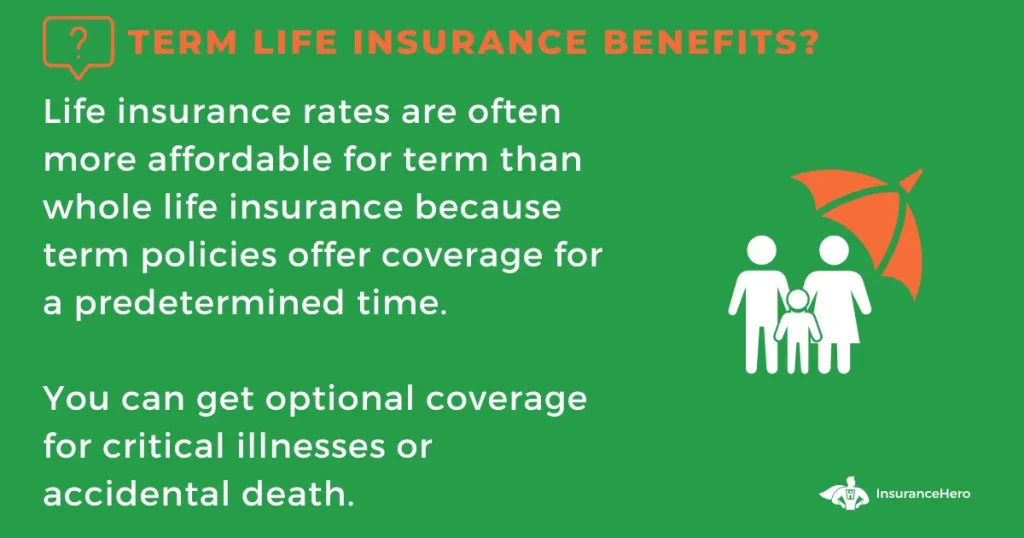

The policy type also plays a role, with term policies costing less than whole-of-life policies due to their limited coverage period. If options like critical illness cover or income protection benefits are added to the policy, this will also affect the cost.

Finally, the amount you want to take out of your term life insurance will also affect your monthly payment. The lower the payout, the cheaper the life insurance will be.

The importance of the applicant‘s age cannot be stressed enough. The younger a person is when applying for life coverage, the cheaper the premium.

The premium stays the same with level term coverage throughout the coverage period.

Covered individuals save substantial money by locking in their premiums at a young age. This cash can be used to increase coverage, invest, save for retirement, or enhance lifestyle.

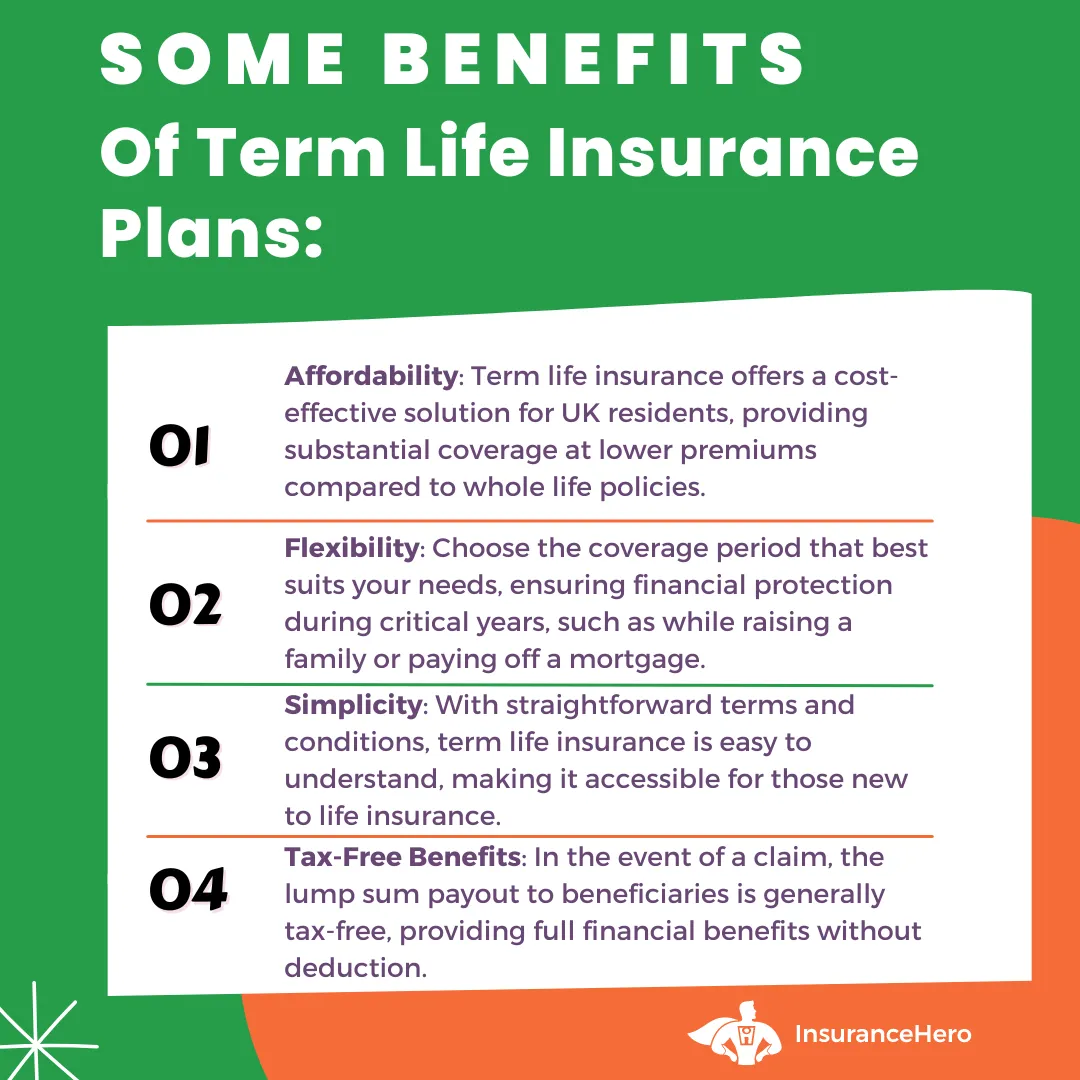

Why People Choose Term Insurance

Term coverage offers several benefits beyond affordable premiums, including the option to lock in or reduce them. The insured can select from a wide range of coverage levels.

The recommended coverage amount is £100,000, but higher and lower amounts are available.

This allows the insured to choose a level that adequately provides for beneficiaries. In addition, each spouse can purchase a separate term life insurance policy and name the same beneficiaries.

This is an inexpensive way to ensure that children are provided for when one or both spouses die.

Term life benefits can be used to pay funeral expenses, repay debts, cover childcare or educational costs for children, or provide replacement income.

Even if the family is not in substantial debt, knowing this extra money will be available in the future can be a relief. Situations can change, and it always helps to be prepared.

For most households, a mortgage is not the only expense; having a cash sum to pay other bills makes things easier.

Disadvantages of Term Insurance

Though term life insurance has many benefits, it also has a few drawbacks. Premium payments are designed to cover policy costs during a specific period.

If the insured does not die within the covered term, the policy ends, and paid premiums are not refunded. The insured may be able to extend the term, but the premium for doing so is usually higher.

With a decreasing term policy, the coverage limit decreases; by the end of the term, it is usually close to zero. If the individual becomes terminally ill within the period and knows that death will come shortly, this can create additional worry.

The individual will see the coverage level decreasing each year and know that family members will not be as well taken care of as they could have been with a level or increasing term policy.

Term Life Insurance – Frequently Asked Questions

What does term life insurance cover?

As you might have deduced already, term life insurance covers your life for an established period of time. The payout occurs when the policyholder dies within the policy’s duration.

Is it possible to have joint term life insurance?

Yes, of course. If you want joint life insurance cover with your partner, it is possible. It is usually better than having a separate life insurance policy for each spouse.

With a joint life policy, you can choose a first-to-die or second-to-die life insurance.

First-to-die life insurance is a good choice for those who want to make sure that their partner and children are taken care of in case of the other partner’s death.

Second-to-die life insurance, on the other hand, is better for those who want to leave money to heirs (also for inheritance tax) or a charity.

Can I have multiple life insurance policies?

Yes, nothing is stopping you from purchasing life insurance policies from several providers.

Is critical illness cover included in the life insurance policy?

No terminal illness cover is included in your life insurance policy. However, you can add critical illness coverage separately if that’s essential.

Remember that, since they are two separate policies, your critical illness claim will not affect your life insurance payout.

What happens if I miss payments on my term life insurance policy?

What will happen when you don’t pay your monthly premium depends on the life insurance provider. Most life insurance providers offer a 30-day grace period from the due date of your life insurance payment.

The good news is that your life insurance cover doesn’t end when you enter the grace period. So, in case you die during it, your family or whoever you intend to give the lump sum to will still receive the financial support.

What happens if I don’t die during the term insurance period?

If you don’t die during your life insurance coverage period, you might be able to extend it; however, you might have to pay higher premiums. It all truly depends on who you buy life insurance from.

Do you have to pay taxes on life insurance payouts?

No, life insurance payouts are tax-free lump sums, meaning you don’t have to pay tax on them once you receive them.

How to make a life insurance claim?

If you die during the term life insurance period, then your loved ones will most likely want to make a claim.

Thankfully, making life insurance claims is not as hard as long as you have all the necessary documents.

This would include the death certificate, a completed claim form that should be readily available on the life insurance provider’s website, and a policy document, which is simply a life insurance policy certificate issued when a policy is signed.

Your beneficiaries will also be asked to state your name and surname and the relationship you had.

In short, here is how a life insurance claim process looks:

- Contact the life insurance provider – usually, you can inform the provider by calling or emailing them. However, more and more life insurance providers allow beneficiaries to claim online.

- Prepare the required documents: the death certificate, the claim form, and the policy document.

- Receive the cash sum—once you have completed all the necessary forms and submitted all the documents, the life insurance will pay out the established amount.

If you’re wondering who can make a claim, the answer is anyone. However, not everyone will receive financial support through a life insurance policy payout.

This is reserved for named beneficiaries. If you haven’t calledanyone, the money will go to your next of kin.

Are all kinds of deaths accepted for the death benefit?

Generally speaking, no matter how you die, your beneficiaries should be able to claim your life insurance. There’s one exception, and that is suicide.

Suppose the person who got the insurance commits suicide within 12 to 24 months after signing the document (the exact period depends on the insurance company). In that case, their beneficiaries will most likely not be able to receive the death benefit.

Are there any other situations in which the payout can be declined?

Aside from suicide, the death benefit can be declined for several other reasons – non-disclosure (you lied about something during your life insurance application process), not paying premiums that cause insurance to expire, or natural death during the waiting period, being one of them.

How to Get the Best Term Life Insurance Offer

Once you decide to buy term life insurance, you might wonder how you can get it at the best price. The answer is to compare term life insurance quotes.

There is honestly no other way – if you want to know who has the best policy, you need to compare those from a few different providers. Thankfully, we’re here to help you get the best life insurance quote.

What We Offer

Our site makes comparing term life cover quotes and coverage levels quick and easy. We scour the hundreds of insurance companies in the market and compare their term life policies to find the best deal based on your coverage needs.

This saves you a lot of time because you don’t need to shop around on individual provider sites.

You will find the best term life coverage by providing a small amount of information and letting us do what we do best.

Enrolling is easy, and within a short time, you will have a term life policy that meets the financial needs of your beneficiaries. With financial considerations made for surviving loved ones, you can get back to enjoying life.