Income Protection Insurance For Dentists

Are you a self-employed or an NHS dentist? Do you worry about what would happen financially to you and your loved ones should you be unable to work?

Dentists’ Income Protection Cover Summary:

In return for a regular monthly payment, income protection for dentists pays a replacement monthly wage if you are unable to work due to an accident, injury, or illness. It will protect you until you can return to the workplace.

Here’s why it’s worth considering:

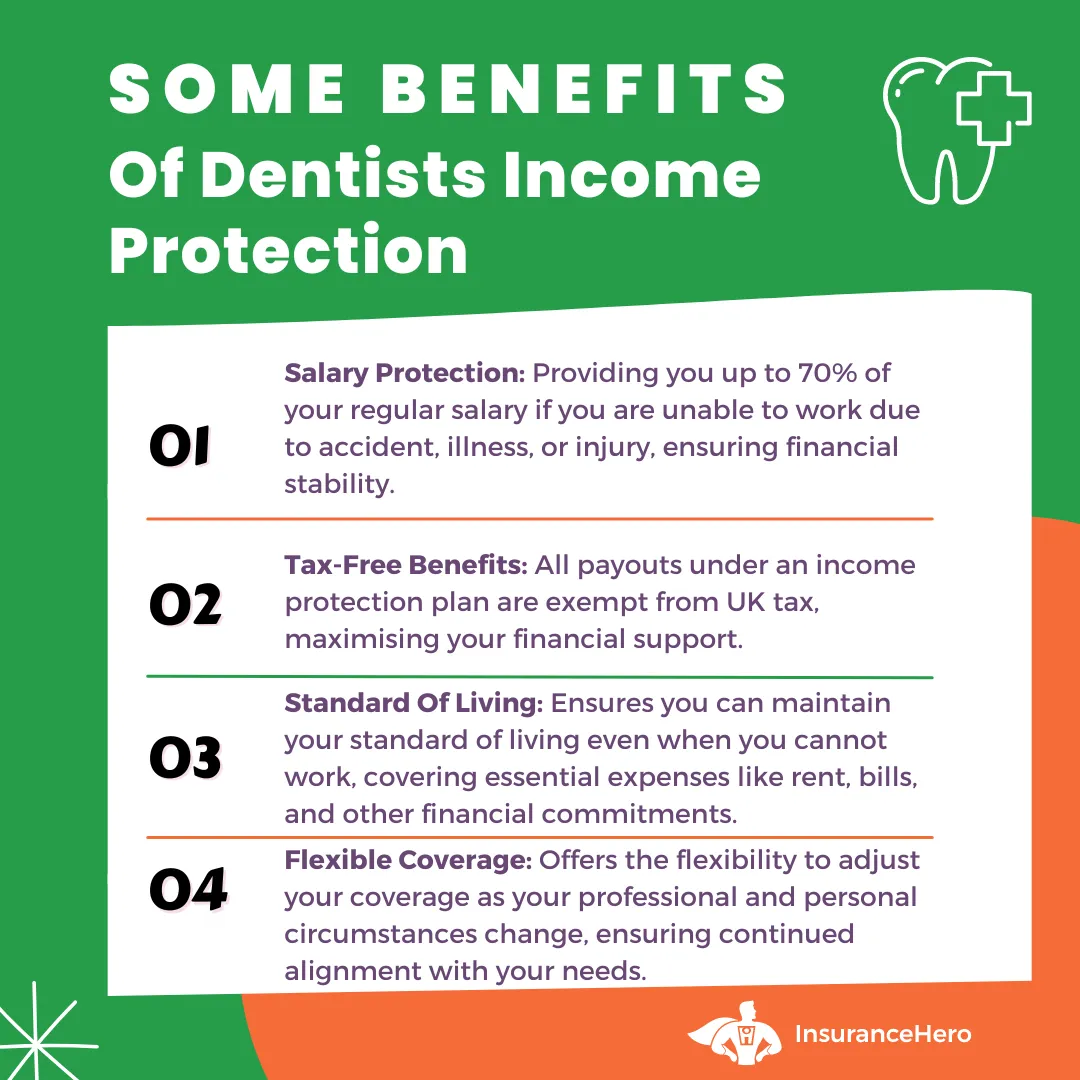

- Depending on the length of the claims period, you can continue to receive payments until you return to the workplace, retire or die.

- You can insure up to a level of between 60% and 70% of your gross salary if you are an employee (or 60% to 70% of net profit for the self-employed).

- Your standard of living stays the same even if you are not able to work.

- Income insurance can be flexible and changed to suit your evolving personal and professional situation.

Get Income Protection Quotes From The UK’s Top Companies

Why do Dentists need Income Protection?

As with many other professions, dental practitioners may be unable to work for sustained periods due to industry-specific injuries.

Dentists are more likely to develop musculoskeletal disorders. Research undertaken by Brown et al. in 2010 focused on why dentists retire due to poor health.

Musculoskeletal disorders are the reason cited by 55% of dental professionals surveyed.

Regarding specific injuries, a study by the PMC of work-related musculoskeletal disorders in dentistry practitioners found the most common injuries suffered include:

- Neck and shoulder pain – caused by an unnatural head position when attending to patients

- Back pain – Injury caused by improper posture and repetitive strain

- Hand pain – caused by repetitive stress, such as hand pressure when scaling and polishing

High stress is another factor affecting dentists. There is evidence that the profession is associated with a high level of job stress caused by the heavy workload from running behind schedule and dealing with anxious patients.

What Is Covered Under Income Protection?

Income protection pays out if you are unable to work due to illness or an accident.

Being unable to do your job is defined differently by different underwriters, but can include any of the following:

- Inability to undertake any type of paid employment

- Failure to carry out your actual job

- Failure to do your job or one that you are similarly qualified to do

Dentist sickness insurance that provides cover if you cannot do your actual job will always be the most expensive coverage, unlike being unable to do any job.

Specific policies will result in a proportionate payment. It will top up earnings if you return to full-time employment, even if in a lower-paid job.

Not Covered

Most policies do not payout as long as you receive a full salary, and all plans limit the claim amount to ensure that you do not make a profit.

Insurers will not pay out if you cannot work due to any of the following:

- Existing medical issues that you had before taking out protection. These are also known as pre-existing medical conditions

- Inability to do your job due to drug or alcohol abuse

- Participation in extreme sports or activities that did not form part of the list at the policy’s outset

- Childbirth and pregnancy

Additional features that provide Further Cover

Further income protection features, both standard and optional, that you and your broker or advisers should be aware of include the following list:

- Childcare benefits

This feature will pay a set amount for each of your children when you are not working. It helps with further childcare costs you may face if not working, including a live-in nanny or additional child-minder requirements.

- Specified trauma or injury benefits

You are entitled to an additional payout if you get a specific illness or injury listed on your policy under this inclusion. It is typically a regular payment that tops up the standard monthly replacement salary, but can sometimes be paid as a one-off lump sum.

- Death benefits

This option allows your dependents to receive a lump-sum payout if you die while receiving income protection benefits. It should be noted that if an accident or injury proved fatal at the time, a payout might not be due.

- Pausing or freezing your policy

Policies cannot pay out a portion of your salary if you are not working when an incident happens. In the event of unemployment, it is often possible to freeze your plan until you return to employment.

- Involuntary Redundancy

It is often possible to include an additional option in an income protection policy to cover involuntary dismissal. You can discuss the policy terms with your adviser when deciding.

- The Claims Process

You have made the right choice by having an income protection plan in place, but what is the claim process if you suddenly find you cannot keep working?

An example real-world policy:

| Policy Feature | Example Details |

|---|---|

| Policyholder age | 37 year old male |

| Smoker status | Non-smoker |

| Monthly benefit insured | £1,750 |

| Deferred period | 12 weeks |

| Policy end age | 60 years |

| Cover type | Full-term (it pays until recovery or the age of 60) |

| Premium type | Guaranteed |

| Aviva | £39.80 per month |

| Zurich | £47.25 per month |

| AIG | £52.10 per month |

| Effect of shorter deferral (8 weeks) | Approx. £46.90 per month |

| Effect of longer deferral (26 weeks) | Approx. £31.40 per month |

| Typical loadings (if applicable) | Impact of longer deferral (26 weeks) |

| Optional features added | Own-occupation cover, indexation (3% p.a.) |

Is Income Protection Appropriate for Your Situation?

Whether you are single or have a family with children, your immediate thoughts should be: If you are unable to do your job due to illness, can you pay your bills and other financial commitments?

In deciding whether income protection is appropriate for you, take into consideration:

- Financial Commitments – Do you have substantial mortgage or rent payments, personal loans, car loans, overdrafts, equity release, school fees or household bills? Can you keep paying these if you are not able to work?

- Savings—If you have substantial savings, you may be able to live without a salary for a time. Will your savings last a year or more?

- A Supporting Partner – If your other half works and can sustain the family if you cannot work, then perhaps you can afford to maintain your typical day-to-day living

Depending on whether you are self-employed in private practice or a dentist working for the National Health Service, there are additional considerations for your situation:

Income Protection For the Self-Employed Dentist

A self-employed dental practitioner working at a practice but not as an owner should opt for standard insurance protection.

Dental owners who typically own a practice through a limited company may want to consider dentist income protection for company directors.

It differs from standard income protection insurance as it considers dividends and salaries paid through the limited company.

If you are unemployed for a period without insurance coverage, your financial fallback is the UK Government’s sickness benefit. It is less than £100 per week and is payable for a maximum of 28 weeks.

It is not an option for many who want to maintain a fraction of a lifestyle.

Income Protection For the NHS Dentist

NHS dental employees benefit from better salary protection from their employer if they are unable to work.

Depending on the length of service, an employee with more than five years of service would expect to receive 12 months of sick pay; full pay for the first 6 months and half pay for the final 6 months.

This means that income protection for dentists can be offset against the employer’s sick pay period.

Effectively, the deferred period in the insurance coverage could start a year after the application for a benefit. It helps reduce the plan’s monthly payment cost.

How Can Insurance Hero Help?

Insurance Hero is a broker and expert at providing plans for self-employed dentists in private practices and the public sector.

We have relationships with an extensive network of underwriters. What sets us apart, though, is our thorough fact-finding process.

We understand the dental profession and will work with you to create a tailored package aligned with your professional and personal needs.

Contact Insurance Hero, which specialises in delivering competitive, tailored quotes to the dental industry. Call our professional and friendly team of brokers today on 0203 129 88 66 for a no-obligation quote.

The key elements – What you need to know

Many features, both standard and optional, can be tailored to your current or anticipated situation. You should be aware of these before you enter discussions or take out insurance.

- Flexible Cover

Before you take out insurance, you can decide how long before a payout occurs, should you not be able to work or when you want your replacement salary payments to begin.

- Variable or fixed benefits

Depending on your professional and personal circumstances, you can choose whether to increase, decrease, or keep your payments on hold.

- The Deferred Period

When setting up your insurance, you will conduct a thorough fact-finding exercise with your insurer. It will advise you on tailoring everything to your personal and professional needs.

One area that needs to be adapted is the deferred period.

It is the gap between when you make a claim and when the replacement salary kicks in. If you are not self-employed, it can vary from the next day to one year and be tied to match your employer’s sickness terms and conditions.

- The Sum Assured

The sum assured is the salary you would receive should you submit a qualifying application for benefits due to injuries or illness.

Policies will typically not exceed 60% to 70% of your previous wage to encourage a return to the workplace. It is up to you to select how much of your salary you want to pay. The higher the salary to be covered, the higher the cost.

- The Cease Age

It is merely the age you will be at the time the plan matures. It is standard practice to align this with your retirement date. The longer you wait to retire, the higher the premiums will be.

- The Length of Claims Period

When you take out insurance, you need to decide whether you want it for a shorter duration of up to 5 years or a longer duration that will protect you until retirement.

Short-term cover limits the payout duration. Popular protection durations range from one to five years, and there is usually a cap.

Long-term cover: This protection is more expensive on a monthly basis but will provide you with a monthly salary until you can return to paid employment or until retirement if you can never work in a dental practice again.

Like most other professionals, Insurance Hero recommends a long-term policy. Statistics from the UK indicate that the average claim length is over seven years, significantly longer than the five-year cap on short-term protection. Cheaper is not always better.

Understanding Indexation and Premiums

Indexation is the option to tie your protection plan to movements in the Consumer Price Index (CPI), a measure of inflation used by the UK government.

There are three types of cover associated with indexation:

- Increasing

The premium level and the subsequent replacement salary will increase in regular increments, tracking movements in the consumer price index. This type of cover is also known as Index-Linked Cover.

- Level

With level cover, the premium and subsequent replacement salary will stay the same throughout the plan duration.

- Decreasing

This type of protection is typically associated with an expected reduction in outgoings, such as mortgage payments.

A premium is a monthly payment made throughout the fixed-term duration of the cover, and it is calculated by an underwriter.

There are three options for the ongoing premium, which you pay every month:

- Age-banded

It works to increase the monthly payment amount due as the policyholder gets older and a higher associated risk of older people going on to make an income protection request for benefit.

Age-banded premiums are typically cheaper at the outset and increase incrementally over time.

- Guaranteed

The underwriter cannot change the monthly payment due throughout the duration of the plan. This is guaranteed unless the policyholder makes changes to the policy.

Guaranteed premiums can be a cost-effective option over the policy’s term, particularly if taken out when the policyholder is young with no underlying medical conditions.

- Reviewable

A reviewable premium means the underwriter can review the level of protection at any time. This might be due to unforeseen circumstances that have increased claims.

It allows the underwriter to adjust the monthly payment amount. Despite starting at a better value over a policy’s lifetime, a reviewable option tends to be more expensive due to periodic upward revisions.

How to make a claim

- Contact your insurance broker by phone, email, or correspondence and request an application form.

Required Information

- Return the completed form together with the requested information, which will typically be:

- A GP or Specialist medical report of your condition

- Financial information, including payslips and P60 for employees and tax returns and accounts for the self-employed, including limited companies

How A Claim is Assessed

- Your insurer will review whether your current circumstances meet the policy definitions

- The payable benefit is typically tied to your salary when you were working, and the maximum payable amount is in the policy documentation. It may be lower if your salary falls once a policy is in place

- You must keep paying your premiums until your insurer contacts you

Once a claim has been accepted

- Your insurer will confirm payment details and when you should expect payment

- The benefit application is periodically reviewed while you are not working

Call today for an income protection quote and your coverage options. Our friendly team of brokers only provides watertight protection products so you can receive income when you need it. Phone Insurance Hero, your professional dental insurance company, on 0203 129 88 66

FAQs

Can any dental professional apply for income protection?

Any dentistry practitioner can apply for cover, irrespective of whether you operate as self-employed in private or public practice.

The criteria for applying for plans are:

- You are aged 16 or over

- Not older than 63 when completing an application form

- You have a UK Building Society or Bank account

- You have a registration with a UK medical practice for at least three years

- Are currently subject to the payment of UK income tax

As a dentist, how much will it cost me?

Numerous factors will affect the monthly payment you will make. These include, but are not limited to, the following:

- Will you be taking out short-term or long-term cover?

- How long do you want the length of the claim period to be?

- How old are you, and do you have any underlying medical conditions?

- What percentage of your salary do you want to include under the policy?

- Do you want indexation in your policy?

- Do you want the policy to cover an inability to do your specific job or to include any job?

How much of my income is covered?

For both a self-employed and an employed dentist, the maximum coverage is 70% of your regular gross income.

You can choose a lower than 70% LTV to keep your monthly payment down.

A coverage cap may encourage claimants to return to the workplace, which may be more challenging if the salary is paid at 100% of the insurance coverage when they are unable to keep working.

It should not put you in a better financial situation than if you had never made a claim and were working.

Can I receive other claim money besides my income protection dentist plan?

This is fine if the total income received from different sources does not exceed 75% of your pre-claim income.

You will be unable to receive more than 75% of your monthly income, such as other injury or sickness benefits from other claim sources.

Can I make policy changes once I take out insurance cover?

Personal and professional needs tend to change. Salaries may increase, more children may become part of the household, or a mortgage may be repaid—the list is endless.

It is common sense that you can increase or decrease the level of your income protection to match your changing circumstances.

Income Protection Insurance For Doctors

Income protection insurance for doctors plans work by providing a replacement salary if you cannot do your work due to a…

Joint Income Protection Insurance For Dual Income Couples

If you’re in a similar situation to 25% of couples with a dual income, you’ll never have even contemplated Income Pr…

Can You Get Group Income Protection Insurance?

Are you worried about how you’ll cope financially if illness or injury stops you working? In 2024 alone, insurer…

Self-Employed Income Protection Insurance

Working as self-employed can be immensely rewarding if a business becomes successful and, with no employer or boss to re…

Income Protection Insurance For Vets

Being a vet can be a challenging yet immensely satisfying profession. Accidents and injuries can occur in the workpl…

Income Protection Insurance For Contractors

Do you worry about how you will pay the bills if you cannot work? Do you have loved ones who would suffer from financial…

How Much Does Income Protection Insurance Cost?

While most people aim for the maximum amount of cover for the minimum cost, the actual cost of income protection insuran…

Income Protection Insurance For Teachers Guide

Receive a monthly income for as long as you need if you are off work sick or physically injured – it is that simple. …

Does UK Income Protection Insurance Cover Maternity Costs?

If you’ve just learned that your family is about to grow, there’s a good chance you’re filled with both tremendous…

Does Income Protection Cover Redundancy?

When times are tough, when the economy turns downward, or when corporate profits demand a reduction in expenses, employe…

What Is Accident Sickness And Unemployment Insurance (ASU)?

When it comes to safeguarding your family and your future, two major transition points matter. The first is any …

External resources:

Steve Case is a seasoned professional in the UK financial services industry, with over twenty years of experience. At Insurance Hero, Steve is known for simplifying complex insurance topics, making them accessible to a broad audience. His focus on clear, practical advice and customer service excellence has established him as a respected leader in the field.