Relevant Life Insurance Quotes And Cover Guide

As an employer, do you want to look after your employees beyond just providing them with a wage?

Did you know that Relevant Life Insurance can be offered to your employees so they can look after their loved ones if something should happen to them? In this updated guide for 2026, we explain Relevant Life Cover and how it could benefit your company.

Relevant Life Insurance Policy Benefits:

Relevant life insurance is an effective way for businesses to provide death-in-service benefits to employees while gaining substantial tax benefits.

Insurance Hero can help you find the most comprehensive and cost-effective life insurance quotes available.

Here are five key advantages:

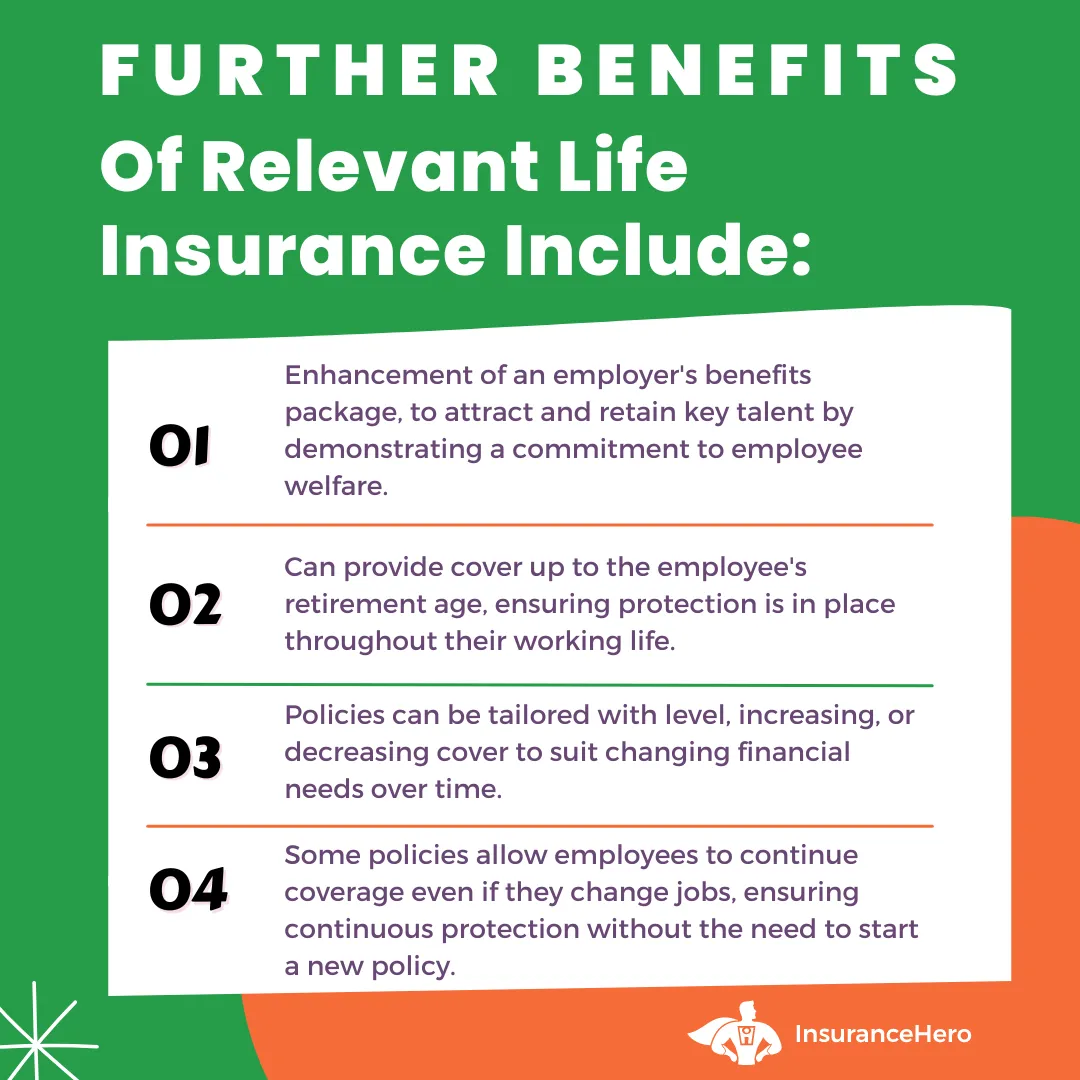

- Small Business Flexibility: Beneficial for smaller businesses, offering similar benefits as group schemes without needing eligibility.

- Talent Attraction: Demonstrates commitment to employee welfare, enhancing appeal to potential hires and helping retain important staff.

- Customisable Coverage: With inflation-linked options, coverage can be adjusted to your budget and needs, typically 15 to 25 times an employee’s salary.

- Tax Efficiency: Premiums are tax-deductible for the business and exempt from National Insurance contributions.

The Smartest Way To Provide Protection For Your Business And Employees. Get A Free Quote Today

Relevant Life Insurance Summary Tables:

Policy Duration:

| Criteria | Details |

|---|---|

| Policy Expiry Age | Up to 75 years old |

| Retirement Planning Consideration | Policy expected to last until retirement |

Cost Factors:

| Factor | Impact |

|---|---|

| Insurance Provider | Different providers calculate risk and, therefore, costs differently |

| Level of Cover | The chosen amount of cover significantly impacts the cost |

| Policy Term | The choice of policy term affects premiums |

| Age | Older individuals typically face higher premiums |

| Smoker Status | Smokers may see higher premiums than non-smokers |

| Occupation | High-risk occupations could influence premiums |

Optional Add-ons for Relevant Life Policies:

| Addon Option | Description |

|---|---|

| Fixed Increasing Life Cover | Cover increases annually by a set percentage |

| Index-linked Relevant Life Cover | Cover increases based on an index like RPI |

| Guaranteed Premiums | Keeps premiums the same for the full term |

| Reviewable Premiums | Allows insurers to review and potentially adjust premiums |

Key Legal Requirements for Relevant Life Cover:

| Requirement | Description |

|---|---|

| Policy Type | Must meet specific conditions under ITTOIA 2005 and ITEPA 2003 |

| Policy Holder | Only employers can apply for UK resident employees |

| Trust Requirements | Policies must be held in trust, paying out to nominated beneficiaries |

| Tax Considerations | Tax-efficient for both employer and employee, not counted towards lifetime pension allowance |

What is Relevant Life Insurance?

Relevant Life Insurance is a group life scheme paid for by a business for the benefit of its employees.

The cover is written into trust and pays out a lump sum of money to the scheme’s trustees, and for the employee’s benefit (beneficiaries) should they die while employed and the policy is in place.

Studies indicate that over two-thirds of businesses have never heard of Relevant Life Coverage, a death-in-service benefit.

Paying regular premiums for a product that provides staff with free insurance throughout a fixed-term policy can be beneficial for team morale, as it demonstrates that their employer genuinely cares for their well-being, going beyond just paying a wage.

Is Relevant Life Insurance A Benefit in Kind?

Benefits in kind are not included in wages and are offered to staff and company directors. They are also known as fringe benefits packages and include benefits such as private medical insurance or a company car.

Premiums paid into a relevant life policy are not benefits; instead, they are an allowable business expense. It means an employee does not need to pay National Insurance or income tax on the premiums.

What About Setting up a Trust?

Trusts can be complex structures, and employers must obtain proper advice when setting up a trust as part of a relevant life protection plan.

For insurance purposes, a trust is a legal arrangement that manages a life plan until the trust’s assets pass to someone else.

A trust includes four parties: the principal employer, the member (employee), the trustees, and the beneficiaries who will receive the trust’s contents.

A trust for relevant life protection ensures that:

- Trust assets are distributed to the rightful person.

- Trust assets pay out quickly.

- Trust assets payout tax efficiently.

Unlike other types of trust structures, a discretionary trust must be established. A discretionary trust allows for adding discretionary beneficiaries after the trust has been created, simply by writing to the trustees.

UK Relevant Life Insurance Experts. We Won’t Be Beaten On Price! Quick Quote Form

How Much Insurance Do I Need?

Most companies prefer to set up life insurance on a salary multiplier, with age and annual earnings as the key factors and a maximum coverage cap.

As a rule of thumb, many insurers break down the amount of cover required into different age brackets as follows:

- 17 to 39 years old: Up to a maximum of 25 X salary

- 40 to 59 years old: Up to a maximum of 20 X salary

- 60 to 69 years old: Up to a maximum of 15 X salary

How Much Does Relevant Life Insurance Cost

The cost of providing death-in-service benefits for staff will see different factors employed to assess the level of premium, including:

- The length of the policy term

- The amount of coverage

- The age of the staff member

- The underlying health of the employee

- If the employee participates in hazardous pursuits

- If the staff member is a smoker or a non-smoker

- Their family and home life

Example:

We have taken an example of two staff undertaking the same role as an office-based engineer, both non-smoking, with a family but no underlying health conditions, and only differing in age:

For a 25-year-old employee looking for £245,000 of protection, the premium is £6.97

For a 45-year-old employee also looking for £245,000 of protection, the premium is higher at £24.95

How Can I Set Up Relevant Life Cover?

It is essential to obtain sound guidance when setting up a group life scheme, as it involves complexities, including establishing a discretionary trust as part of the policy.

You can speak directly to an insurance provider, but an independent broker can help you access multiple providers, enabling you to get a more competitive quote. Insurance Hero can assist in every step of the process.

How Can Insurance Hero Help?

Insurance Hero is an independent broker specialising in life insurance, including relevant life cover. As an independent broker, we are not tied to any insurance provider. We can provide you with competitive quotes that also align closely with the needs of your business and employees.

Contact Insurance Hero at 0203 129 88 66; a professional adviser will be happy to help.

Featured Relevant Life Insurance Companies:

Vitality:

| Feature | Benefit |

|---|---|

| Eligibility | Aged between 16 and 70, UK resident (excluding the Channel Islands and the Isle of Man) |

| Plan Duration | The minimum term of one year must end before the covered person reaches 75 |

| Coverage Type | Single person coverage only |

| Cover Options | Level or indexed cover to keep pace with inflation |

| Minimum Premiums | Minimum monthly premium of £10, or £30 with Vitality Plus. Annual minimums apply. |

| Premium Calculation | Based on cover amount, term, age, health, lifestyle, and dangerous activities |

| Payment Frequency | Monthly or annually, via direct debit, EFT, or TT |

| Premium Changes | May change due to cover type, adjustments in cover, indexation, or Vitality Optimiser |

| Plan Flexibility | Options to increase or reduce cover, change the term, or adjust the Vitality Optimiser |

| Life Cover | Pays a lump sum on death or terminal illness diagnosis (with less than 12 months expectancy) |

| Healthy Living Programme | Rewards for healthy living with discounts and the potential to control future premiums |

| Claim Process | Benefits paid to the trustees of the Relevant Life Policy Trust are free of personal income tax and capital gains tax |

| Exclusions | No payout for suicide within 12 months of cover start or reinstatement |

| Cancellation Policy | You can cancel anytime. A full refund will be issued within 30 days of receiving the plan details. Conditions apply after that. |

| Complaints and Compensation | Procedures for complaints and access to the Financial Services Compensation Scheme (FSCS) |

Aviva:

| Feature | Benefit |

|---|---|

| Life Cover | Pays out a lump sum if the covered individual dies during the policy term. |

| Employee Significant Illness Cover (Optional) | Pays out a lump sum if the covered individual is diagnosed with a significant illness, survives for at least ten days, and the condition results in retirement or anticipated retirement. |

| Terminal Illness Benefit | It is included in both types of coverage and pays out upon the diagnosis of a terminal illness that meets the policy definition. |

| Tax Efficiency | Premiums may be considered an allowable expense for the business, potentially reducing corporation tax. |

| No Benefit in Kind | Premiums fully funded by the employer are not usually treated as income for the employee, thereby avoiding additional tax and National Insurance contributions. |

| Inheritance Tax | Benefits are not included in the employee’s estate for inheritance tax purposes, potentially offering a tax-efficient way to provide for beneficiaries. |

| No Impact on Lifetime Allowance | Policy proceeds do not count towards the employee’s pension lifetime allowance, avoiding potential tax charges for high earners. |

| Relevant Life Trust | Premiums may be considered an allowable business expense, potentially reducing corporation tax. |

| Continuation Option if Employee Leaves | Provides options for transferring the policy to a new employer or converting to a personal policy under certain conditions. |

| Suitable for Small Businesses and High Earners | Offers a tax-efficient life insurance solution for employees who might not have access to group life schemes or need to manage their lifetime allowance. |

Royal London

| Feature | Overview |

|---|---|

| Maximum Cover | For individuals under 40, coverage is up to 30 times the annual total earnings, with adjustments for age. |

| Coverage Type | Coverage is provided on an individual (single life) basis. |

| Premium Structure | Premiums are fixed and guaranteed throughout the term. |

| Benefit Payment | Benefits are paid out as a one-time lump sum. |

| Coverage Flexibility | Options include fixed, escalating, or diminishing coverage over the policy term. |

| Policy Duration | The policy term ranges from a minimum of one year to a maximum of 57 years. |

| Renewability | The policy term ranges from 1 to 57 years. |

| Eligibility Age | Coverage initiation is possible from 18 to 73 years, with termination at 74 years at the latest. |

| Coverage Limit | There is no cap on the coverage amount provided. |

| Inflation Protection | Coverage can increase annually by a fixed rate (2%-5%) or in line with the retail price index (2%-10%). |

| Decrease Option | Offers renewal options every 5 or 10 years for fixed and escalating cover types. |

| Policy Exclusions | Excludes claims from self-inflicted injuries within the first 12 months and non-compliant terminal illnesses. |

| Benefit | Explanation |

|---|---|

| Adaptable Coverage | The plan’s structure allows for adjustments in coverage to align with evolving financial responsibilities. |

| Claim Eligibility | Benefits are accessible upon the insured’s death or diagnosis of a qualifying terminal illness. |

| Customisable Protection | Clients can modify their coverage in response to changes in compensation or needs. |

| Inflation Adaptability | The plan offers mechanisms to adjust the benefit amount, preserving its value against inflationary pressures. |

| Renewal Flexibility | The plan’s renewal options provide continuity of coverage without necessitating a new agreement. |

Regarding HMRC, Are There Tax Benefits with Relevant Life Insurance?

Relevant Life Insurance is tax-efficient for both a business and its employees.

For the company

Life insurance premiums are an allowable business expense when calculating tax liability.

The structure of relevant life insurance often means premiums can be up to almost 50% cheaper than personal life cover.

For the employee

An employee does not need to pay National Insurance or income tax on premiums, as they are an allowable business expense rather than a benefit in kind, as we discussed earlier in this guide.

The welcome news for staff members is that any payout from life insurance policies does not count toward the employee’s lifetime pension scheme allowance.

Additional considerations for the employee regarding HMRC are that the plan is only available to those aged 75 or younger and that any payout is not subject to Inheritance Tax, as it is written into a trust.

What About Critical Illness Cover?

Insurers typically offer two types of relevant life protection: a stand-alone life policy and a life policy that includes critical illness cover.

Life insurance provides a financial lump sum of money if you should die, whereas a critical disease is not dependent on your death to payout.

Following the diagnosis of a qualifying illness, the insured employee must survive for at least ten days to qualify for the policy payout.

Like life insurance, critical illness coverage, if taken as part of a more comprehensive product, will use a portion of the premium for the significant illness cover.

Qualifying diseases or conditions are agreed at the start of the policy and can include the following:

- Heart attack

- Major organ transplant

- Benign spinal cord tumour

- Aorta graft surgery

- Heart valve replacement or repair

- Liver failure

- Multiple system atrophy

- Paralysis of a limb

- Structural heart surgery

- Severe lung disease

Is Terminal Illness Cover Included?

Terminal illness is typically covered under standard relevant life insurance and a policy with critical cover. It pays out if medical professionals do not expect the insured to live beyond 12 months following diagnosis.

Are There Other Policy Options and Benefits?

Relevant life cover does include further cover options as part of the overall policy, including the following:

Inflation-linked cover

Relevant life insurance can link to the rate of inflation, with the level of coverage either increasing, decreasing or remaining the same throughout the policy.

Increasing

Inflation-linked relevant life cover sees the premium and subsequent sum assured rise in line with the retail price index (RPI), a UK government benchmark.

Decreasing

Decreased cover means premiums and the sum assured fall throughout the policy. This is often taken up if the staff member has a mortgage that is being repaid and is gradually reducing.

Level

In level coverage, the premiums paid and the sum assured remain the same throughout the policy.

Guaranteed increase in coverage

The employer has some flexibility in managing employees’ needs under a relevant life insurance policy.

This means that some changes can occur without the need for additional underwriting.

Changes may include:

- A rise in salary

- An employee undergoes a divorce.

- The employee adopts a child.

- The employee gets married or enters a civil partnership.

- A staff member has increased a mortgage and needs additional coverage.

Additional benefits

The best life plans offer additional benefits from being part of a larger group scheme.

These include the following:

- Full bereavement support from professional advisers should loved ones need assistance following the death of the insured.

- A funeral component that pays out a portion of any lump-sum payout quickly, ensuring a proper funeral can occur if necessary.

- The support of specialist medical consultants to provide further medical opinions if required.

- 24/7 GP access via both telephone and video.

- Counselling sessions with a psychologist.

How Do You Make A Claim?

If your company needs to claim the death of an employee, it is an unfortunate and sensitive time. Insurers will look to make the claims process as simple as possible, often employing assessors trained to talk sensitively.

During a claims process, you should expect your insurer to:

- Check that the policy is still in place and that premiums are up to date at the time of the claim.

- Appoint a central claims assessor who will be the main point of contact throughout the claims process.

Summary

As a company, you will want to do your utmost for the well-being of your employees. Your employees may be well paid, but providing them with additional peace of mind that their dependents will be financially secure in the event of something happening to them is a real boost.

You can make this happen for your employees through a relevant life insurance policy.

Do not delay; instead, put in place a robust policy today.

Relevant Life Plans FAQs

What are the minimum and maximum ages for a policy?

The reply to this will depend on the insurer, but as a rule of thumb, the minimum age to take out a relevant life policy is 18, and the maximum age to purchase cover is 73.

What are the absolute minimum and maximum terms for level cover?

Most insurers will provide a minimum one-year policy coverage. However, such a short duration may not include terminal illness protection for a maximum term of 40 years.

What is the minimum amount of cover permitted under a policy?

Most insurers do not have a minimum permitted level of coverage; instead, any minimums are driven by the lowest premium that can be paid.

Do you recommend any particular provider?

Yes, we have had excellent feedback from clients who have taken out a policy with LV=.

LV= Relevant Life Cover is a tax-efficient life insurance policy designed for employers to provide individual death-in-service benefits to directors or employees.

It offers high-value, inheritance tax-free payouts through a discretionary trust, ideal for SMEs and limited company directors outside of group schemes.