Vitality Life Insurance Review – Should You Buy?

Vitality Life takes a more active role than most insurance providers do by helping people to live active and healthy lifestyles.

Choosing the right life insurance can be daunting, so our comprehensive Vitality Life Insurance review is here to guide you.

In this review, we explore the features, benefits, and potential drawbacks of Vitality Life Insurance to help you make an informed decision about your coverage.

Who Is Vitality Life’s Target Customer?

Those who find the cover offered beneficial would benefit from the extra perks included, as the more healthy activities you engage in, the more you’re rewarded with a discount on your premiums.

Vitality Life Insurance Reviews. Some Positives Worth Thinking About:

- Compared with the competition, they have fewer exclusions.

- Defaqto 5-star rated cover from only £8 per month.

- Premiums for younger men and women are consistently better than those of many other insurers

- Carry sound testimonials for customer care

- Feature exceptional deals for joint cover

- Better rates are obtainable for smokers and vapers.

See How Vitality’s Plans Compare Against Other Leading Life Insurance Companies – Quick Quote Form

Vitality Life Insurance Summary:

| Product | Description |

|---|---|

| Life Insurance | Lump sum to loved ones upon death or terminal illness. |

| Income Protection | Monthly income if sick or injured and can’t work. |

| Serious Illness Cover | Covers between five and 70 years, a lump sum if you pass away within the term. |

| Mortgage Protection | Pays off the mortgage if you are terminally ill or pass away. |

| Term Life Insurance | Covers between five and 70 years, lump sum if you pass away within the term. |

| Whole Of Life Insurance | Lasts the whole life, a guaranteed lump sum to the family upon death. |

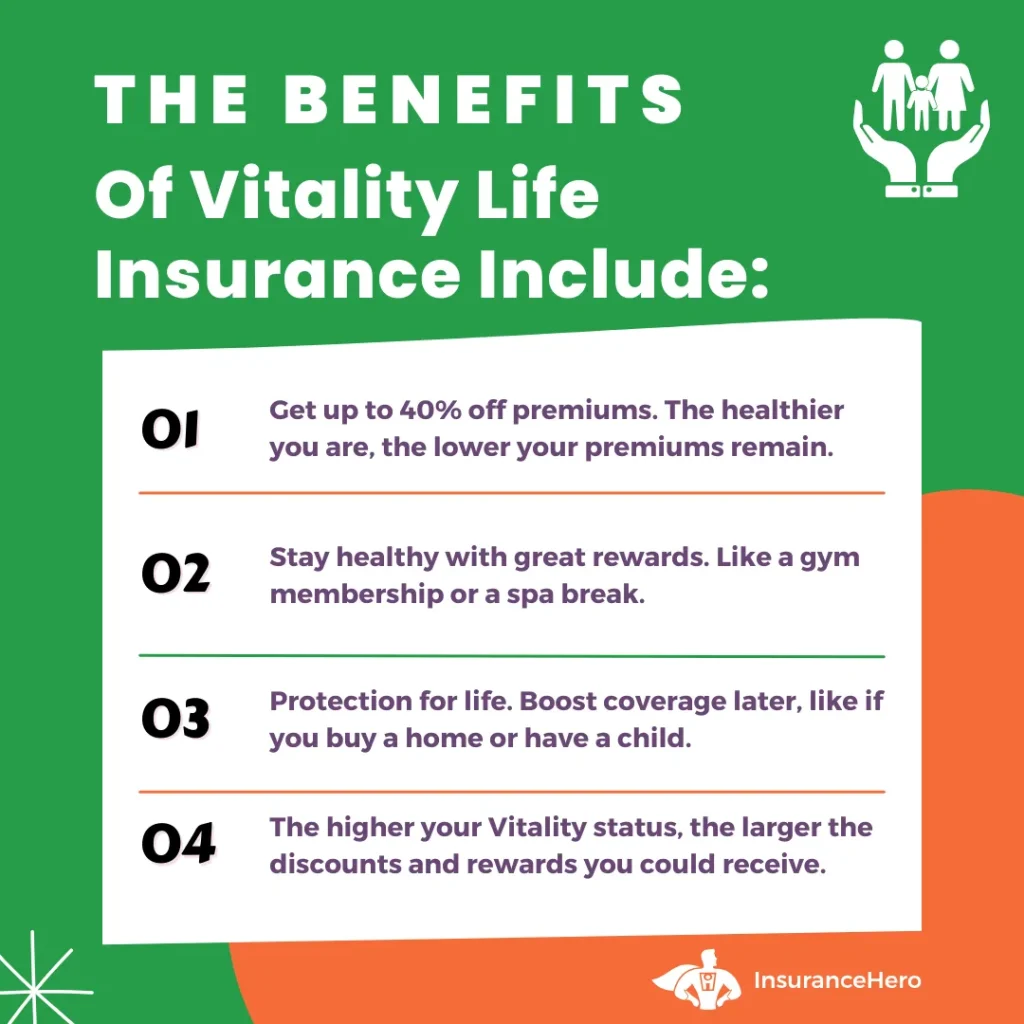

| Additional Benefits | Up to 40% off premiums, gym memberships, spa breaks, earn up to 2 months of premiums back, etc. |

How can a Vitality policy be purchased?

Purchasing a Vitality policy is a straightforward process that can provide valuable protection for you and your loved ones.

To acquire a Vitality policy, you can follow these steps:

- Research: Begin by researching the different types of policies offered by Vitality. They offer a range of options, including life insurance, critical illness coverage, and income protection. Determine which policy suits your needs and financial situation.

- Evaluate the Benefits: Consider the benefits and advantages of a Vitality policy. Vitality is known for its extensive range of rewards for active customers, including free items, discounts, and more. Additionally, their life cover is considered one of the most comprehensive in the UK. Assess these benefits and determine if they align with your requirements.

- Compare Quotes: To ensure you get the best coverage at the most competitive price, it’s wise to compare Vitality’s life insurance quotes. Contact our friendly team of experts who specialise in Vitality policies. They can guide you through the process, provide personalised recommendations, and help you obtain multiple quotes.

- Get in Touch: After carefully evaluating the options and comparing quotes, please contact our team of experts. They will be available to answer any questions and help you understand the terms and conditions of a Vitality policy. They can also assist in completing the necessary paperwork.

- Purchase: After finalising your decision and understanding the terms, it’s time to purchase your Vitality policy. The Insurance Hero team will guide you through the process and ensure that all required information is provided accurately. They will also help you choose the appropriate coverage amount and any additional options you may need.

Following these steps, you can easily purchase a Vitality policy that offers essential protection for your family, mortgage, or other financial needs. Remember, our team is here to support you throughout the process and ensure a seamless experience.

Household name online review companies indicate positive customer feedback with Vitality Life Insurance:

| Review Platform | Review Quality And Number |

|---|---|

| Trustpilot | 48,401 Reviews With An Overall Rating Of “Excellent”. |

| SmartMoneyPeople | A Score Of 4.17 Out Of 5. Based on 24 Reviews. |

| Fairer Finance | A claims score of 97.05% and an overall rating of 80.67% |

| Defaqto | Rated 5 out of 5 stars on this popular platform, showing this insurer has a high satisfaction score. |

Some Background History

They’ve been around for a long time, long before they sprang up in 2014. Before that, it was a partnership between Prudential and Discovery trading under the name PruProtect since the insurance company launched in 2007.

In 2015, Discovery took ownership and relaunched as Vitality Life, paying out 99% of life insurance claims and achieving a 93% success rate for claims submitted for serious illnesses in 2024.

From then on, all Vitality Life reviews were based solely on Discovery’s ownership, without collaboration with Prudential.

Points Reward Scheme

Every customer gets free access to this. It offers access to its exclusive cashback scheme with select partners. The partners are companies with products and services to help you live healthier.

Examples include 50% cashback when you buy a bike at Evans Cycles, or if you have a Virgin Active Health Club near you, you can use it for half the price.

You don’t need to buy fitness gear, such as half-price fitness wearables, to benefit from the scheme.

This is open to all customers; all that is required is an activity tracker to track your activity. The example they give for their points scheme is earning 12 points by taking 12,500 steps daily twice a week.

That may sound like a challenge, but it won’t be for some, considering the recommended number of steps per day is 10,000, equivalent to walking for 5 miles.

Complete 25,000 steps in a week, and you’ll be rewarded with a relaxing drink at Starbucks and a ticket to a Cineworld or Vue cinema for any screening that takes your fancy.

To help you earn your points to get your rewards, they will also keep you motivated by boosting your rewards as you progress from a Bronze level to Silver to Gold to reach Platinum status once you’ve earned 2,400 points.

The more healthy activities you do, the more points you rack up. Even just starting, you can boost your rewards to silver status by taking an online health review and a Vitality Health check.

Suppose you are active or at least interested in becoming active. This life insurance provider supports customers in leading healthy and active lifestyles.

Add-Ons that Work to Bring Your Premiums Down

There are options to add to the Wellness Optimiser for £4.50 per month and the Vitality Optimiser for £3.30 per month.

Both options get you better rewards and discounts, including an instant monthly premium discount.

It’s not a fitness cult you’re joining, though!

At this stage, you’d be forgiven for thinking it’s a membership to an exclusive healthy-living group. First and foremost, Vitality Life Insurance is an insurer.

They do things a little differently, wanting to be in the business of life by protecting it. That’s why there are some neat little extras in there.

The cover must be right, as they are primarily insurers. Life insurance is an investment in your family’s future, not necessarily the policyholder’s.

The Vitality Life Healthy Living Benefit Scheme supports your efforts to be around your family for as long as possible.

What are the qualifications to qualify for the Apple Watch promotion?

To qualify for the Apple Watch promotion, the following conditions must be met:

- Possession of a Vitality policy: You must have an active Vitality insurance policy.

- Minimum monthly premium: Your monthly premium for the Vitality policy must be £49.75 or higher.

- One watch per plan: Only one Apple Watch can be obtained per insurance plan. If you have a joint policy, you cannot receive two watches.

- Flexible purchase time: Purchasing the Apple Watch immediately upon policy activation is unnecessary. You can buy it at any point during your policy term.

- Activity-based pricing: The cost of the watch is determined by your level of physical activity. The more active you are, the lower the cost.

- Earning vitality points: To minimise the cost of the watch, you must earn at least 160 vitality points each month.

- Watch payment range: Depending on your monthly activity level, you can pay anywhere from £0 to £9.50 for the Apple Watch, with the cost decreasing as your activity level increases.

The Plans Vitality Life Offer

- The Lifestyle Care Cover

This plan protects your lifestyle. If your concern is being unable to care for yourself in later life, this cover is likely to be of interest.

- The Mortgage Life Insurance

As it sounds, this option is only suitable for those with a mortgage and protects your payments in the event of either death or a diagnosis of a defined critical illness.

However, for the critical illness to be covered, it must meet the policy’s criteria. The fine print will be essential reading before signing the document (more on that later).

- The VitalityLife Plan – Premiums starting at £5 per month

This is a level-term policy that will pay out a fixed lump sum to your family in the event of your death. Serious illness cover can be added, providing protection should you become seriously ill and unable to perform your job.

The VitalityLife plan provides immediate cover, so your life insurance starts immediately rather than waiting 28 days or until any part of your policy begins.

You get instant cover, so immediate peace of mind.

The maximum coverage is £20,000,000.

- The Essentials Plan – Premiums begin at £8 per month

This is very similar to the VitalityLife plan, except that it excludes immediate cover and a few other extras.

The maximum coverage is the same as that of the VitalityLife plan, at £20,000,000.

- Serious Illness Cover

This can be added to both plans to provide additional protection should you be diagnosed with a serious illness. Perhaps something that strikes, such as a heart attack, leaves you unable to work. It’s not coverage based on you being diagnosed with a life-threatening illness, but rather financial protection against a loss of income due to an illness preventing you from working.

- Terminal Illness Cover

Unlike serious illness cover, terminal illness cover is less beneficial because it requires stringent criteria for a successful claim. A terminal illness must be diagnosed to be eligible, resulting in you having less than 12 months to live. Additionally, you must have more than a year remaining on your policy.

The Types of Life Insurance Vitality Life Offers

- Level term

The amount of coverage you take out at the start of your policy won’t change.

- Indexed

Index cover protects against inflation. Your policy’s payout amount ensures that your beneficiaries will receive an annual increase on the policy anniversary.

- Decreasing term

On a decreasing term plan, your payout decreases each year. It’s generally used as a mortgage insurance product. The more you pay towards your home, the less the outstanding balance will be.

Therefore, a lesser sum would be required to repay the mortgage balance. It’s the most affordable product, with the Essential Plans’ most basic option providing the bare essentials of a life insurance product.

How can I cancel my Vitality life insurance policy?

To cancel your Vitality life insurance policy, you have a few options. Firstly, contact Vitality directly and inform them of your decision to cancel. They will guide you through the necessary steps and provide any additional information.

Alternatively, if you prefer assistance during the cancellation process, our team of friendly experts is here to help. They can guide you through the process, answer any questions, and even help you find a new policy with a provider that better aligns with your needs.

Whether you contact Vitality directly or seek guidance from our experts, we are committed to providing the support you need to cancel your life insurance policy smoothly.

Overall Thoughts

At the outset, you might find it challenging to understand the terms of each Vitality Life plan and add-ons.

They fall short on transparency, but most insurance providers are similar. A lot of jargon is in the fine print, and even talking to company representatives leaves you with more questions than when you asked the first.

The customer experience reports from Fairer Finance, an independent consumer help group, gave Vitality Life a 52% transparency score, which is below the average for most providers.

Of the 28 life insurers listed on Fairer Finances consumer reports data, Vitality Life ranks 22nd. Claims handling and approvals are good, but transparency is their Achilles heel.

They excel at being involved with customers after the sign-up process. Often, a life insurance policy is taken out and never given a second thought.

It’s just a small premium that appears on your bank statement each month for years, or for the rest of your life, on whole-of-life policies, with no correspondence after taking out the policy, other than when changes are being made.

Vitality Life interacts with its customers more than any other insurance provider. It’s not about life insurance, but let’s face it: Would you look forward to a monthly e-magazine discussing life insurance?

Neither do they, and it’s probably why they don’t. They focus on helping their customers live healthier, longer.

They have an active user group of fitness enthusiasts. They publish and send you their e-magazine, which includes success stories, motivational columns, and a push to inspire and keep you on track with healthy living.

All the rewards partners are focused on healthy living, so if that’s not interesting to you, you won’t find Vitality Life any different from the rest, as you’ll likely disregard them as another insurance provider—a company you pay monthly for something you’ll never see.

For those trying to live a healthy lifestyle and finding it comes at a cost in gym fees and gadgets, and you’re looking to get life insurance or perhaps switch to a provider that supports your efforts, Vitality Life is worth a closer look.

Remember to scrutinise those terms and conditions and all-important policy documents to ensure you understand what they mean, as that’s the only genuine concern with Vitality Life.

While they excel in helping their customers lead healthy lives, they fall short in their use of industry jargon.

Want to find out how Vitality Life stacks up against the most suitable insurance providers for your current lifestyle?

At Insurance Hero, our primary role is to provide life insurance quotes that meet customers’ needs and deliver excellent value at the lowest possible price.

We search, compare, and analyse the policies from over 300 insurance providers, returning only the most suitable providers and policies that meet your needs and budget.

On your shortlist of suitable providers, Insurance Hero and Vitality Life, so you can see firsthand how their policies and price points compare to those of their competitors.

There is no cost to you and no obligation, either. It’s just an expert hand matching you with the right provider, policy, and price.

The best life insurance UK plans can be within your reach. We also hope you have found our Vitality Life Insurance review helpful and look forward to helping you secure the best policy for your unique needs.

When my children get to a certain age, I plan to get divorced – how does this affect my life coverage needs?

Even though a joint life insurance policy can be more cost-effective, getting a single policy could be wise. Or you could think about life insurance for dads or life insurance for new mums.

Further Information:

Head Office: Vitality, 4th Floor, 70 Gracechurch Street, London EC3V 0XL.

VitalityLife Customer Services, Sheffield S95 1BW

Telephone: 0808 256 6753

Website: https://www.vitality.co.uk/life-insurance/

E-Mail: lifecustomerservices@vitality.co.uk

AA Life Insurance UK Cover Review

Various life insurance products are available, including level term, decreasing term, and 50-plus. AA life insu…

AEGON Life Insurance Reviews – Compare Quotes

If you want to provide financially for surviving loved ones upon death, AEGON life coverage may be the solution. …

AIG Life Insurance UK Reviews

AIG (American International Group) is synonymous with the insurance industry. AIG is a multinational insurer fo…

ASDA Life Insurance Cover Reviews

ASDA Financial Services offers travel, home, motorist, pet, life insurance, personal loans, trade, gift, and credit card…

Aviva Life Insurance Review – Cover From £5 Per Month

Aviva is the largest UK insurance services provider and the fifth largest insurance group, with more than 45 million cus…

Axa Life Insurance Cover Review

The AXA Group has been in the insurance business since the 18th century. Acquisitions, mergers, and name changes for lea…

Barclays Life Insurance Review

Barclays PLC is a major financial services company backed by more than 300 years of history. Welcome to our new…

British Seniors Over 50 Life Insurance Reviews

Find out about British Seniors Over 50 Life Insurance Reviews, Customer Experience, and Policies Available. Abou…

Direct Line Life Insurance For Over 50’s Review

Direct Line is a household name for insurance products. At the outset, their core offering was vehicle insurance with a …

Ageas Protect Life Insurance Review

Fortis Life is now Ageas Protect, the financial protection arm of Ageas within the UK. The company offers produ…

Friends Life Life Insurance Reviews

Since 1810, Friends Life has been providing financial services. Founded in Yorkshire as Friends Provident in 1832, the c…

LV Life Insurance Reviews

In 2007, Liverpool Victoria rebranded their company name to use LV=. The LV= brand is a visual play on the word…

Nationwide Life Insurance Reviews And Cover

Nationwide Building Society offers insurance, banking, investment, loan, credit card, and mortgage services to residents…

NatWest Life Insurance Review From £5.46 Per Month

Welcome to our newly updated 2026 Natwest life insurance reviews page National Provincial Bank was established i…

One Family Over 50s Life Insurance Reviews

One Family over 50s life insurance offers UK residents aged 50 to 80 a straightforward way to take out life insurance co…

Post Office Life Insurance Review

Welcome to our Post Office life insurance review. In the United States, the Post Office is where residents mail letters …

Prudential Life Insurance UK Reviews

The international financial services group Prudential plc serves over 25 million customers and manages approximately £3…

Royal London Life Insurance Reviews

Royal London is the largest mutual life and pensions company in the UK. It comprises several specialist businesses desig…

Scottish Provident Life Insurance Review

Scottish Mutual Assurance Limited provides healthcare and protection products under the brand name Scottish Provident. …

Scottish Widows Life Insurance Reviews

Scottish Widows is a nationally recognised financial services provider that has served families with financial protectio…

Shepherds Friendly Over 50s Life Insurance Review

The Shepherds Friendly Society is one of the longest-running insurers in the world. In 1826, they began by establishi…

Smart Life Insurance Reviews, What Buyers Should Know

Welcome to our newly updated Smart Life Insurance reviews guide. Smart Life Insurance offers people a range of flexible,…

The Exeter Life Insurance Reviews

Do you have pre-existing medical conditions? Do you want to put in place a robust life insurance policy that will provid…

Virgin Money Life Insurance Review

Virgin Life Insurance is one of the over 400 companies in Virgin Group Limited, the British-branded venture capital cong…

Zurich Life Insurance Reviews

Zurich Financial Services Group, commonly referred to as Zurich, was founded in 1872. Headquartered in Zurich, …

Saga Life Insurance Over 50 Reviews

Welcome to our Saga Life Insurance Over 50 Reviews. Many people over 50 are concerned about choosing the right life insu…

HSBC Life Insurance Review

Life insurance is an important financial product that can help provide financial security to your loved ones in the even…

Lloyds Bank Life Insurance Review

“Lloyds Bank is likely at the forefront of your search if you’re in the market for life insurance. But how does this maj…