£100,000 Life Insurance Policy Cost 2026 – Simplified Quotes

One of the most popular questions that insurance agents and insurance companies are asked is, “How much does £100,000 of life insurance cost in 2026?”

When comparing insurance quotes, it is also essential to consider additional factors to determine how much life insurance is right for you and your family.

How much coverage you have is just as important as the company you work with. Here, we will discuss what you should know about choosing a policy.

£100 000 Life Insurance Summary:

We are pleased to report that a 100k life policy can be secured for around £4.71 per month for non-smokers. For smokers, the cheapest policy available through Insurance Hero is £5.81 per month.

Here’s why it’s worth considering:

- Financial Protection: Life insurance provides your loved ones with a reliable financial safety net, helping them maintain their lifestyle if you pass away.

- Debt Relief: Helps settle outstanding debts such as mortgages and loans, shielding your family from inheriting financial pressures.

- Cost-Effective: Coverage is affordable, with policies costing less than a single lottery ticket, making it accessible for most families.

We have thoroughly reviewed policies and premiums from various UK insurers, including those not listed on comparison sites.

We’re confident we can provide you with a more competitive life insurance quote than the biased, commission-focused comparison platforms.

Need 100k In Cover? Compare The Leading Life Insurance Companies To Get The Best Deal

How much does a 100000 life insurance policy cost?

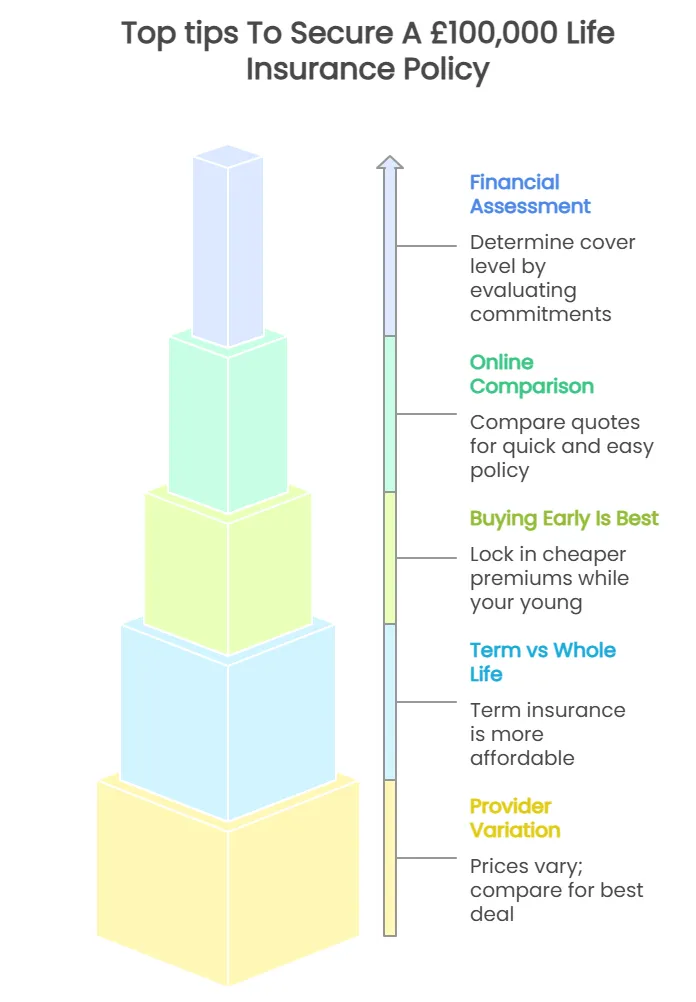

The cost of a 100000 life insurance policy depends on your chosen provider. Cost varies depending on factors such as age, health, and occupation.

We recommend comparing costs from various providers to find your best deal using our comparison form.

Below are example quotations for a £100,000 level term life insurance plan over a 10-year term, assuming the applicant is a non-smoker in good health:

| Age Of The Individual | Cost Of Cover For A Smoker | Cost Of Cover For A Non-Smoker |

| 20 | £5.79 | £4.65 |

| 25 | £7.21 | £5.33 |

| 30 | £9.82 | £6.81 |

| 35 | £12.56 | £8.92 |

| 40 | £19.74 | £12.39 |

| 45 | £24.72 | £15.35 |

What Does £100,000 Life Insurance Cost for Seniors and Over 50s?

Once you reach 50 and above, one of the most frequently chosen types of life insurance is an over-50s life plan.

These over-50 life insurance policies with 100k coverage typically offer guaranteed acceptance to UK residents aged 50 to 85 and don’t require any medical exams or health questionnaires.

However, because insurers are taking on unknown risks, the maximum coverage available is usually limited to around £20,000.

If you’re looking for a larger sum assured, such as £100,000, it’s still achievable with other types of policies, such as term life or whole-of-life insurance. However, please note that your age and health will impact the monthly cost.

Here’s an overview of sample monthly premiums for a £100k level term life insurance policy over a 10-year period. These figures are based on a healthy, non-smoking applicant.

| Age | Estimated Monthly Premium for £100,000 Cover (10-Year Level Term) |

|---|---|

| 50 | £16.93 |

| 55 | £19.24 |

| 60 | £29.35 |

| 65 | £41.23 |

| 70 | £62.46 |

| 75 | £113.88 |

💡 Tip: If you’re in good health and willing to answer medical questions, a term or whole of life policy could offer significantly more value than an Over 50s plan.

Special Insurer Deal For 2026

- Compared to the main competition, they have fewer exclusions

- Premiums for many age groups are much better than those of “household name” insurers

- Excellent reviews for customer care

- It comes with great rates for shared coverage

- Cigarette, pipe smokers and vapers are given fair treatment

Key Points of £100,000 Life Insurance Policy

| Key Point | Description |

|---|---|

| Payout | Cash lump sum (e.g., £100,000) if you pass away during the policy term |

| Coverage Use | Can cover mortgage payments, living expenses, funeral costs, etc. |

| Premium | A Monthly payment is required to keep the cover valid |

| Policy Types | Various types to suit different needs and budgets |

| Maximum Cover | Up to £1,000,000 of cover is available through Insurance Hero |

What could £100,000 Life Insurance Cover?

| Coverage Area | Description |

|---|---|

| Mortgage Payments | Pay off the mortgage or maintain the monthly repayments |

| Childcare Costs | Cover additional childcare costs or lost income |

| Family Living Costs | Maintain current lifestyle without cutbacks |

| Outstanding Debts | Cover debts to prevent loss of savings intended for loved ones |

| Funeral Costs | Cover funeral expenses (average cost in the UK: £9,300) |

| Inheritance | Leave a cash gift or inheritance for loved ones |

Life Insurance Reviewed

Before explaining the cost of life insurance, it is important to take a step back and review what life insurance is.

A life insurance policy is an agreement between a policyholder and an insurance company.

In exchange for the policyholder’s monthly premium payments, the insurance company agrees to pay a specified amount upon the policyholder’s death.

The policy’s beneficiaries can then use these funds to pay final expenses, handle debts, and cover costs.

Different Types of Life Insurance

Several types of life insurance policies cover different areas and can be purchased at varying monthly premiums.

Reviewing and understanding all available options is essential before deciding that £100,000 of life insurance is what you want or need.

Level Term Assurance

Level Term Assurance is when a person pays a set premium, usually guaranteed, for a set number of years, also referred to as a term.

Suppose the policyholder dies during the policy term. In that case, the insurance company will pay a lump sum of cash to beneficiaries as agreed upon and outlined in the policy.

This type of policy and lump-sum payment is often used to cover expenses for surviving family members or to pay off an interest-only mortgage.

Whole of Life Insurance

Whole of Life Insurance is similar to Level Term, but it does not have a set term during which it remains active.

This means that, regardless of how many years the policyholder has had it, it will pay a lump sum to the listed beneficiaries.

Because of this, Whole of Life premiums tend to be higher than those for other types of insurance, such as Mortgage Life Insurance or Level Term.

Whole-of-life policies are often chosen when there is a constant need for a lump-sum payout.

Mortgage Life Insurance or Decreasing Term Assurance

Both Mortgage Life Insurance and Decreasing Term Assurance work in the same way as Level Term Assurance.

The only difference is that coverage decreases over the policy term. Because the insured sum decreases over time, so do the premium payments.

Mortgage Life Insurance is often chosen when the policyholder wishes to cover an outstanding mortgage, as the remaining debt decreases, so does the coverage.

Family Home Benefit

Family Income Benefit works the same way as Level Term Assurance, except that instead of beneficiaries receiving a lump sum tax-free, they receive similar payments to the policyholder’s regular income stream.

This is the most popular choice when the insured does not want their beneficiaries to receive a large lump sum and would rather receive regular payments as if their income were still present.

Determining How Much Life Insurance is Needed

Choosing the level of life insurance coverage is often a highly personal decision. The factors influencing this decision are based on the policyholder’s unique circumstances and their specific needs and desires for a life insurance policy.

One question you can ask yourself to make the decision easier is: How will funeral costs and outstanding debts be paid when you pass away?

How will your mortgage be handled? And how much will your family need to survive in a lump sum or regular payments?

Our new life insurance average cost UK guide provides detailed cost breakdowns for the different types of life insurance currently available in the United Kingdom.

Payout Rates and Reliability

Life insurance payout rates for policies with a value of 100k or more are robust, with most major insurers approving between 97% and 99.5% of valid claims.

So, if you purchase a policy that meets its terms, the likelihood of you receiving a payout is exceptionally high.

Providers such as Aviva, Vitality, and Royal London have consistently demonstrated outstanding reliability, with life insurance payout rates ranging from 98% to 99.6%.

100 000 Life Insurance FAQs

How the Cost of Life Insurance is Determined

The cost of life insurance, or the premium, is determined by various factors.

These factors most often include the type of insurance policy, how much coverage is needed, how long the policy is active, the policyholder’s health and age, his or her lifestyle choices, and whether or not he or she is a smoker.

It is important to remember that every insurance company is different – what may be a significant factor for one may be only marginally important to another.

This is why it is so important to compare insurance options.

What Else Should You Consider When Receiving a Life Insurance Quote?

While the points mentioned above are among the most important to consider when choosing a life insurance policy, other factors should also be considered when comparing policy options.

The first of these additional considerations is your health as the policyholder. If you have any pre-existing conditions or health issues, speaking with a life insurance agent, such as one at Insurance Hero, may be beneficial.

Our professionals can help you find a life insurance company that will work with you, regardless of any concerning health or lifestyle issues.

Additionally, you may consider a joint life insurance policy if you have a spouse.

For joint policies, it is essential to remember that, although they are the most cost-effective, they will pay out only once, when the first joint policyholder dies.

While this may be ideal for a couple with no living children and/or family, those with surviving beneficiaries will probably want to secure individual policies.