Best Life Insurance With Pre-Existing Medical Conditions 2024

Do you have underlying health issues? Do you worry about what would happen to you or your loved ones if something happened to you?

Did you know that life insurance is still affordable even if you have pre-existing conditions? Read on to learn why you should still consider getting life insurance with pre-existing medical conditions and why it may cost much less than you think.

How would the following be covered without proper pre-existing medical condition life insurance?

- When you pass away, will your estate be free from an Inheritance Tax Bill?

- Provision of cash gifts to relatives or children?

- Mortgage payments and other significant financial commitments. How will these be repaid if you die?

- Outstanding debts accrued in your name

- Planning for funeral arrangements

What is Life Insurance With A Pre-Existing Condition?

Life insurance is a financial safety net for you and your loved ones should you pass away unexpectedly. Paying a monthly premium into a fixed-term policy allows an insurer to pay out a lump sum of money to designated beneficiaries on a life insurance plan should the need arise.

It helps provide you with the financial peace of mind that any financial commitment agreed upon at the policy start will be covered.

Compare The UK’s Top 10 Insurers For Pre-Existing Medical Conditions. Find The Best Policy & Save Money Today

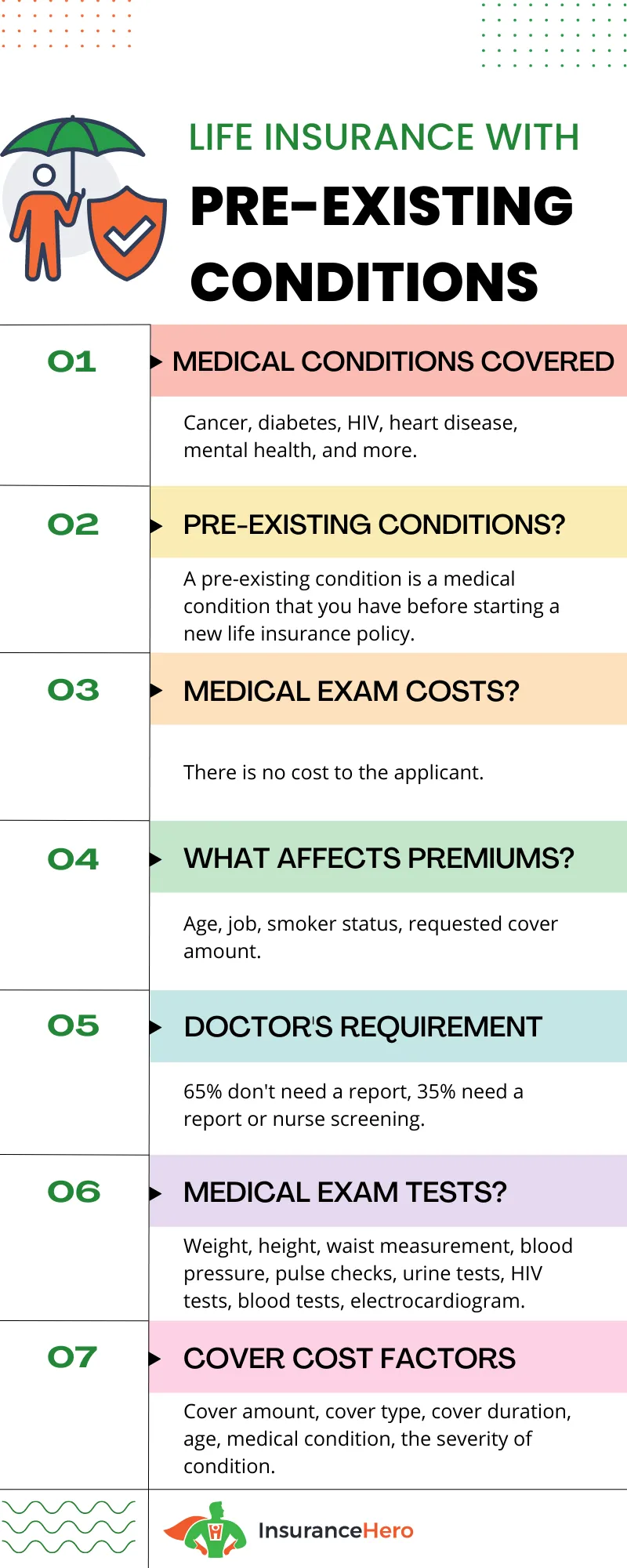

What Is A Pre-Existing Medical Condition?

Pre-existing medical conditions are a wide range of medical issues that already affect your life before you take out coverage and will affect the cost of life insurance to some degree.

A pre-existing health condition can include both life-threatening diseases such as cancer, stroke or heart attack or manageable conditions that typically include but are not limited to the following:

- High blood pressure

- Diabetes

- Asthma

- Obesity

- Depression

- Epilepsy

- Smoker-related conditions

Manageable conditions may not necessarily impact the risk of you dying and may even see policy premiums at standard or close to standard terms.

Depending on the severity of a pre-existing condition, the life insurance provider may need to see your medical records, speak with your General Practitioner, and ask you to undergo a medical examination before they can provide a quote for life cover.

Insurance companies must fully understand the severity of your condition and be aware of its impact on your daily life to accurately put in place a plan that closely aligns with your actual circumstances.

Life insurance with pre-existing medical conditions is a different process from traditional life insurance.

Applicants with a normal medical history are offered life insurance at standard terms through an online or voice questionnaire, and the insurance provider can quickly provide life insurance quotes without further medical consultation or examination.

Some Reasons To Choose Us:

- Compared With The Main Competition, There Are Fewer Exclusions For People With Pre-existing Health Conditions

- Secure Online Quotations. 5-Star Rated Service

- Safeguard Your Financial Future. 60-Second Form. Great Selection Of Insurance Plans. Protect Your Family

- Reliability – Honesty – Caring – Trustworthy – Amazing Prices – UK-Based Staff And No Overseas Call Centres

- Premiums For Older Individuals Routinely Preferable To Other Insurers

Help Protect Your Family’s Future. Compare Top Insurers. Find Your Cheapest Quote

What Do Insurers Think About Pre-Existing Conditions?

Life insurance providers base prices on how likely you are to make a claim. If you have a pre-existing medical condition, it can affect the life cover cost, depending on the severity.

Generally, the higher the risk of making a claim, the higher the insurance coverage. An insurance provider will calculate the cost using complex mathematical algorithms to provide a monthly premium.

Can You Be Refused Cover If You Have an Underlying Medical Condition?

In some instances, with pre-existing health conditions, life insurance may not be offered to you due to the severity of a pre-existing condition, with no insurance company prepared to provide a quote.

However, using a specialist broker experienced in providing insurance to those with existing conditions can make a difference. It can help with the quote process by ensuring accurate information and minimising the risk of rejection by underwriters.

How Insurance Hero Can Help You Get Life Insurance with Pre-Existing Medical Conditions

Insurance Hero is independent with experience providing life insurance with pre existing conditions in the United Kingdom.

As a specialist broker, Insurance Hero has relationships with underwriters that exclusively deal with those with pre-existing conditions and not generalist underwriters.

It means that Insurance Hero knows the life insurance application process for higher-risk life insurance intimately.

Through an extensive fact-finding questionnaire, Insurance Hero can provide specialist underwriters with the accurate information they need to move forward and give a quote that works in two ways:

Firstly, it allows the underwriter to accurately ascertain if they need to speak to a GP regarding your medical history and the level of medical examination you need to undertake.

Secondly, it allows the insurer to ensure that any life insurance policy with pre-existing conditions accurately reflects your circumstances closely. If you pass away, you must know that the document put in place is watertight and will payout.

Best Life Insurance Companies. Help at Every Stage. Simple Quote Process – 60 Sec Form

Why an Honest Approach Is Crucial When Applying for Life Insurance with Pre-Existing Conditions

When answering a fact-finding questionnaire, you must answer any questions honestly to ensure a plan accurately reflects your circumstances.

Suppose you pass away suddenly, and it is found that your death results from an undisclosed pre-existing medical condition. In that case, it may stop an insurance provider from paying out on a claim that may financially disadvantage your loved ones.

Insurance Hero has experience in providing life insurance for those with pre-existing conditions. Contact our experienced team today at 0203 129 88 66 to see how we can put together a plan that will protect your loved ones should something happen to you.

What About Mortgage Life Insurance with Pre-Existing Medical Conditions?

Life insurance is not a legal requirement to successfully apply for a mortgage. However, suppose you have a pre-existing medical condition.

In that case, consideration must be given to how your dependents will pay the mortgage should something unexpected happen to you, especially if you are the breadwinner.

If a watertight policy is implemented, any lump sum payout can be used to pay off outstanding mortgage repayments, ensuring your family can live rent-free and have financial peace of mind.

What Happens If I Develop A Condition Once the Policy Has Started?

If you develop a medical condition once a life insurance plan has started, this will not affect the policy’s terms.

Suppose you were honest about any pre-existing medical conditions and developed an illness at the start of the plan. In that case, it will typically not affect the validity of your policy.

What Is the Best Life Insurance for Pre-Existing Medical Conditions?

Selecting the appropriate life insurance with pre-existing conditions coverage depends on your specific circumstances and what you are looking to cover.

There are many different elements in a life insurance policy, and we will look at those now so you can get a better understanding of how to select the right life cover. However, a proficient broker will also assist you with this.

Whole of Life Insurance

The highest-costing type of life insurance cover is whole of life insurance, especially if you have a pre-existing condition. The insurer will financially payout on a policy when you die, as the insurance plan does not have a maturity date and is open-ended. As such, it is a higher cost than a fixed-term policy.

It is crucial that when choosing a whole of life plan, you take it out as soon as possible, as the younger you are at the policy commencement, the lower the premium. If you decide to take out this plan type when you are in your forties or fifties, it can be an expensive, albeit all-encompassing, insurance plan.

Fixed Term Insurance

Also known as term insurance, a fixed-term policy has a pre-decided duration, which may be anything up to thirty years, and may be aligned to a fixed-term financial obligation such as a mortgage.

A fixed-term insurance policy is much lower-cost than a whole-life policy. The downside is that no payout will be due should you die once the policy expires.

Over 50s plans – Life Insurance for Seniors with Pre-Existing Medical Conditions

When you reach fifty years old, it is still possible to submit a life insurance application for whole of life or term insurance, but it will become more costly due to an increased likelihood of you dying. A lower-cost option is an over 50s plan.

The lump-sum payout of this product type is lower than other life insurance with pre-existing conditions policies.

It operates on a guaranteed acceptance basis, where you will automatically qualify for policy cover even if you have an adverse medical record. No medical information, GP report, or medical examination is required for approval of this type of plan.

Any lump sum payout on an over 50s plan is rarely above £30,000, which is certainly not enough to pay off a mortgage.

Typically, this type of plan is employed to pay off small financial obligations, including personal loans and balances on credit card cards. It is also often used to pay for funeral costs or give children or grandchildren a small monetary gift.

Family Income Benefit

Family income benefit is a plan that works similarly to life insurance, where financial cover is provided should you pass away.

The critical difference is in how the payout takes place. Whereas a life insurance policy will pay out a lump sum upon the policyholder’s death, a family income benefit breaks a payment down into monthly amounts, which makes budgeting easier than receiving a large monetary payment.

Types Of Premiums: Life Insurance With Pre-Existing Medical Conditions

Life insurance is a flexible cover as the circumstances of a policyholder, particularly one with pre-existing conditions, may change throughout the policy.

Flexibility extends to the types of premiums available and includes increasing, decreasing or level cover.

Increasing cover

The monthly premium and the corresponding level of payout increase throughout the policy. The growth is in line with the UK government benchmark CPI index, a measure of inflation.

Selecting this premium option ensures that a payout will retain the same purchasing power at the end of a policy as it did at the start.

Decreasing cover

With decreasing cover, the life insurance premiums and the corresponding payout will decline throughout a policy. This cover type is typically tied to a fixed-term plan that provides financial protection against a mortgage whose payments also reduce over time.

Level cover

With level cover, the premium and corresponding payout level will remain the same for the policy’s duration. The disadvantage of this premium option is that the payout level may be small due to being eroded throughout the policy by inflation.

Associated Life Insurance Cover

Life insurance with pre-existing health conditions is a flexible type of cover. It is often associated with other insurance policies that provide financial coverage, either as part of a broader plan or as stand-alone cover.

Critical Illness Cover

Critical illness cover has a lengthy association with life insurance, often as an additional component within a policy.

Unlike life cover, you do not have to pass away for you and your dependents to benefit from financial cover. To qualify for a payout, you must survive at least ten days from diagnosis of a qualifying illness and no longer be able to work.

Typically, a list of common qualifying illnesses is detailed at the start of a policy, but this can also be tailored to include other specific illnesses.

Standard conditions include but are not limited to the following:

- Parkinson’s disease

- Alzheimer’s disease or pre-senile dementia

- Systemic lupus erythematosus

- Multiple system atrophy

- High blood pressure

- Heart valve replacement or repair

- Loss of hand or foot

- Structural heart surgery

- Heart disease

- Benign brain tumour

- Severe lung disease

- Coronary artery by-pass grafts

- Benign spinal cord tumour

- Traumatic brain injury

- Heart attack

Income Protection

Income protection is another financial product not dependent on death for the policyholder to benefit.

An income protection policy is set up to provide a replacement wage if you cannot work for a time due to an accident or illness.

When a replacement wage is forthcoming after you can no longer work, it often ties in with the statutory requirements of your employment contract regarding sickness pay.

For example, a company may pay their staff for three months when not in the workplace, which means a replacement salary for any policy would start after three months.

You should think about a policy if you have any of the following financial obligations, and if you have no savings, would struggle to pay them back if you are not able to work:

- Hire purchase agreement

- Mortgage

- Equity release loan

- Bank Overdraft

- Car loan

- Personal loan

- Debt owed on credit cards

Life Insurance With Pre-Existing Conditions Summary Table

| Definition | A pre-existing medical condition is an illness, injury or disease that the person had in the past or is currently experiencing before taking out life insurance. |

| Types of Pre-existing Conditions | Asthma and breathing problems, Heart disease, including heart attacks and angina, High cholesterol, High blood pressure, and Cancer. Strokes, including mini-strokes and brain haemorrhage, Anxiety, Depression, Diabetes, Obesity, Epilepsy, Cerebral palsy and other neurological conditions, Kidney diseases |

| Getting Life Insurance with a Pre-existing condition | Yes, but it might cost more, and the number of providers willing to cover may be limited. |

| Assessment | Everyone is assessed on a case-by-case basis. |

| Questions asked by insurance providers | General health and lifestyle, details of pre-existing medical conditions, medication, hospitalisation, family history of the condition, medical records, GP, medical assessment, and/or a medical examination. |

| Policy types | Policies with exclusions, Policies without exclusions |

| Type 1 diabetes | Insurance providers may be less strict. |

| Type 2 diabetes | There is a chance that providers might not offer you insurance. |

| Expert Opinion | Always declare all medical information to avoid the risk of not being covered. |

If you have pre-existing medical conditions, you may already know there may be challenges in getting life insurance coverage at a fair price that will include your ailments.

To increase your chance of insurance coverage, it is crucial to consider the services of insurers that specialise in this area. They will be able to guide you properly through the process and use specialist underwriters who have experience in pre-existing conditions.

Why delay in at least getting a quote for cover? Would you not like the peace of mind of knowing your family will be protected if something should happen to you?

Life Insurance With Medical Conditions Case Studies

Case Study 1: Young Couple – The Hughes Family

Meet James and Hannah Hughes, a young couple in their early 30s living in Manchester, England. They are the proud parents of two young children, Amelia and Liam.

James and Hannah work full-time jobs to provide a comfortable life for their family. However, they both have life insurance with medical conditions.

James, an IT professional, was diagnosed with Type 1 diabetes in his late teens. On the other hand, Hannah, a primary school teacher, recently discovered she had an underactive thyroid.

Their life insurance for medical conditions coverage offers them the security they need, ensuring that their children’s future is well-protected, no matter what happens.

By getting life insurance, James and Hannah made a responsible choice. Even though they have medical conditions, it hasn’t stopped them from obtaining life insurance for pre-existing conditions. Their plan is designed to provide a financial safety net for their dependents in the event of their untimely death.

Their life insurance medical conditions coverage will help them pay off any remaining debts and mortgage payments and potentially cover the costs of their children’s education.

You can secure your family’s future by taking life insurance with existing medical conditions cover through Insurance Hero.

After thoroughly analysing their situation, Hughes chose the best life insurance for pre-existing conditions. They worked with Insurance Hero, who compared multiple providers and policies to find them the right fit.

Securing life insurance with pre-existing conditions is feasible. It’s a responsible step for anyone with dependents. This case shows you can get life insurance with pre-existing conditions, providing much-needed peace of mind for you and your loved ones.

Case Study 2: Older Couple – The Bakers

Let’s now turn to the Bakers, Robert and Susan, a couple in their mid-50s residing in Leeds. Their three children are all grown up and settled.

The couple, however, is now responsible for caring for Robert’s elderly mother. Despite Robert having a heart condition and Susan battling rheumatoid arthritis, they’ve both secured life insurance with medical conditions.

Their life insurance for medical conditions provides them with a sense of security. They know that in the event of their passing, Robert’s mother will be taken care of. Their life insurance pre existing conditions ensures that the care costs for Robert’s mother, along with other financial obligations, will be met.

This coverage can help cover funeral costs and outstanding loans and ensure that Robert’s mother’s care is paid for, alleviating any financial stress from their children.

Through their life insurance medical conditions policy, the Bakers have peace of mind knowing that their responsibilities are catered for in their absence. They obtained a bespoke life insurance with existing medical conditions plan and are relieved knowing their loved ones are protected.

Robert and Susan reviewed numerous options before choosing the best life insurance for pre-existing conditions. They sought expert advice to secure a policy that fits their needs and budget.

Their story emphasises that securing life insurance with pre-existing conditions is not only possible, but it’s also a wise decision to ensure the financial stability of your loved ones.

It again confirms the answer to a common question – can you get life insurance with pre-existing conditions? Yes, you can.

Life Insurance With No Medical Exam Explained

Are you looking for a life insurance no medical exam policy? Did you know that in many cases, no medical examination is …

Life Insurance With A Heart Condition Quotes 2024

Can I Get Life Insurance If I Have A Heart Condition Or A Stent? Providers typically ask detailed questions reg…

Best Life Insurance For HIV Positive Patients 2024

In 2021, there were 107, 200 cases of people infected with HIV of which 27% of those were unaware they had the condition…

Life Insurance For Disabled Adults And People In The UK

Insurance Hero has tried hard to find the best life cover for those with a disability in the UK. From that list…

Best Cancer Life Insurance And Critical Illness Quotes

When a medical tragedy strikes, knowing there is financial support for you and your family can bring a lot of relief to …

Life Insurance Cover With Anxiety Or Depression 2024

In the UK, one in four people will experience some mental health issue each year, with the most common conditions encoun…

Best Diabetes Life Insurance Coverage 2024

Some people assume it is virtually impossible to secure life insurance with some pre-existing condition. This includes d…

Does Asthma Affect Life Insurance Underwriting & Your Chance Of Getting Cover?

Suffering from Asthma and considering life insurance? You can likely get cover when the condition is mild and identified…

Life Insurance With High Cholesterol 2024

High cholesterol and high blood pressure affect almost 30 percent of the population. If left untreated, these conditions…

Prognosis For Life Insurance Quotes After A Hypertension Diagnosis

Even if you haven’t had a stroke, or heart attack, there can still be issues with life insurance policies if you fail …

Epilepsy Life Insurance And Critical Illness Cover Guide

Pre-existing illnesses are more common now than a few decades ago. Insurance Hero is an insurance company speci…

Best High BMI Life Insurance For Overweight People In 2024

The average individual has a Body Mass Index (BMI) of 23. BMI is the measure of the ratio between height and weight. …

Do Any UK Companies Offer Female Cancer Life Insurance?

Cancer is a worldwide medical issue. More than 335,500 people in the UK will be diagnosed with cancer in 2025, according…

Life Insurance For Ex And Recovering Alcoholics

Life insurance is an essential product that helps individuals support their families, even when they are no longer aroun…

Best Life Insurance For Smokers & Vapers 2024

Estimates in the UK still indicate over 9 million people smoke despite smoking restrictions in indoor public places. Smo…

Best Impaired Risk Life Insurance Cover In 2024

It is well-known that health status affects the premiums offered by most life insurance carriers. If you’re ide…

Best Bipolar Life Insurance Options 2024

According to Bipolar UK, an organisation that provides support for people affected by bipolar disorder, 1.3 million peop…

Life Insurance With Lupus What Are Your Options?

Are you living with lupus and worrying about how it affects your chances of getting life insurance? You’re not …

Life Insurance With Crohn’s Disease 2024

Crohn’s disease is one of the main inflammatory bowel diseases that affects 1 in every 650 people in the UK. …

A Guide To OCD Life Insurance In 2024

Navigating the world of OCD life insurance (Obsessive-Compulsive Disorder ) might seem challenging, but don’t worry – …

Best MS Life Insurance Multiple Sclerosis Life Cover 2024

Understanding life insurance can be quite complex, especially when you’re navigating a condition like Multiple Sclerosis…

Is It Possible To Get Life Insurance After A Stroke?

Few things bring the fragility of life and the inevitability of mortality into focus quite like a major health event. …

Skin Cancer Life Insurance Cover, Is It Possible?

Cancer is a devastating illness, but it’s difficult to discuss primarily because it’s not just one disease. Canc…

Research Sources:

- How to get life insurance with pre-existing medical (Reddit)

- Can you get life insurance with a pre-existing condition in the UK? (Aviva)

- What are the most common pre-existing medical conditions covered by life insurance? (L&G)

Steve Case is a seasoned professional in the UK financial services and insurance industry, with over twenty years of experience. At Insurance Hero, Steve is known for his ability to simplify complex insurance topics, making them accessible to a broad audience. His focus on clear, practical advice and customer service excellence has established him as a respected leader in the field.