Discover What A Life Insurance Beneficiary Means

Life insurance is a vital component of financial planning, giving you peace of mind knowing that your loved ones will be taken care of when you’re gone.

But do you know what a life insurance beneficiary is and how it affects your policy?

Understanding the role of beneficiaries and their significance in the insurance process can make a difference when deciding on a policy that suits your and your family’s needs.

In the UK, life insurance trusts protect the proceeds of a life insurance policy in the event of the policyholder’s death. By establishing a trust, the policyholder can ensure that the death benefit is paid directly to the designated beneficiaries, free from inheritance tax and outside of the probate process.

Typically, the trustee appointed to oversee the trust will be a professional legal advisor or a family member. The beneficiaries are named in the trust document and can be changed at any time by the policyholder.

Life insurance trusts are a useful estate planning tool because they offer greater control and flexibility in distributing assets after death. When establishing a trust, it is important to seek professional advice to ensure that all legal and tax implications are properly considered.

Beneficiaries Explained

Types of Beneficiaries

There are various types of beneficiaries that you can choose to include in your life insurance policy:

| Beneficiary Type | Description |

|---|---|

| Primary | The main recipients are first in line to receive the policy’s proceeds upon the policyholder’s death. |

| Contingent | Secondary recipients will receive the policy’s proceeds if the primary beneficiaries are no longer alive or unable to claim the benefits. |

| Revocable | Beneficiaries whose designation can be changed by the policyholder without their consent. |

| Irrevocable | Beneficiaries whose designation cannot be changed without their consent have a more secure interest in the policy. |

Life Insurance Beneficiary Payout Options:

| Payout Option | Description |

|---|---|

| Lump Sum | Beneficiaries receive the entire policy benefit in a single payment. |

| Annuity | Beneficiaries receive the policy benefit as regular payments over a specified period. |

| Interest Payments | Beneficiaries receive regular interest payments on the policy’s proceeds while the principal remains untouched. |

| Fixed Period | Beneficiaries receive the policy benefit as a series of payments for a specific duration, such as 10 or 20 years. |

The Role of a Beneficiary

A beneficiary is responsible for receiving the death benefit from a life insurance policy. This payout can provide financial stability, help cover funeral expenses, pay off debts, or act as an inheritance.

Choosing a Beneficiary

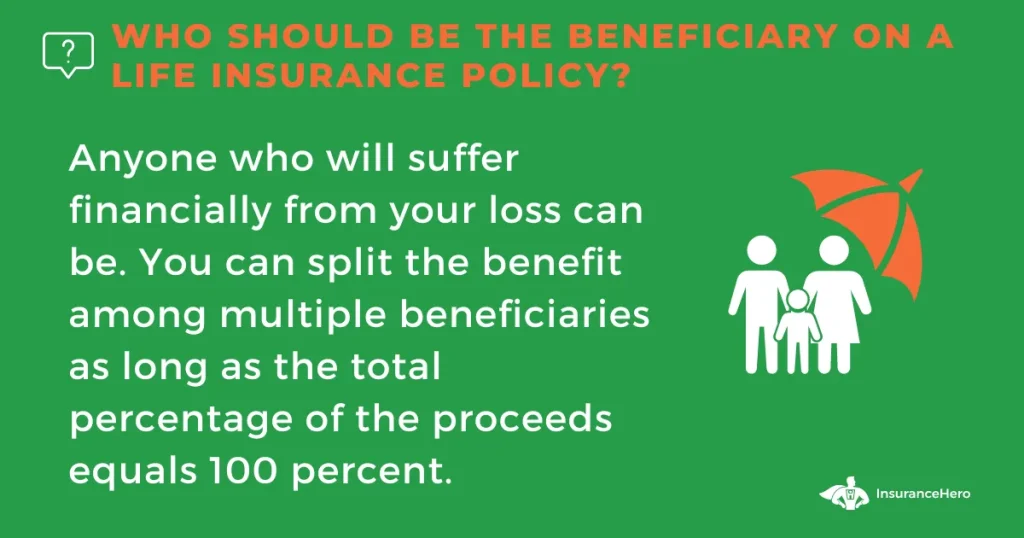

Selecting a beneficiary can be a deeply personal decision. It’s essential to consider the needs of those who depend on you.

Here are a few common options:

- 💑Spouses and partners: Your spouse or partner is often the first person you consider when choosing a beneficiary. By naming them, you ensure their financial stability after you’re gone.

- 👶Children: You may want to provide financial security for your children’s future, covering their education, housing, or other needs. However, minors cannot directly receive life insurance payouts in the UK, so setting up a trust or appointing a guardian to manage the funds is essential.

- 👨👩👧Relatives: Naming siblings, parents, or other relatives can be an excellent way to provide for their needs, especially if they depend on you for support.

- 🏥Charitable organisations: Leaving a legacy by naming a charity your beneficiary is a meaningful way to make a lasting impact.

- 📜Trusts: Establishing a trust can ensure that the life insurance proceeds are managed and distributed according to your wishes.

- 🏢Business partners: If you own a business, you may want to ensure its continuity by naming your business partners as beneficiaries. This allows them to buy out their share of the business and keep it running smoothly.

Life Insurance Trusts and Beneficiaries

Different methods exist for establishing a life insurance policy in trust, and as a potential beneficiary, it’s essential to understand these legal structures:

- An absolute trust: In this arrangement, the life policy owner (the grantor) transfers their policy to a dependable group of individuals (the trustees) for management. The grantor selects the beneficiaries from the beginning (with no alterations allowed). Eventually, the trust’s proceeds will be distributed to the beneficiaries.

- A discretionary trust: In this setup, the trustees can decide which beneficiaries will receive the trust, the amount allocated to each, and the distribution timing.

- A flexible trust: This structure includes two categories of beneficiaries – the ‘default beneficiary,’ who has the right to any trust-generated income, and the ‘discretionary beneficiary,’ who may receive capital or income from the trust only if the trustees designate them during the trust’s duration. If no designations are made by the trust’s conclusion, the default beneficiaries will receive all the benefits.

Beneficiary Designation Process

How to Designate a Beneficiary

When you apply for a life insurance policy in the UK, you’ll be asked to name your beneficiary or beneficiaries. Be sure to provide their full name, address, date of birth, and relationship to you to avoid any confusion.

Updating Beneficiary Information

Life events such as marriage, divorce, or childbirth may require updating your beneficiaries. Most life insurance policies in the UK allow you to update your beneficiary information anytime.

Regularly reviewing and updating this information is essential to ensure your policy reflects your current wishes.

Importance of Keeping Beneficiary Information Current

Keeping your beneficiary information up to date ensures the right people receive the death benefit. Failing to update your information can result in unintended consequences, such as the benefit being paid to an ex-spouse or bypassing your children.

Common Mistakes to Avoid When Designating Beneficiaries

When choosing your beneficiaries, it’s crucial to avoid these common pitfalls:

- Not naming a contingent beneficiary

- Naming minors without setting up a trust or guardian

- Not updating beneficiary information after significant life events

- Failing to consider the tax implications for your beneficiaries

- Not discussing your wishes with your beneficiaries

Legal Aspects

The Role of Laws in Beneficiary Designation

In the UK, the law guides how life insurance benefits are distributed. Still, it’s essential to familiarise yourself with the regulations that apply to your specific policy and situation.

Protecting the Beneficiary’s Interests

When designating beneficiaries, it’s vital to consider potential legal and financial issues that may affect them, such as:

- Estate taxes: Life insurance payouts are generally tax-free in the UK, but may be subject to inheritance tax if they are part of your estate. You can avoid this by placing your policy in trust.

- Creditors: In the UK, life insurance proceeds are typically protected from creditors. However, it’s essential to structure your policy appropriately to ensure this protection.

- Divorce: If you divorce, updating your beneficiary information is crucial to avoid any disputes or unintended consequences.

Disputes and Legal Challenges

While disputes and legal challenges to life insurance payouts are rare, they can occur. To minimise the risk, ensure your policy is up to date and discuss your wishes with your beneficiaries.

Life Insurance Payouts

How Life Insurance Benefits Are Paid Out

Once a claim has been submitted and approved, the insurance company pays the death benefit to the named beneficiaries. This process is generally straightforward and quick in the UK, often taking just a few weeks.

Payout Options for Beneficiaries

Beneficiaries in the UK have several options for receiving the death benefit:

- 💰Lump-sum payment: The beneficiary receives the entire benefit in one payment. This option provides immediate access to the funds.

- 📅Annuities: The death benefit can be paid out in regular instalments over a specified period, providing a steady income stream.

- 💹Interest income: The insurance company retains the death benefit and pays the beneficiary interest on the funds.

Factors Affecting Payout Amounts

The amount your beneficiaries receive may depend on several factors, such as:

- Policy type: The five main types of UK life insurance policies are Level term, Decreasing term, Over 50s, Whole of life, and Income protection plans. Each type offers different coverage and benefits.

- Policy exclusions: Some policies may include specific exclusions, such as death due to pre-existing medical conditions or hazardous activities, which can affect payouts.

- Policy loans and withdrawals: If you have taken out loans or withdrawals from your policy, the payout your beneficiaries receive may be reduced.

Tax Implications

Tax Treatment of Life Insurance Proceeds

In the UK, life insurance proceeds are generally tax-free. However, if the payout forms part of your estate, it may be subject to inheritance tax. To avoid this, you can place your policy in trust, which keeps the proceeds separate from your estate.

Tax Implications for Beneficiaries

While life insurance payouts are typically tax-free, other taxes may apply to your beneficiaries, depending on their circumstances:

- Inheritance tax: If the death benefit forms part of your estate and exceeds the inheritance tax threshold, your beneficiaries may be liable for inheritance tax.

- Income tax: If your beneficiaries choose to receive the payout as an annuity or interest income, they may be subject to income tax on those payments.

Strategies for Minimising Tax Liability

To reduce the tax burden on your beneficiaries, consider the following strategies:

- Place your life insurance policy in trust

- Utilise gift allowances to transfer wealth during your lifetime

- Ensure your will is up-to-date and clearly outlines your wishes

Life Insurance Beneficiary Conclusion

Understanding the role of beneficiaries in life insurance is crucial to ensuring your loved ones are provided for when you’re gone.

You can create a solid financial plan to protect your family’s future by choosing the right beneficiary, keeping their information up to date, and considering potential legal and financial issues.

Key Takeaways

- Beneficiaries play a crucial role in life insurance policies

- There are different types of beneficiaries, including primary, contingent, and revocable/irrevocable

- It’s essential to keep beneficiary information up-to-date and avoid common mistakes

- Legal and financial considerations, such as taxes and creditor protection, should be taken into account when designating beneficiaries

- Life insurance payouts can be made through lump-sum payments, annuities, or interest income

📝Frequently Asked Questions:

How do I change my beneficiary on my life insurance policy?

You can change your beneficiary in the UK by contacting your insurance provider and providing updated information.

Can I name more than one beneficiary?

Yes, you can name multiple primary and contingent beneficiaries and specify the percentage of the death benefit each should receive.

Can a life insurance policy have multiple types of beneficiaries?

Yes, you can have a combination of primary, contingent, and revocable/irrevocable beneficiaries in your policy.

What happens if my beneficiary predeceases me?

If your primary beneficiary predeceases you and you have named a contingent beneficiary, the death benefit will be paid to the contingent beneficiary. If you haven’t named a contingent beneficiary, the death benefit will be paid to your estate.

Do beneficiaries have to pay taxes on life insurance payouts?

In the UK, life insurance payouts are generally tax-free. However, other taxes may apply, such as inheritance tax if the payout forms part of your estate or income tax on annuity or interest income payments.

Can other family members contest a life insurance policy?

While rare, disputes and legal challenges can occur. To minimise the risk, ensure your policy is up to date and discuss your wishes with your beneficiaries.

What is the difference between a revocable and an irrevocable beneficiary?

The policyholder can change a revocable beneficiary at any time, while an irrevocable beneficiary can only be changed with their consent.

📝Further External Resources

Money Helper – This UK Government website is a great starting point to learn about life insurance beneficiary rules in the UK. It offers a comprehensive guide on choosing the right policy and understanding who can be named as a beneficiary.

The Association of British Insurers (ABI) – The ABI is a trade association representing the UK’s insurance industry. Its website provides a wealth of information on life insurance beneficiary rules and other types of insurance.

Citizens Advice – This charity provides free, confidential advice on a range of subjects, including life insurance beneficiary rules. Its website offers helpful tips on ensuring your policy payout goes to the right person.

Which? – Which? is a consumer watchdog that provides unbiased reviews and advice on a range of products and services. Its website offers information on life insurance beneficiary rules, product reviews and comparisons.

Age UK – This charity supports and advises older people in the UK. Its website offers information on life insurance beneficiary rules relevant to seniors, as well as other aspects of financial planning and protection.

The Money Charity – This charity offers education and advice on financial matters. Its website covers topics such as life insurance and how to ensure your policy meets your needs.

The Financial Ombudsman Service – Offers impartial advice and support to consumers complaining about financial products and services. Its website contains life insurance information and what to do if you dispute with your insurer.

The Chartered Insurance Institute (CII) is a professional body for the insurance and financial planning industries. Its website offers a range of resources on life insurance and training and career development opportunities for people working in these sectors.

Steve Case is a seasoned professional in the UK financial services and insurance industry, with over twenty years of experience. At Insurance Hero, Steve is known for his ability to simplify complex insurance topics, making them accessible to a broad audience. His focus on clear, practical advice and customer service excellence has established him as a respected leader in the field.