Reduce Inheritance Tax With Seniors Life Insurance After 60

Many people view life insurance as a policy they pay into and then forget about. For some, it’s simply a pot of money left to their family upon their passing.

However, it can be much more than that.

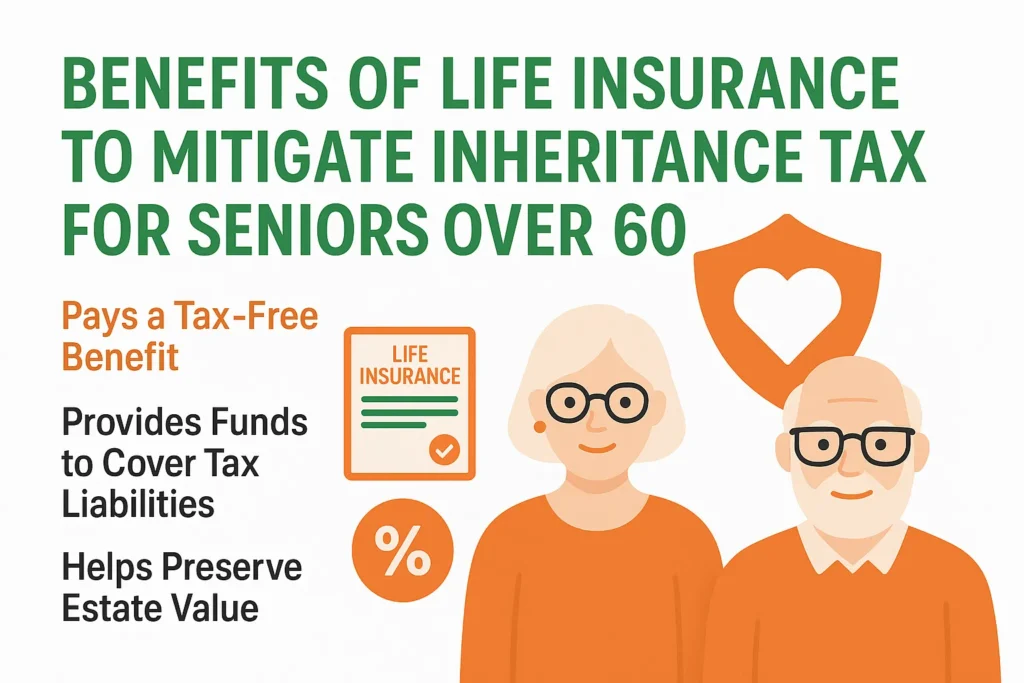

By providing a tax-free payment to beneficiaries, such as a spouse or children, life insurance can be used to cover taxes while maintaining the value of your estate.

Life insurance for those over sixty in the UK can be a minefield of fine print and competing providers, but with the right information and support, you can find a policy that will provide for you and your family.

Take Control Of Your Legacy. See How Life Insurance Can Ease The Inheritance Tax Burden For Your Family

| Consideration | Our Explanation |

|---|---|

| Purpose of Life Insurance | To provide funds that cover inheritance tax liabilities upon death, ensuring heirs receive the intended estate value. |

| Ideal Age to Start | Over 60 is common, but earlier is often more cost-effective due to lower premiums and better health. |

| Type of Policy | Whole of life insurance is typically used, as it guarantees a payment upon death. |

| Ownership Structure | Policies should be written in trust to keep the payout outside the estate and avoid increasing the inheritance tax burden. |

| Premium Affordability | Premiums increase with age; affordability and budgeting are essential for long-term viability. |

| Tax-Free Payout | Life insurance payments are typically exempt from income and capital gains tax, and can be structured to avoid inheritance tax. |

| Beneficiaries | Whole-of-life insurance is typically used, as it guarantees a payment upon death. |

| Financial Advice | Insurance Hero can assure that the policy is correctly structured for maximum tax efficiency and legal compliance. |

What Is Inheritance Tax?

Inheritance tax, also called the ‘death tax,’ is a tax applied to the value of a person’s estate after they pass away. In the UK, this tax is currently 40% of any amount exceeding £325,000.

- This means that if your estate’s total value is £400,000, 40% of £75,000 would be owed to the government.

Just as it’s important to understand how medical exams impact life insurance rates for seniors over sixty, it’s essential to grasp the nuances of inheritance tax.

While we all dream of passing on our wealth and success to our loved ones, it can take careful planning to maximise how much of what we own reaches them. Life insurance can be part of that planning.

How Life Insurance Can Help

One of the benefits of a life insurance policy is that it provides liquid resources for beneficiaries.

In the above example, to cover 40% of £75,000 owed, your spouse or children might be required to liquidate part of your estate, selling assets they would rather keep.

Provided it’s enough, the payout from a life insurance policy could cover this cost, leaving your estate untouched.

How to Avoid Inheritance Tax Affecting Your Life Insurance

The simplest way to protect your life insurance benefit from being taxed after your death is to put it in a trust.

- By doing this, you aren’t attempting to trick the government – this is a standard and straightforward process provided by many UK insurance companies.

- Putting your life insurance in trust means that one or more trustees legally own it. These are people who follow the rules you stipulate, establishing who benefits from your policy.

Another way to think about this process is that you are writing a will specifically for your life insurance policy. As a result, it can grant you more control over how your payout is handled.

Because you are granting control of your policy to someone else, it is no longer a part of your estate and thus will not be subject to inheritance tax.

This can leave the payout free for your beneficiaries to use for after-death expenses.

Calculating Coverage

If you want to protect your life insurance policy so your loved ones can use it to cover inheritance tax, the policy must be for the right amount.

Experts can assist you with this, but a starting point requires determining the value of your estate, understanding how much your investments may appreciate, and using the inheritance tax numbers above to calculate the size of the payout needed to adequately provide for your beneficiaries.

The Help You Need

Life insurance can be a lifeline to those you leave behind, and a little planning can go a long way in making sure it does as much good as possible.

Insurance Hero can help you through the entire process by providing fast comparisons of the UK’s leading providers.

If you’re still contemplating a new policy, be sure to read our article: Is life insurance worth it for seniors with no dependents? to see other uses of a policy that might surprise you.

Related resources to learn more about this subject:

- https://adviser.royallondon.com/articles-and-guides/protection/using-a-whole-of-life-plan-when-inheritance-tax-planning

- https://ifs.org.uk/taxlab/taxlab-taxes-explained/inheritance-tax-explained

- https://www.ageuk.org.uk/information-advice/money-legal/income-tax/inheritance-tax/

Steve Case is a seasoned professional in the UK financial services industry, with over twenty years of experience. At Insurance Hero, Steve is known for simplifying complex insurance topics, making them accessible to a broad audience. His focus on clear, practical advice and customer service excellence has established him as a respected leader in the field.