How Many Life Insurance Policies Can I Have?

In the UK, it’s entirely legal and often practical to hold multiple life insurance policies.

A well-known solution is to take out at least one life insurance policy. Many types of life insurance policies are designed to protect various assets.

That’s why you may want to decide that one life insurance policy is not enough and start looking for extra insurance coverage, especially if you happen to reach significant milestones in your life.

Can You Take Out Multiple Life Insurance Policies? Summary:

Whether you’re planning for different financial responsibilities or seeking more comprehensive coverage, having more than one policy can offer flexibility and peace of mind.

Here’s what you need to know:

- You can have more than one life insurance policy. There’s no legal limit on how many life insurance policies you can hold.

- Reasons for holding multiple policies include covering a mortgage, protecting your family’s income, or business-related needs, such as key person protection.

- Insurers assess total risk. They’ll consider your overall cover level and financial justification when you apply for multiple life insurance policies.

- You can mix policy types, such as combining level term, decreasing term, and whole-of-life insurance, depending on your needs.

- Claiming on multiple policies is allowed. Your beneficiaries can receive payouts from all valid policies if you pass away during the coverage term.

Best Life Insurance Companies · Help at Every Stage · Simple Quote Process – 60 Sec Form

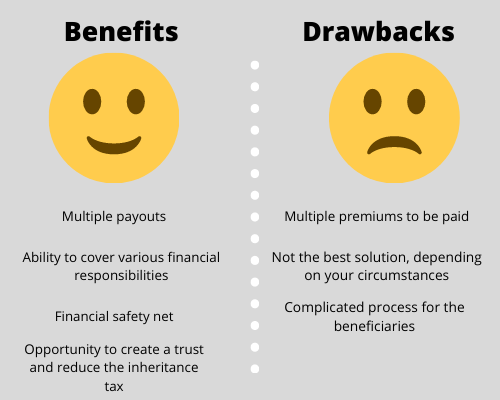

Benefits of Having Multiple Life Insurance Policies

Having multiple life insurance policies has several advantages – the biggest one being the ability to cover various financial responsibilities, such as a spouse, children, mortgage, funeral costs, or tuition fees.

Your beneficiaries will have more financial support if you’re not there to help them, which will undoubtedly ease some of their worries.

If you’re in a relationship and take out two or more life insurance policies, your loved ones will receive two or more payouts. In a joint life insurance policy, both spouses must pass away before the beneficiaries can receive payouts.

Additionally, having multiple life insurance policies rather than just one life insurance policy gives you the option of putting one of them in a trust.

This way, you can reduce the inheritance tax due when you pass away. Once in trust, your life insurance policy won’t contribute to your estate, meaning you’re less likely to meet the inheritance tax threshold.

Drawbacks of Having Multiple Life Insurance Policies

While having multiple policies has many benefits, we must also mention their drawbacks. These can be divided into potential issues for policyholders and beneficiaries.

As a policyholder, you need to remember that you have to finance your premium payments on a regular basis. The more policies you have, the more difficult they can be in terms of management, for example, because of different payment due dates.

Also, multiple life insurance policies may not be the best solution based on your circumstances. Sometimes, creating a joint policy or taking out different types of additional coverage may be more cost-effective.

If you’re unsure which option is best for you, you can always seek assistance from a professional advisor, such as Insurance Hero.

Beneficiaries will have to make multiple claims to receive payouts from all life insurance policies you take out.

This process can be complicated, tiring, and time-consuming. Nevertheless, many consider it worth it, given the final outcome.

Different Types of Life Insurance Policies

The right life insurance policy for you will depend on what you need coverage for, how much life insurance coverage you need, over what period, and when’s the best time to take it out.

Below, you’ll find several different types of life insurance policies. Read on to learn which one suits you best.

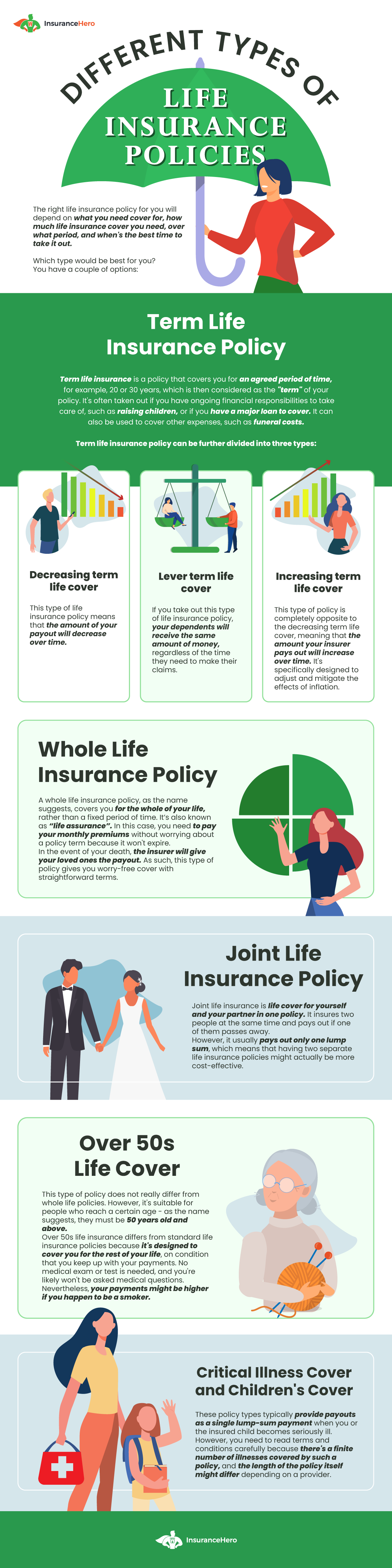

Term Life Insurance Policy

Term life insurance is a policy that covers you for an agreed period of time, for example, 20 or 30 years, which is then considered as the “term” of your policy.

It’s often taken out if you have ongoing financial responsibilities, such as raising children or a major loan to cover (for example, a mortgage). It can also cover other expenses, such as funeral costs.

Term life insurance policy can be further divided into three types:

- Decreasing term life cover – This type of life insurance policy means the payout amount decreases over time. People often take it out when their financial responsibilities, such as loan repayments, mortgages, or debts, decrease over time. However, there’s an interest cap on decreasing term life cover, meaning the payout may not always cover the full amount of your outstanding debt.

- Level term life cover – if you take out this type of life insurance policy, your dependents will receive the same amount of money, regardless of the time they need to make their claims. However, level-term life cover does not adjust for inflation. For long-term policies, the increasing cost of living is likely to make the existing coverage amount worth less over time, if not insufficient.

- Increasing term life cover – this type of policy is opposite to the decreasing term life cover, meaning that the amount your insurer pays out will increase over time. It’s specifically designed to adjust and mitigate the effects of inflation. The increase can be index-linked (in line with inflation) or fixed, which can be more beneficial if you keep it long enough. This way, it may rise faster than the inflation rate. Regardless of the type of increase, this type of life insurance policy offers an attractive solution for people whose families might need more assistance as the years go by.

Whole Life Insurance Policy

As the name suggests, a whole life insurance policy covers you for the whole of your life rather than a fixed period of time. In this case, you can pay your monthly premiums without worrying about a policy term, as it won’t expire.

In the event of your death, the insurer will give your loved ones the payout. This type of policy gives you worry-free cover with straightforward terms.

Whole life insurance policies, also known as “life assurance,” are usually more expensive than term life insurance.

However, some can be cheaper, provided they cover shorter periods for smaller payouts. Such policies also won’t have additional options, such as borrowing against the policy’s value.

Joint Life Insurance Policy

Simply put, joint life insurance is a single policy covering you and your partner. It insures two people simultaneously and pays out if one of you passes away.

Joint life insurance policies can be viable for you and your partner or spouse. However, depending on your circumstances, having a single joint life insurance policy may not be as cost-effective as having two separate policies.

It may also require your beneficiaries to pay inheritance tax with no deductions (which would not be the case if you put one of your policies in a trust). The best way to find out which is cheapest for you is to compare quotes.

Over 50s Life Cover

This type of policy does not differ that much from whole life policies. However, it’s suitable for people who reach a certain age – as the name suggests, they must be 50 years old and above.

Additionally, over-50s life insurance differs from standard life insurance policies because it’s designed to cover you for the rest of your life, provided you keep up your payments.

No medical exam or test is needed; you likely won’t be asked medical questions. Nevertheless, your payments might be higher if you are a smoker.

Taking out an over-50s life insurance policy can help your surviving partner and family deal with your passing and various financial obligations that are related to it, for example, by covering funeral costs.

You may also want to leave it to them as a gift. In this case, if you want to maximise the payout, consider putting your life insurance policy in a trust. This way, it won’t be liable to inheritance tax and won’t fall within your estate.

Critical Illness Cover and Children’s Cover

These policy types typically provide a single lump-sum payout when you or the insured child becomes seriously ill.

However, you need to read the terms and conditions carefully, as the policy covers only a finite number of illnesses, and the policy length may vary depending on the provider.

All in all, critical illness cover is considered a very sensible addition to your existing policy. Many people often take out additional cover for their children.

Another policy that’s similar to critical illness cover is terminal illness cover. In this case, your family will receive a lump sum if you’ve been diagnosed with an illness from which you will die in the next twelve months.

Frequently Asked Questions

This section answers some of the most frequently asked questions regarding life insurance policies.

Is it legal to have more than one life insurance policy?

Yes, it is legal to have more than one life insurance policy. That’s because different policy types work best for protecting different types of assets, and you may want that extra coverage at some point in your life.

You can also purchase additional life insurance policies at different times and combine them according to your budget and family needs.

How many life insurance policies can I have?

You can have as many life insurance policies as you want and can afford; there is no legal limit.

How do life insurance policies work?

The process is relatively simple. First, you need to pay a fixed premium. Premium costs are influenced by factors such as age or lifestyle.

Keep your payments up, and your cover will last for the entirety of the agreed period – depending on the policy type, it can last for life.

Additionally, some providers don’t require you to make payments when you reach a certain age and allow you to keep your life insurance coverage.

Finally, your loved ones receive a fixed cash lump sum upon your passing. Some providers will return the premiums you paid in the case when you’ve only had your life insurance policy for a couple of years.

Can I have more than one beneficiary on my life insurance policies?

Yes, you can have multiple beneficiaries on your life insurance policies. However, the payout form for your policies varies depending on the policy type.

Usually, the payout from a single-life insurance policy forms part of the policyholder’s estate. On the other hand, the payout would typically go to the surviving policyholders in a joint policy.

Still, multiple beneficiaries can claim multiple life insurance policies in your name.

Do I need more than one life insurance policy?

The answer to this question is not as straightforward as you might think. You know that having more than one life insurance policy is possible.

However, the fact that you can take out multiple policies doesn’t mean you have to.

Depending on your needs, you might decide to purchase additional life insurance. However, in many cases, it might be better to adapt your existing deal according to various events and milestones in your life.

When should I change my existing life insurance policy?

Several life events may prompt you to consider changing your existing life insurance policies and increasing your coverage.

These include, but are not limited to:

- Remortgaging or taking out a new mortgage

- Having an increase in remuneration, either by a change of employment or promotion

- Becoming a parent (by having biological children or by adopting a child/stepchild)

- Getting married

- Entering a civil partnership

Can I have a life insurance policy with multiple companies?

Yes, you can take out multiple policies with more than one company. Legally, it’s not possible to claim against each policy.

However, we recommend choosing one provider and sticking with it, especially if you plan to take out more than one policy.

This way, you’re more likely to get the best premium payments. You may also strike a deal with your provider if you show them you found a more favourable offer.

When is the best time for me to take out life insurance policies?

As we mentioned before, this answer will depend on your individual needs. You may want to consider taking out life insurance policies earlier and paying lower premiums.

However, you may also decide to secure your assets upon major life events.

Ultimately, you must decide when to take out your first life insurance policy, change your existing cover, or opt for multiple policies.

Remember, though, that it’s always better to have at least some form of insurance coverage than have the worst-case scenario happen to you while you’re completely unprepared.

Can you have more than one life insurance policy? Closing thoughts

Many types of life insurance policies and other types of policies may protect your and your family’s livelihood.

Answering the most burning question, you can legally have as many life insurance policies as you want. However, we encourage you to consider your options and make a decision based on your individual circumstances.

You can take out more than one policy if your existing deal no longer fits your needs, but consider looking for life insurance arrangements with the same provider.

This way, you’ll likely receive extensive coverage at a reasonable price. After all, it’s better to be safe than sorry!

Why Use Insurance Hero?

Regardless of your profession, age, and lifestyle, experts at Insurance Hero can help you find the best life insurance policy suited to your needs.

We work with reputable insurance providers ready to offer you a sensible deal at a reasonable price. Take care of yourself and your loved ones today, and contact us.

Steve Case is a seasoned professional in the UK financial services industry, with over twenty years of experience. At Insurance Hero, Steve is known for simplifying complex insurance topics, making them accessible to a broad audience. His focus on clear, practical advice and customer service excellence has established him as a respected leader in the field.