Keyman Insurance Quotes And Key Person Policies 2026

Do you worry that your company will be adversely affected if a key staff member dies?

If your business relies on an individual whose absence would directly affect revenue and could put staff at risk, you should consider keyman insurance.

This guide will examine all aspects of 2026 key person insurance, including who needs it, how much a policy costs, and its tax implications.

Keyman Life Insurance Quotes: Get over £200k of Key Person Insurance from £7.60 Per Month

How Much Does Keyman Insurance Cost?

Keyman business insurance is quoted as life insurance only or life combined with critical illness cover.

Different factors will affect the cost of keyman insurance, which include but are not limited to the following:

- The length of the cover

- The amount of cover

- Does the cover include a critical illness component?

- The age and health of the key person

- Participation of the key person in dangerous activities

- Is the key person a smoker or a non-smoker?

Key person cover can start from as little as £7.60 a month for a non-smoking employee aged 35-45 on a ten-year fixed-term insurance plan.

For an older employee over 55 with critical illness cover included in the policy, the cost of insurance may rise to approximately £60.08 per month.

For a keyman protection insurance quote closely aligned to the needs of your business, Insurance Hero can help. We have experience in providing cover to different sizes of business, and our professional team of brokers are available to provide a quote on 0203 129 88 66

Criteria

| Criteria | Description |

|---|---|

| Role in Company | Critical to company success. |

| Impact on Operations | Significant effect on day-to-day operations. |

| Skills/Knowledge | Unique and hard to replace. |

| Revenue Contribution | A Significant contributor to generating revenue. |

Types of Key Person Insurance Cover

| Cover Type | Description |

|---|---|

| Life Insurance | Lump sum on death or terminal illness. |

| Critical Illness | Covers serious illnesses like heart attack, stroke, and cancer. |

Taxation and Policy Ownership

| Aspect | Description |

|---|---|

| Tax Treatment | Varies based on plan purpose and HMRC rules. |

| Policy Beneficiary | The business itself. |

Categories of Loss Covered

| Category | Description |

|---|---|

| Protection for Profits | Offsets lost income from sales, project delays, or cancellations involving a key person. |

| Shareholder/Partnership Interests | Enables surviving shareholders or partners to buy the deceased’s interests, maintaining control. |

| Guarantee for Business Loans | Coverage equals the value of the guarantee, protecting financial backers. |

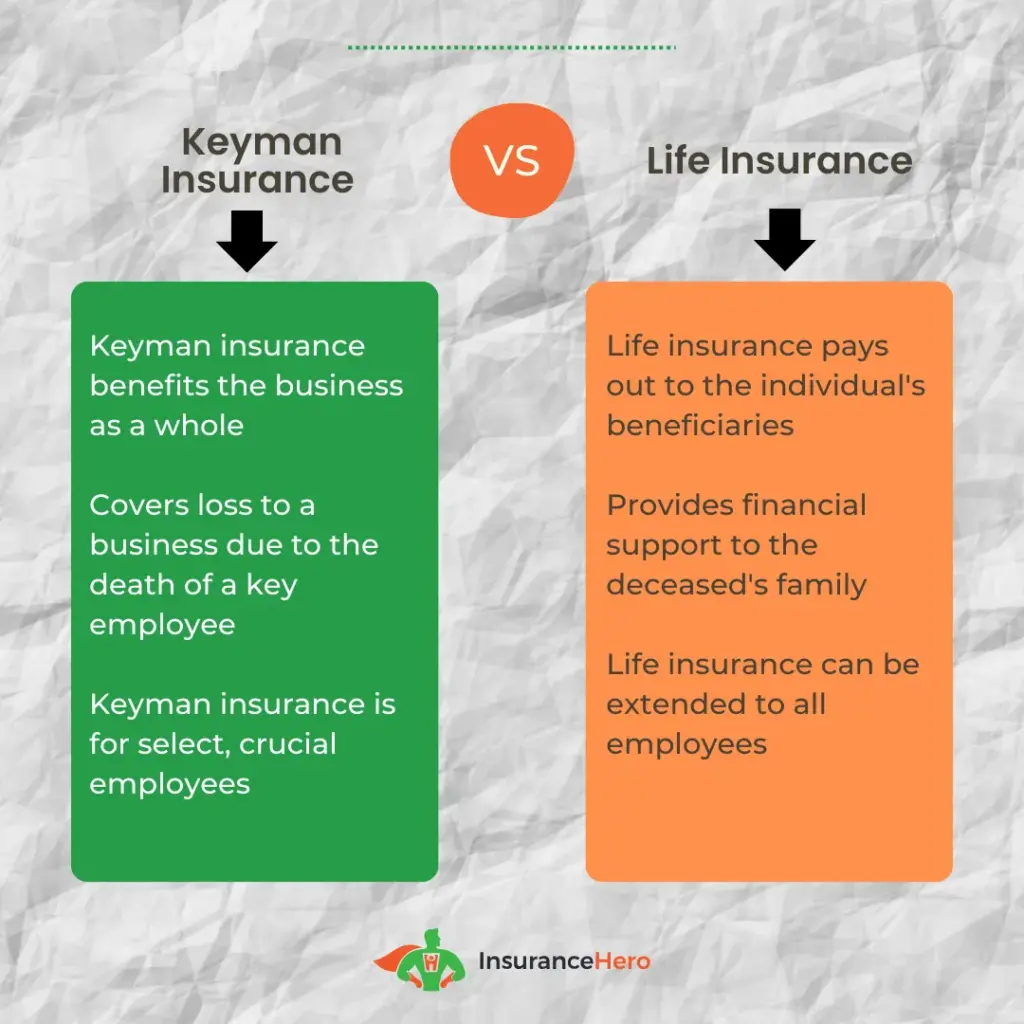

Key Person Insurance vs Other Business Insurance

| Insurance Type | Beneficiary | Purpose |

|---|---|---|

| Key Person Insurance | Company | Covers the loss of key individuals. |

| Relevant Life Insurance | Employee’s Family | Provides death-in-service benefits to employees’ families, which are not directly beneficial to the company. |

| Shareholder Protection | Remaining Shareholders | Allows shareholders to buy out the deceased’s share, maintaining business control. |

Process and Considerations for Key Person Insurance

| Step/Consideration | Description |

|---|---|

| Assessment of Need | Identify irreplaceable personnel whose loss would significantly impact the business. |

| Policy Purchase and Premiums | The company purchases the policy, pays the premiums, and is the policy’s beneficiary. |

| Use of Death Benefit | Funds can be used for recruitment, debt payment, investor payback, or business closure. |

| Term vs. Permanent Life Policies | Term life policies are generally cheaper but temporary; permanent policies cost more but offer lifelong coverage. |

Compare The Top 10 UK Insurers. Protect Your Business For Less

What is Keyman Insurance?

Fundamentally, key personnel insurance is provided by a firm to ensure critical staff members. An insurer underwrites a policy that provides a financial lump sum, or the sum assured, in the event of an insured employee’s death.

The payout amount is funded by paying a monthly or annual premium for the policy’s fixed duration.

What Does Keyman Insurance Cover?

A Keyman insurance policy will protect your business against financial losses if it loses a key staff member.

Typically, a plan includes a life insurance element to cover death; however, it can also include a critical illness element, where a diagnosis of a qualifying disease prevents the staff member from working permanently or for a long time.

Income protection can also be a component of a key man insurance policy, where key people continue to receive their salaries even if they cannot work for a period.

All policies will have slight variations, as each company will have different key employees it considers vital to the business’s ongoing financial success.

A payout has various uses:

- The cost to recruit and then train a replacement member of staff

- Creating a financial cushion against a potential loss of profits

- The winding down of the business in an orderly manner

- Smoothing over a potential loss of confidence from customers or suppliers

- Helping to cover any problems in raising new finance

Who Needs Key Person Cover?

Every business should have key man insurance, but UK statistics show that only 50% of companies have this vital coverage.

Employees are a critical asset of any company, and it is crucial to ensure business continuity should essential employees, partners, company directors, or a founder die or become unable to work.

Who is a key person?

A key person in a business is a person whose absence, through death or critical illness, could severely impact the company’s revenue.

Every business has a ‘key’ member of staff. The key person can be the company founder or CEO, a high-performing sales director, or an employee with a hard-to-replace skill set.

The answer to specific questions will identify a key member of staff and include:

- Would the absence of a key employee affect any essential projects?

- Do any company loan repayments depend on a particular person?

- Is a large client order at risk due to the absence of a critical person?

- Would suppliers get itchy feet and amend the terms of supply?

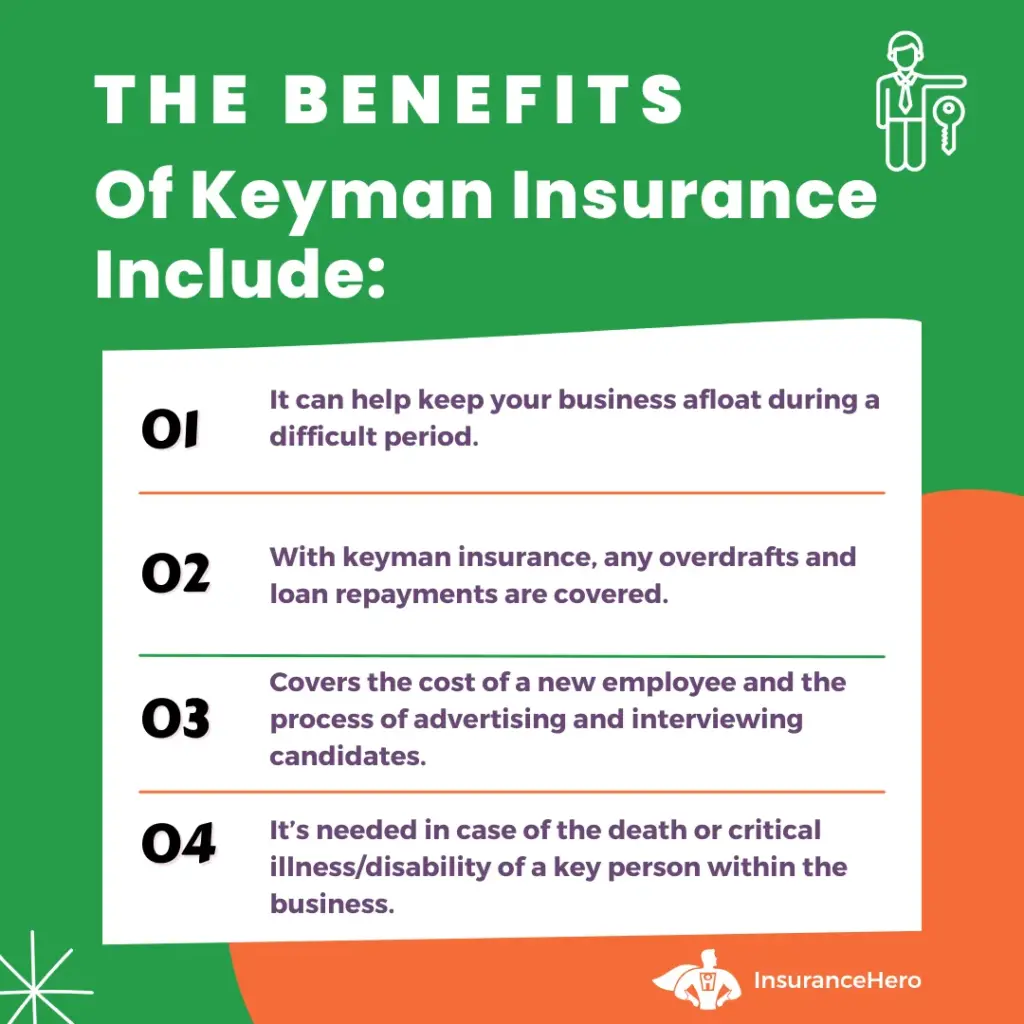

Key Man Insurance Benefits

Financial Stability

Provides a financial safety net for the business in the event of a key employee’s departure.

Business Continuity

Ensures business operations continue smoothly by covering financial losses resulting from the absence of a key team member.

Debt Protection

Helps service debts or loans that the key person might have been responsible for.

Investor Confidence

Increases investor confidence by safeguarding the business’s future.

Employee Retention

Demonstrates a commitment to employees, which can help retain and attract top talent.

Training and Recruitment

Covers costs associated with recruiting and training a replacement for the key individual.

Loss of Revenue Coverage

This compensates for potential revenue loss resulting from the absence of a key person.

Risk Management

A risk management tool that provides business owners and stakeholders peace of mind.

Tax Benefits

Potential tax benefits, such as premiums, are often treated as business expenses (subject to UK tax laws).

Flexibility and Customisation

This product offers flexible coverage options and can be tailored to specific business needs.

What Level Of Cover Is Needed?

Several factors influence the level of key man insurance you should consider. They can be discussed in greater detail with a broker or financial advisor, but as a rule of thumb, consider this most important factor:

Take the annual salary and multiply it by 5 as the minimum level of cover for consideration.

If the founder of a small business earns £250,000 per annum, then the key man insurance cover would be £1,250,000.

The following can also be a consideration when considering the level of cover, as well as the person’s salary:

- Profit multiples to protect the revenue and profit of the business

- The recruitment costs to employ a replacement

- The cost to pay off any debt associated with the keyman

Setting Up Key Person Protection

When setting up a key man cover, it is vital to consider your business’s legal structure, and your broker or advisor will guide you through this.

There are four main business types: sole trader, limited company, partnership, and limited liability partnership.

A sole trader, for example, will see the business owner or a key employee as the keyman.

A limited company, however, will have shareholders; often, the company’s founder can be a key man or another essential member of staff.

Key man insurance sole proprietorship?

Life insurance for a sole proprietor does not qualify as key employee life insurance. When the sole proprietor passes away, the sole proprietorship also ceases to exist.

Consequently, any financial liabilities or losses incurred due to the death of the sole proprietor are transferred to the proprietor’s estate rather than the business itself.

The purpose of life insurance in this context is to manage these financial obligations.

When a sole proprietor owns a life insurance policy on a key employee, it is called key employee life insurance.

What About Critical Illness?

Key worker insurance can also include critical illness cover. This means that a payout is not dependent on the death of a key employee.

A key person may also suffer a severe illness like a heart attack, a stroke, or a cancer diagnosis, as well as be likely to die. All are negative regarding the company’s profitability.

A lump sum may also be payable following a diagnosis of a critical illness or disease if the key employee survives at least 10 days from diagnosis.

A portion of the overall key person cover will include a premium payment for the critical illness component.

Not all illnesses are covered under critical illness insurance, and it is crucial to clarify or request the inclusion of specific diseases before the plan begins.

Examples of conditions include, but are not limited to, the following:

- Structural heart surgery

- Heart valve replacement or repair

- Primary pulmonary hypertension

- Cardiac arrest

- Kidney failure

- Liver failure

- Multiple sclerosis

- Primary pulmonary hypertension

- Major organ transplant

- Traumatic brain injury

- Aorta graft surgery

How Can I Buy Keyman Insurance?

Most Insurance Brokers and Financial Advisors offer plans. They will use their expertise to identify key employees in your organisation, select the appropriate level of cover and ensure that your business is fully protected.

Is Keyman Insurance Tax Deductible?

The rules surrounding Keyman Insurance and HMRC’s tax treatment can be quite complicated. It often depends on how a business intends to use any potential payout should a key person die or suffer a critical illness.

It is important to seek the services and advice of a tax adviser to ensure you receive accurate guidance before undertaking a policy.

Insurance Hero is happy to help with any matters relating to key person insurance, taxation, and keyman insurance corporation tax.

However, consider the following:

For staff

Key man insurance is a benefit for a company in HMRC’s eyes, meaning any premiums paid into the policy are tax-deductible.

For the shareholders

For Corporation Tax Relief, insurance premiums generally do not qualify as a keyman insurance policy that benefits the shareholders of the company and not the business itself.

For business loans

HMRC views key person insurance, specifically taken out against a business loan, as a benefit to the lender and not the company. This means that a business cannot deduct any premiums paid from its corporation tax.

Is Keyman Insurance A Benefit In Kind?

Key person insurance is not considered a benefit in kind. In a true key-man policy, no benefit accrues to the key worker or their family.

The company pays the premiums, and the proceeds are receivable by the company. The key worker’s life or health is insured.

Therefore, true key person insurance policies do not have PAYE (Pay As You Earn) or benefit-in-kind problems.

Smoking Habits And Their Effect on Insurance Costs

The habit of smoking is widely recognised for exacerbating various health problems.

Consequently, this behaviour often leads to higher insurance premiums, particularly for Key Man Insurance. Insurers typically adjust rates for insured individuals who smoke.

Nevertheless, some insurance providers adopt a ‘neutral’ stance on smoking, meaning they do not impose additional charges on smokers.

To illustrate the financial impact of smoking on insurance premiums, the Insurance Hero team obtained Key Person insurance quotations from Aviva.

These keyman insurance quotes were for a hypothetical scenario involving a healthy 30-year-old business executive seeking £500,000 in level-term coverage over a decade.

| Smoker Vs A Non-Smoker |

|---|

| 🚬 £35.71 | 🚭 £20.64 |

Additional Features of Keyperson Insurance

Keyman insurance policies are very comprehensive, and part of the policy will often include the following features:

- A stress and counselling helpline

- Physiotherapy and well-being sessions

- 24/7 access to a GP or medical professional

- Rewards and discounts that can be redeemed in shops for leading a healthy lifestyle

Other Related Insurance

Key person insurance is a business protection cover. Other types of protection that may be considered to protect your company include shareholder protection, business loan protection, and life insurance.

Shareholder protection

Cover to provide a cash lump sum for a surviving shareholder to buy the deceased shareholder’s shares, allowing the remaining shareholder to retain control of the company.

Business loan protection

A cover that repays any debt associated with the company; it includes commercial loans, bank loans, company overdrafts, commercial mortgages, or any other type of corporate debt.

Relevant Life Insurance

This company-paid life cover is intended to benefit the insured’s loved ones in the event of death, not as a direct benefit to the business. Relevant life cover is a tax-efficient insurance vehicle providing various tax reliefs on both the premiums paid and the ultimate lump sum financial payout.

FAQs

How long should keyman insurance last?

These plans are not designed for very long periods, as businesses’ needs change continually. Policy lengths of five to ten years are the most typical duration for keyman insurance.

Should the keyman cover be written into the trust?

Typically, coverage is not included in a trust, as the company pays the insurance premium.

The insurer will pay the company directly following a successful keyman protection claim. It is vital to seek advice from a tax specialist to clarify matters related to your company’s trusts.