Whole vs Term Life Insurance Guide

Picking the right life insurance is one of the most important decisions you could make to provide your family with financial stability after you pass away.

Since there are several types of life insurance, you must thoroughly research which one is best for you.

One of the things you will have to decide on is whether you want to invest in whole life insurance or term life insurance.

Our whole vs term life insurance guide will discuss the differences between the two, including their pros and cons, so you can decide which is more suitable for your situation.

Compare Term And Whole Life Quotes, Completely Free Service, Save Money Now

Whole and Term Life Insurance – An Overview

First things first. Before considering the advantages and disadvantages, we must discuss their differences.

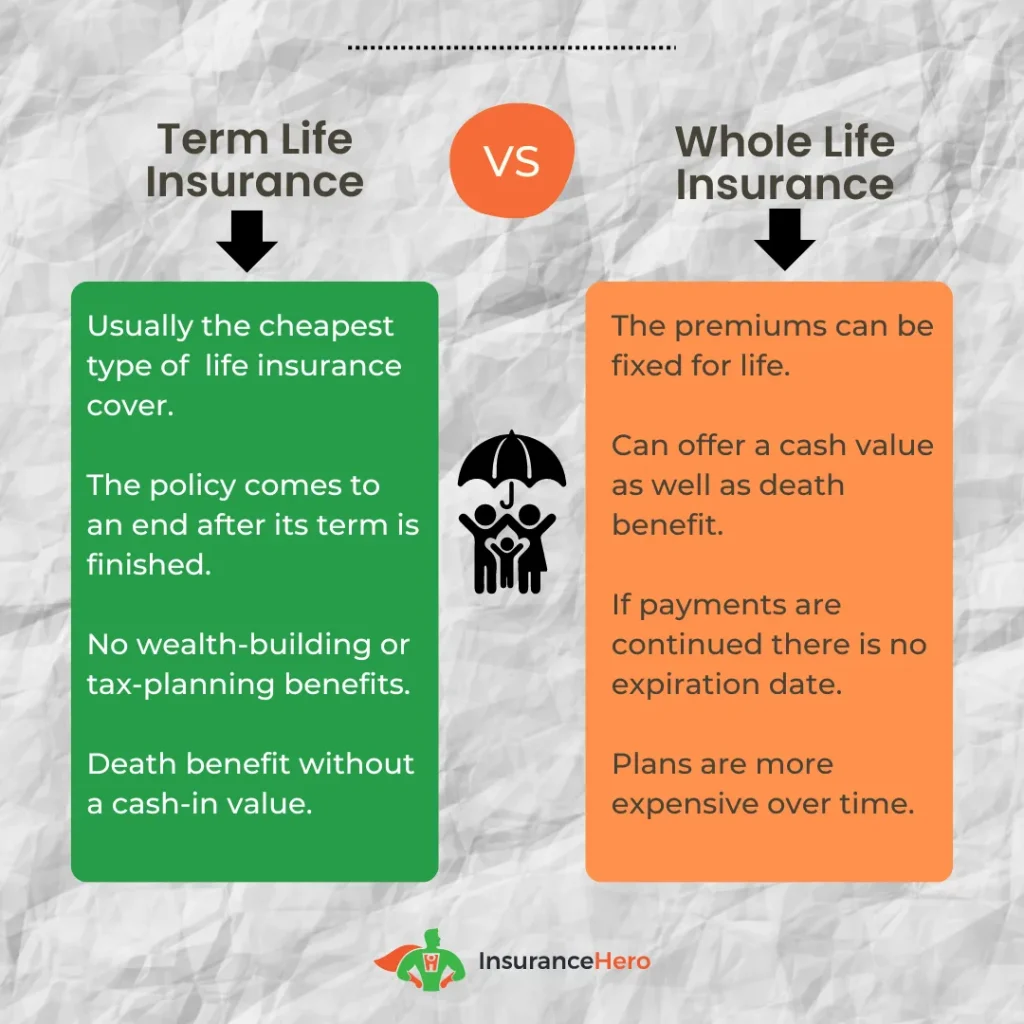

As you can probably deduce from the name, whole life insurance is a policy that covers a person from the moment they sign the policy until their death or until they stop paying their premiums.

Aside from a regular death benefit, a lump-sum payment to your beneficiaries after your passing, whole life insurance also features a cash value component. What is it exactly?

A portion of the premiums is invested throughout your policy. Once you reach a certain amount, you can borrow or withdraw from it, which is especially helpful when dealing with higher-than-usual expenses.

On the other hand, term life insurance covers a person for a specific period. If you pass away during the coverage period, your beneficiaries will receive a death benefit.

However, if you don’t, no one receives any money, and you outlive your coverage. It is very common to take out term life insurance around significant milestones, such asbecoming a parent.

As you can probably imagine, both whole life insurance and term life insurance have their advantages and disadvantages, and there are significant differences between them – being aware of these will help you decide which option will be the best option for you.

Term vs Whole Life Insurance – Similarities and Differences

Term and whole life insurance policies have their similarities and differences

Similarities

The main similarity between whole and term life insurance is that you pay a monthly premium to maintain the policy. Once you stop paying the premium, your insurance will become invalid. Both will also provide your beneficiaries with a death benefit upon your death during the coverage period.

Both whole life insurance and term life insurance are usually taken out to ensure that the people you care about are protected. Term life insurance is more common when you have a financial obligation with a specific timeline, such as a mortgage or the cost of raising a child.

Whole of life insurance, on the other hand, is mainly taken out so that when you pass away, your family and dependents wouldn’t have to worry about the costs of the funeral, as well as lowering their standard of living.

Differences

The first and foremost difference between these two types of insurance is that whole life insurance provides coverage from the moment you sign the policy up until your death, no matter when that happens, while term life insurance covers you only for a specific number of years.

That means the payout is guaranteed for whole life insurance (unless you stop paying your premiums). In contrast, with term life insurance, your beneficiaries will receive a payout only if you die during the coverage period.

Another difference is that whole life insurance, in addition to the death benefit, also comes with a cash value component, which we already discussed.

As for how it looks in relation to taxes, the invested amount grows on a tax-deferred basis, which means that you only pay taxes on this amount once you withdraw the money, not before.

The third difference between the two is that with whole life insurance, premiums are usually the same throughout the policy’s duration.

On the other hand, with term life insurance, you have three options: increasing, decreasing, or level.

What does this mean?

If your term life insurance is increasing, your premiums will start low and increase every year—the same goes for the sum your beneficiaries will receive.

If your term life insurance is level, your premiums and the lump sum will remain the same. Finally, your monthly premiums and the death benefit will decrease each year if you have a decreasing life insurance policy.

When you decide to go with term life insurance, you most likely won’t be able to avoid providing medical information, as the insurance provider needs to calculate how much of a risk you are. If they don’t ask, you probably will have to pay higher premiums.

On the other hand, whole life insurance allows you to obtain a policy without disclosing your medical condition. In the UK, it can be done with over 50s life insurance.

Which Is Better – Term or Whole Life Insurance?

| Term Life Insurance | Whole life insurance |

|---|---|

| Coverage for a specific period of time | Coverage until death |

| Payout in case of death | Payout in case of death |

| There are three premium options to choose from – decreasing, level, and increasing | Premiums stay the same for the entire duration of the policy |

| Death benefit | Death benefit plus cash value |

| Cannot avoid medical underwriting | Can avoid medical underwriting |

| Less expensive | More expensive |

Life insurance is very individual, so we cannot precisely answer which is better – only you can decide.

However, we can give you general guidelines on when to choose one life insurance policy over another.

You should consider a term life insurance policy if:

- You have a specific financial obligation you don’t want your family to worry about if you pass away, such as a mortgage.

- You have children and want to ensure they won’t have to worry about college tuition if you pass away.

- You want your life insurance policy to cover you only for a specific period, such as until retirement.

- You want the more affordable life insurance option.

- You’re not planning on using your life insurance policy as an investment vehicle.

You should consider a whole-of-life insurance policy if:

- You can afford to pay the higher premiums.

- You want a life insurance policy that will cover you until the end of your life and a death benefit that will be paid out no matter when you die.

- You have a lifelong dependent, for example, a child with disabilities.

- You want a life insurance policy to build up a guaranteed cash value you can use during your lifetime.

Term Life Insurance vs Whole Life Insurance – Frequently Asked Questions

What should you consider when choosing between whole-of-life and term life insurance?

Several things will affect your life insurance policy.

Here are some of the questions you should ask yourself whenever you’re choosing which one you should go with:

- How old are you?

- Are you in good health?

- Does your family have many financial needs?

- Do you have children? If so, how old are they?

- Are you concerned about a serious illness and long-term health expenses?

- Do you have a mortgage? How much is it? Do you have any other debts?

- How will you or your family pay for your funeral expenses?

- What are your retirement plans? Do you maybe hope to retire at an earlier age?

- Do you already have some kind of life insurance (for example, because of your employer)?

- Are you concerned about estate planning and tax ramifications?

What happens if I outlive my term life insurance?

Term life insurance is valid only for several years, so you will probably outlast your policy.

If that’s the case, you have three options in which you can continue – you can decide to become uninsured, you can reapply for another term life insurance policy, or you can convert it into a whole life insurance policy.

Can I have both whole and term life insurance?

Yes, there’s nothing preventing you from having both term and whole life insurance policies. If anything, it will leave your dependents even more financially secure as they will receive death benefits from both of those policies. What’s more, the policies don’t have to be from the same company.

Can I convert my life insurance policy?

If at any point you decide that the life insurance policy you currently have is not the one you actually want (for example, you have a term life insurance policy but decide a whole life insurance policy will be a better option and vice versa), you can change it. However, you should be aware that in some cases, the change may incur an additional fee.

Whole vs Term Life Insurance: The Bottom Line

If you want to take care of your loved ones even after your death, life insurance is probably the best way to do so. However, there’s a lot more that goes into picking the right insurance, not only choosing the provider you want to go with (although that is important, too, of course).

One of the most important decisions you must make is whether you want a whole life insurance policy or a term life insurance policy. As you can see above, they are quite different, and the one that is more suitable for you depends on several factors.

Once you decide which one you want to go with, don’t hesitate to reach out to us. Our experts will help you compare plans from leading life insurance providers so that you can make a fully conscious decision. Get in touch and receive a no-obligation free quote today.

Steve Case is a seasoned professional in the UK financial services industry, with over twenty years of experience. At Insurance Hero, Steve is known for simplifying complex insurance topics, making them accessible to a broad audience. His focus on clear, practical advice and customer service excellence has established him as a respected leader in the field.