How Life Insurance Premium Is Calculated?

Taking out a life insurance policy is one of the best ways to give your loved ones financial stability and assist them in the event of your death.

However, before they can receive the payout, you must first put some resources into your policy. For that, you need an agreement with your insurer.

Once everything is set, you can start financing your policy. On the other hand, if you already have a life insurance policy, you may wonder why the costs are prone to change.

If you want to learn how life insurance premiums are calculated, read on. You may find insightful information that may even help you reduce your premium costs.

Protect Your Loved Ones With Life Insurance. Highly Rated For Financial Strength. Quick Quote

What Is Life Insurance Premium?

A life insurance premium is the amount of money you pay for your life insurance policy, usually every month.

If you continue making these payments, your life cover will remain in place. It should pay out in the event of your death – that’s when your beneficiaries need to make a claim.

Your cover could lapse if you miss a payment. As a result, you could be without life insurance, at least for some time. Also, you might need to take out a new policy to restore your cover, often at a less favourable rate.

How Are Life Insurance Premiums Calculated?

There is no universal formula for calculating premium amounts. However, underwriters use statistical analysis and mathematical equations to calculate a fair score.

Since a universal life insurance calculator does not exist, insurers use different methodologies to calculate premiums.

This means that different companies may offer the same policy type at various prices, so it’s best to compare quotes and take your time finding the best deals.

Nevertheless, insurers consider several personal and policy-related factors to calculate your premiums. Read on to find out what they are.

Personal Factors That Affect Life Insurance Premiums

Listed below are personal factors that influence how life insurance premiums are calculated:

Age

Simply put, the more likely the company is to pay out on your policy, the higher your premiums will be. Age is one of the most significant risk factors for insurers, meaning the younger you are, the lower the life insurance premiums you’ll have to pay.

Nevertheless, you can qualify for a policy even later in your life. For people aged 50 and above, over 50s life cover is the best solution.

This type of policy will cover them for the rest of their lives. Still, insurers may calculate premiums based on significant lifestyle factors, such as smoking.

Smoking and Substance Use

Age and, by extension, life expectancy are some of the most important factors considered when calculating life insurance premiums. Your insurer will also consider other factors that can directly influence your longevity.

Smoking is known to be a common reason behind shorter life expectancy. Researchers agree it increases the risk of contracting critical illnesses like lung or throat cancer.

You can expect a higher insurance premium if you’re a smoker. Sometimes, the difference between life insurance premiums for smokers and non-smokers can be twice as large.

Similarly, frequent alcohol consumption and the use of recreational drugs are considered to pose a risk to your health and lead to a shorter life expectancy. As such, they’re very likely to result in you paying higher premiums.

Occupation

Some careers are considered higher-risk than others, and people in these jobs are usually charged a higher monthly premium.

Such occupations include:

- Military positions

- Police officers

- Prison officers

- Firefighters

- Fishermen

- Offshore workers

Family Medical History

Your premiums will be more expensive if you have any existing health conditions or have had any serious illnesses in the past. Similarly, your insurer would like to know whether there are hereditary conditions or other serious health issues in your family’s medical history.

Certain medical conditions increase the risk of death and, therefore, pose a higher risk to the insurer. However, if you prove that you have fully recovered from an illness or are effectively managing a chronic health condition, your insurer may agree to lower premiums.

BMI

Insurers also consider BMI, or the Body Mass Index, when calculating premiums. BMI is used to determine whether you’re at a healthy weight.

Being underweight or overweight poses some risks to your health, for example, heart disease, high blood pressure, or type 2 diabetes, which can affect your lifespan. This, in turn, results in higher premiums.

Mental Health and Suicide

When applying for life insurance, your physical and mental well-being are taken into account.

However, documented mental health problems, previous suicide attempts, or instances of self-harm will not prevent you from being accepted for life insurance.

Remember that your potential insurer will consider the time elapsed since the occurrence and the treatment received. Additionally, the treatment (or lack thereof) and the impact of such issues on your life will likely influence the cost of your life insurance premiums.

To receive life insurance coverage, you must provide your company with specific information about your physical and mental health.

However, your insurer may also obtain certain information from your GP. As such, you must be honest and provide them with true statements.

One thing that no longer affects life premiums is gender, thanks to a ruling by the European Court of Justice that became effective in December 2013.

Policy Factors That Affect Insurance Premiums

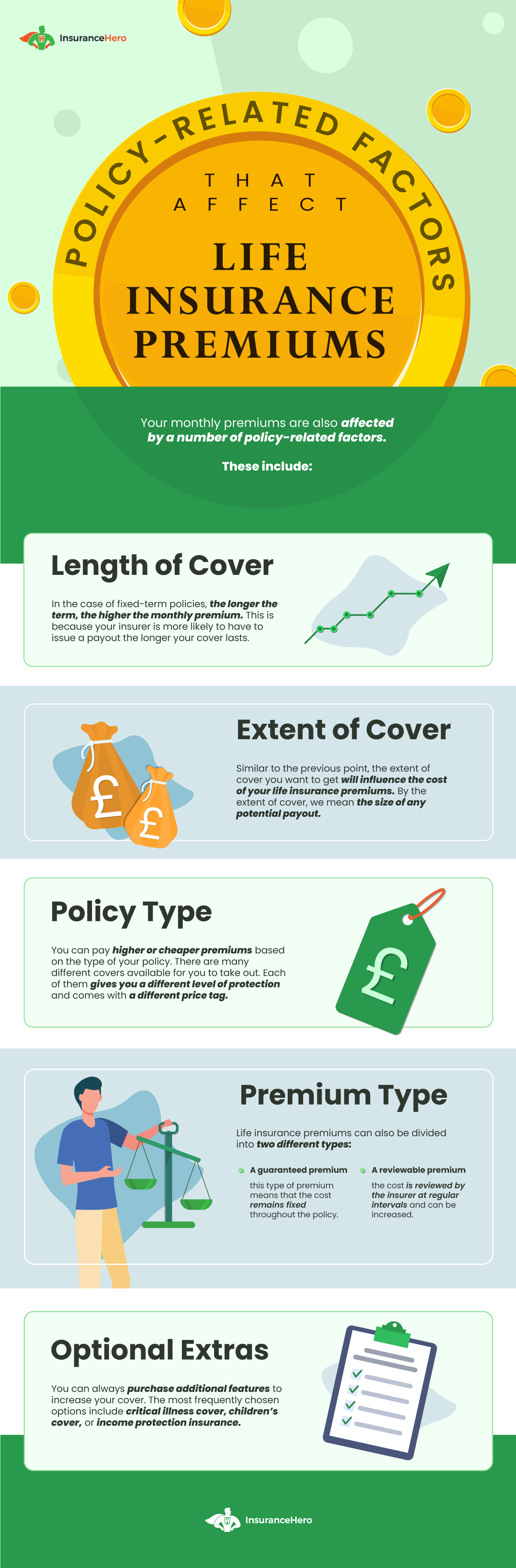

In addition to personal factors, your monthly premiums can be affected by several policy-related factors. These include:

Length of Cover

For fixed-term policies, the longer the term, the higher the monthly premium. This is because your insurer is more likely to have to issue a payout the longer your cover lasts.

When it comes to whole-of-life policies, which cover you until you pass away, you can usually have a set period for fixed life insurance premium rates – typically, it’s 10 years.

Once this period is over, your insurer reserves the right to review your premium. If you have developed any serious medical conditions or suffered any medical issues during this time, you can expect a potential increase in your premiums.

Extent of Cover

Similar to the previous point, the extent of cover you want will influence the cost of your life insurance premiums. By the extent of cover, we mean the size of any potential payout.

Simply put, the more coverage you want, the higher the monthly premium you must pay. The relationship between the premium and the extent of your life insurance policy cover is usually straightforward.

This means a policy for £100,000 will be twice as cheap as a policy that insures you for £200,000.

Policy Type

Your policy type can affect your premiums. Many plans are available, each offering a different level of protection and price.

For example, joint life insurance policies tend to have higher premiums than others. In this case, beneficiaries receive their payout upon the first partner’s death. The risk of a claim is higher, hence the higher costs.

However, the cost is shared between the partners, making joint cover a financially viable option.

When it comes to whole life insurance policies, they often include a guaranteed premium for a specific period (typically 10 years). After that, your premiums are reviewed and can potentially increase.

On the other hand, fixed-term life insurance policies have lower premiums than, for example, whole-of-life cover.

That’s because your insurer is given a set period, such as 25 years (hence the name ‘fixed-term’). In the case of whole-of-life policies, they are required to provide your beneficiaries with a payout in the event of your death, whenever it happens.

This can take longer than any period of time specified in a fixed-term policy.

With so many options available, you need to think about your needs. Maybe you’d benefit more from not one but two life insurance policies?

Don’t make your decision based only on your monthly premiums. Consider the types and levels of coverage that certain life insurance policies can provide, and choose the best option for you and your loved ones.

Premium Type

Life insurance premiums can also be divided into two different types:

- A guaranteed premium means the cost remains fixed throughout the policy.

- A reviewable premium – the cost is reviewed by the insurer at regular intervals and can be increased.

Guaranteed premiums can help you plan your budget, as you know exactly how much you must pay each month. They also give you a clear answer regarding the cost of your life insurance.

On the other hand, reviewable premiums tend to be cheaper at the start of your life insurance policy. However, they can end up being more expensive in the long run.

C

Term Vs. Whole Life

As mentioned above, policy type is one factor that influences life insurance premiums. Term life insurance is less expensive because it covers a stated period, while whole life insurance is permanent (though a whole life policy may include a cash value option).

If the coverage period of a term life policy expires and the policyholder is still alive, no payment is made. Term life insurance is typically used to cover the balance of a mortgage if the individual dies while the policy is in force.

A whole-life policy is considered an investment, and the policyholder can build up cash value by drawing an income. By choosing a whole life policy with a level premium, an individual can make this coverage more affordable.

The premium remains the same for the duration of the policy, while the premium for a term life policy increases over time.

A whole life policy with a level premium is easy to budget for and pays beneficiaries a lump sum when the policyholder dies. Please click here to read our whole vs term life insurance guide.

If you are under 30, decreasing term life insurance is remarkably affordable.

Optional Extras

You can opt for a simple life insurance policy and call it a day. However, you might want to purchase extra features to increase your cover. These extras often come with additional costs.

For example, you might consider getting critical illness coverage, which will pay a lump sum if you contract a serious illness during the policy term. You may also want to add your child to your policy (children’s cover).

Additionally, your premiums will be higher if you choose income protection insurance and other payment protection insurance options. These are not obligatory, so you can expect to pay extra money for such features.

How Many Life Insurance Policies Can I Have In The UK?

You can have as many life insurance policies as you like in the UK, but there are a few things to bear in mind.

- Firstly, each policy will have its own terms and conditions, so make sure you read these carefully before taking out cover.

- Secondly, it’s important to remember that you’ll need to keep up with payments on each policy to keep the cover effective. Missed payments can lead to your policy being cancelled or voided.

- Finally, having multiple life insurance policies may mean you’re not fully covered against all risks, so it’s always worth talking to an expert before taking out additional cover.

Does Life Insurance Cover Funeral Costs?

It’s a fairly common question. Does life insurance cover funeral costs? In short, life insurance does not cover funeral costs. Funeral costs are the responsibility of the deceased person’s family or estate.

However, life insurance can help pay for funeral expenses. The death benefit from a life insurance policy can be used to cover the cost of a funeral and other final expenses, such as outstanding bills and debts.

Summing Up

As you can see, many factors contribute to the final answer for how life insurance premiums are calculated.

Personal circumstances, such as the amount of your life insurance premiums, are affected by several policy-related factors, such as the length and extent of the coverage you want, your policy type, and additional features you may want to add.

With no standard formula to calculate premiums, you must remember that you must take care of factors you can control if you want to qualify for life insurance and have lower premiums.

These include your lifestyle and various policy-related aspects that depend on your needs.

Why Use Insurance Hero?

Insurance Hero partners with reputable insurers to offer you great deals at competitive prices.

Contact us today and let us help you find the best life insurance policy tailored to your needs, or read our useful life insurance guide to get a clearer understanding of the subject.

Steve Case is a seasoned professional in the UK financial services industry, with over twenty years of experience. At Insurance Hero, Steve is known for simplifying complex insurance topics, making them accessible to a broad audience. His focus on clear, practical advice and customer service excellence has established him as a respected leader in the field.